Global| Dec 18 2017

Global| Dec 18 2017EMU Inflation Is Still Too Low

Summary

Central banks have fallen into particular groups according to the environment in which they make policy. The European Central Bank and the Federal Reserve are in one group. That group faces ongoing and perhaps accelerating economic [...]

Central banks have fallen into particular groups according to the environment in which they make policy. The European Central Bank and the Federal Reserve are in one group. That group faces ongoing and perhaps accelerating economic growth paired with stubborn below-target inflation. Both countries in this group have taken steps to begin to prepare for a period of stronger growth and normal inflation ahead. Japan faces stubborn below-target inflation without any clear prospect of inflation normalcy. Weak growth in an environment where both growth and inflation have been extremely weak for a very long period put Japan in a special policy dilemma. The United Kingdom, in contrast, has solid growth and too high inflation. But the U.K. faces a coming negative shock to growth from its transition out of the EU arrangement and its inflation rate continues to run hot, but fortunately inflation is hotter than wage settlements so that real wages are actually eroded in the U.K. and inflation is not embroiled in a wage price spiral. The challenge for the Bank of England is to deal with its current too hot inflation without spoiling the economy for the challenge ahead when conditions will cool and perhaps do so sharply as the Brexit transition occurs.

Central banks have fallen into particular groups according to the environment in which they make policy. The European Central Bank and the Federal Reserve are in one group. That group faces ongoing and perhaps accelerating economic growth paired with stubborn below-target inflation. Both countries in this group have taken steps to begin to prepare for a period of stronger growth and normal inflation ahead. Japan faces stubborn below-target inflation without any clear prospect of inflation normalcy. Weak growth in an environment where both growth and inflation have been extremely weak for a very long period put Japan in a special policy dilemma. The United Kingdom, in contrast, has solid growth and too high inflation. But the U.K. faces a coming negative shock to growth from its transition out of the EU arrangement and its inflation rate continues to run hot, but fortunately inflation is hotter than wage settlements so that real wages are actually eroded in the U.K. and inflation is not embroiled in a wage price spiral. The challenge for the Bank of England is to deal with its current too hot inflation without spoiling the economy for the challenge ahead when conditions will cool and perhaps do so sharply as the Brexit transition occurs.

For these reasons, there is no general recommendation for money policies globally even though there is a synchronized upswing of global growth in progress.

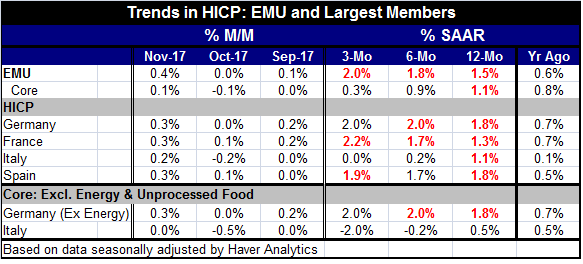

Conditions in the EMU show headline inflation is making inroads with the pace accelerating over short-term horizons from 1.5% over 12 months to 1.8% over six months to a slightly too-hot 2% pace over three months (the ECB target is for a pace just below 2%, so 2% itself is technically 'too fast.'). Still, core inflation in the EMU is much lower and trending in the opposite direction. Since oil prices have been greatly affecting headline inflation, central banks have been using the core rate as a better gauge for policy. In the EMU, the year-on-year core rate is just 1.1%; its annualized three-month rate is just 0.3%. That's hardly the stuff of building inflation.

In the U.S., inflation continues to undershoot and its 12-month core pace is 1.4% - not too different from the 1.1% pace in the EMU - while U.S. target inflation is up by just 1.6% (These calculations use the Fed's PCE definition since the Fed targets PCE inflation).

Anyway that you slice it, global inflation is not kicking in. The question here is whether the synchronized business expansion will drive inflation higher or whether the concerted central bank tightening (U.S. and BOE) plus less stimulus from the ECB will over compensate? Judging from the markets, there is nothing but confidence in the stock market, but the flattening U.S. yield curve tells a cautionary tale about a too restrictive U.S. monetary policy. Right now no one seems to take the yield curve too seriously, but serious it is.

The table below surveys the EMU more broadly sampling the inflation base across all the reporting original members of the EMU (plus Greece). It also shows the price level to date performances over the various member nations showing current price level divergence with low-inflation Germany comparing price indexes now with what they were when the EMU was first formed.

The price level in the EMU is now 6.2% higher vs. Germany that it was when EMU was first formed. Germany has improved its competitiveness vis-a-vis the whole EMU. But since Germany itself is part of that calculation for the EMU and since Germany has a large weight in the EMU, that comparison is not very telling. In the table, looking at country detail, we can see that only two of the ten countries in the table have price levels that have risen by less than 6.2% relative to the German price level since the EMU was formed. They are Finland (5.6%) and France (1.4%). The next most competitive economy with Germany is a tie between Italy and the Netherlands with both having had their price levels rise by 9.4 percentage points more than the German price level since the EMU was formed. At the other extreme, Luxembourg as a financial center is not so concerned with price competitiveness and that explains how the price level has climbed by 22.4% more than Germany's price level without much ill effect. Still Spain's price level has risen by 18.3% more than Germany's on this timeline and after austerity that is only about four percentage points better than Spain at its worst. Austerity has brought some remarkable changes to the price divergences of Ireland and Greece with Germany. But for most of the rest of the EMU, the progress has been minor and Germany retains significant competitive advantages based on its ability to have run lower inflation than everyone else in the EMU on a consistent basis.

Building pressures of disagreement

With these metrics in minds, we can see the uneven histories and choices various countries have had and can better understand the outlook dilemma being faced. The U.S. adopted at 2% inflation target in January 2012 and has had only one month since then where headline inflation exceeded 2% over a 12-month period. Core inflation has never equaled or exceeded 2%. In the EMU, inflation is below 2% everywhere and in some places the pace of inflation is still falling. But inflation is gaining pace in Germany where the unemployment rate is the lowest in Europe and where inflation fears burn hottest. The tensions between the policy choices of Germans and other ECB members are going to increase as German inflation rises to 2% and maybe above it while EMU inflation will remain 'too weak' and the push for continued policy accommodation will dominate ECB policy despite German protests. In the U.S., we can already see from the so-called 'dot plots' that some FOMC members are getting increasingly worried about inflation rising even as it continues to undershoot. The year ahead is sure to produce more friction and fireworks at the ECB and at the Fed than we have seen in some time. Look out for 2018.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief