Global| Apr 03 2013

Global| Apr 03 2013EMU Inflation Heads Lower...Following Growth

Summary

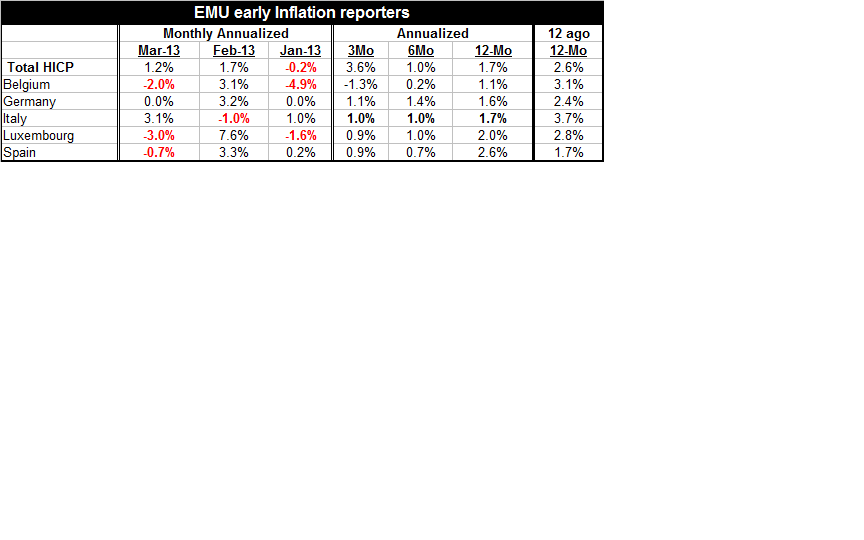

There is no arguing with the fact that EMU inflation is turning lower. One year ago EMU's Year-over-year inflation rate was 2.6% - high by the standards of the ECB but hardly bristling. In March of 2013, one year later, the pace is [...]

There is no arguing with the fact that EMU inflation is turning lower. One year ago EMU's Year-over-year inflation rate was 2.6% - high by the standards of the ECB but hardly bristling. In March of 2013, one year later, the pace is down to 1.7%.

Inflation which in Germany is unchanged month to month and up at a 1.1% pace over three-months has fallen the least over the past year, dropping by just 0.8 percentage points. That's the same as the drop in Luxembourg. The overall HICP has dropped its pace by 0.9 percentage points. Belgium and Italy each have sliced two percentage points off their respective Year-over-paces. The standard deviation in the year-over-year inflation among these five early reports is lower than it was one year ago, so the Community is achieving some convergence.

Although Spain's HICP fell by a large 0.7% in March that followed an even larger rise of 3.3% month-to-month in February. Spain is the only early inflation reporter to show a rise in inflation year-over-years as its pace gained by 0.9 percentage points. Spain is still held in the grip of austerity.

Among the troubled borrower group only Spain shows stubborn inflation. These data are only up to-date though February. Still the picture shows that for the most part the troubled borrowers are reducing inflation and at a solid pace- Spain is the exception. Greece's inflation rate is lower year-over-year by one percentage point, Portugal's is lower compared to a year ago by 2.8 percentage points, Ireland's rate is lower by just 0.3 percentage points.

By and large inflation is controlled in the Zone, the problem is that growth has been all but stopped to do it. It's a bit like stopping someone from bleeding by stopping their heart. You'd better be able to get it going again.

The issue for the Zone is how to re-ignite growth without backtracking on inflation progress or worsening the fiscal situation. And this has been a conundrum for the EU and ECB. The ECB has given as much help as it could- like the Fed maybe too much help. But that has not been the right kind of fuel. In the presence of austerity, monetary policy loses its bite. Inflation is not the problem in the Zone. Growth is the problem. Another problem in the Zone is not knowing what to do to reignite it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief