Global| Jan 05 2018

Global| Jan 05 2018EMU Inflation Keeps a Low Profile

Summary

In December, the HICP headline rate gained only 0.1% and the core gained only 0.1%, both very modest increases. The year-on-year pace of the headline fell to 1.4% from 1.5% previously, obviously not pressuring the ECB to move any [...]

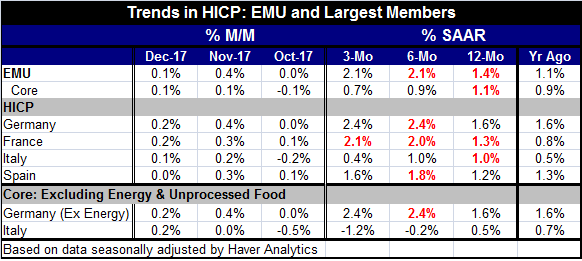

In December, the HICP headline rate gained only 0.1% and the core gained only 0.1%, both very modest increases.

In December, the HICP headline rate gained only 0.1% and the core gained only 0.1%, both very modest increases.

The year-on-year pace of the headline fell to 1.4% from 1.5% previously, obviously not pressuring the ECB to move any faster with its flirtations with restoring normalcy. The core rate is at 1.1% year-on-year for the third consecutive month after stepping down from a gain of 1.2% back in September. Clearly, inflation pressures are calm and not building in a systematic way.

The progressive growth rates for prices show headline prices at a 2.1% pace over three months and over six months compared to 1.4% over 12 months. The core shows inflation deceleration from 1.1% over 12 months to a pace of 0.9% over six months to a pace of 0.7% over three months. The headline is the highest rate and also the rate most affected by oil prices that have been cantankerous.

By country, the scheme is different as Germany has headline inflation at 1.6% year-on-year compared to 1.3% for France, 1.2% for Spain and 1.0% for Italy. Italy is now the low inflation country among the four largest EMU economies and Germany is now the high inflation country, my how things can change.

The progressive growth rates at the country level show German inflation at a 2.4% pace over three months and over six months compared to 1.6% over 12 months. The pace of inflation in Germany seems to have stepped up, but it is not a continuous acceleration. In France, inflation is accelerating from 1.3% over 12 months to 2.0% over six months and to 2.1% over three months. Spain shows mixed patterns with inflation at 1.2% over 12 months then stepping up to 1.8% over six months and falling back to 1.6% over three months. Italy shows inflation decelerating as the pace is at 1% for 12 months and for six months then drops off to a feeble 0.4% over three months.

Italy's core inflation rate also show disinflation and deflation as it's pace is at 0.5% over 12 months and falls to -0.2% over six months and to -1.2% over three months. In contrast, Germany's domestic CPI excluding energy shows inflation at 1.6% over 12 months and stepping up to a 2.4% pace over six months and over three months.

Nowhere are inflation trends really pressuring things. But in Germany and France, there are headline rates over three or six months or both that might breed some discomfort. Germany is the best performing economy in Europe so it is not surprising that with the lowest unemployment rate since German reunification it is now seeing some inflation pressure --and more than other fellow EMU members. Still, it is seeing very little inflation pressure.

Moreover, the ECB makes policy for all of the EMU and not just for Germany. While Germans may be uncomfortable, the German year-on-year rate is still in-bounds and the all-important EMU inflation rates are also in-bounds. Europe may be headed for more policy clashes at the ECB, but there is no inflation brewing at a pace that requires anyone's attention.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief