Global| Nov 27 2015

Global| Nov 27 2015EMU Index Holds Its Ground in November

Summary

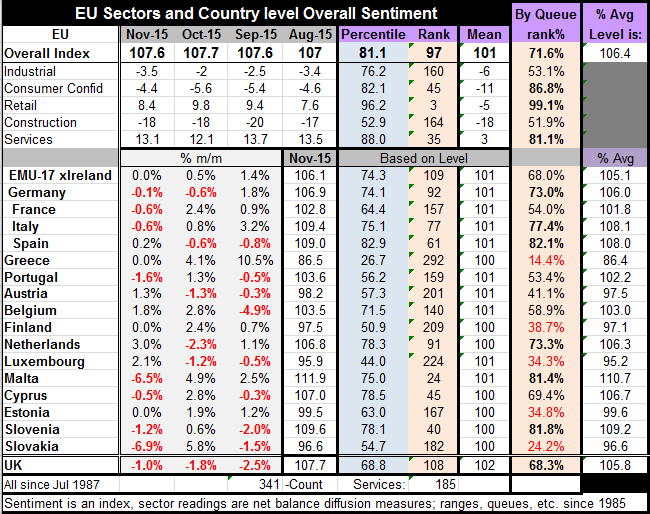

The EU overall sentiment index slipped this month while the index for EMU members was dead flat at last month's level. The EU index sits in the 71st percentile of its historic queue of data. The EMU index is a bit weaker, standing in [...]

The EU overall sentiment index slipped this month while the index for EMU members was dead flat at last month's level. The EU index sits in the 71st percentile of its historic queue of data. The EMU index is a bit weaker, standing in the 68th percentile of its historic queue.

The EU overall sentiment index slipped this month while the index for EMU members was dead flat at last month's level. The EU index sits in the 71st percentile of its historic queue of data. The EMU index is a bit weaker, standing in the 68th percentile of its historic queue.

On the month the EU index components show improvement in consumer confidence (to -4.4 in November from -5.6 in October) and in Services (to 13.1 from 12.1). The construction sector remains stuck at its -18 reading in November. The industrial sector weakened (to -3.5 from -2) and retailing dropped back (to 8.4 from 9.8).

The level of sector index stands ranges from mediocre (near 50) to extremely strong (near 100) No sector gives off a truly weak reading in relative terms (queue standings) although three sectors post outright negative readings. Retailing, despite its step-down this month, stands in the 99th percentile of its historic queue of data. It has rarely been stronger. Consumer confidence stands in the 86th percentile of its historic queue of data, a strong reading as well. Services post an 81st percentile standing. On the other hand, the industrial sector has a 53 percentile standing, barely above its historic median (which occurs at a rank standing of 50). Construction has a 51st percentile standing.

Of course, at an advanced stage of the business cycle we would expect to see - or to have seen - much stronger readings than most of these. But Europe has been troubled with austerity programs in place and a too-low rate of inflation. The real curiosity of the readings is the weak industrial sector since the euro exchange rate is so low. The extreme degree of competitiveness in EMU coupled with the weakness in EMU growth and in EMU export growth stands as testament to the weakness of the global economy.

In November economic indices fell in eight of 16 EMU member countries. Declines were scattered as the three largest EMU economies saw their indices fall as did tiny Malta. Greece, Finland and Estonia saw no change in their respective indices.

Five member nations have Sentiment readings that stand below the 40th percentile of their respective historic queues of data, they are: Greece, Slovakia, Luxembourg, Estonia and Finland.

Seven countries have readings in the top 40th percentile those include Spain. Slovenia, Malta, Italy, The Netherlands, Germany and Cyprus.

The weakest readings are generally in the smaller economies. Still there is a good deal of weakness scattered around; even France, the third largest economy in EMU, has only a 54th percentile standing.

The readings this month are for the most part a replay of last month with a bit of jockeying back and forth for position by individual countries. Last month only five countries saw their economic sentiment indices fall, while this month there are eight but without any impact on the overall index.

The 68th percentile standing for EMU tells the story of growth amid moderation. The indices for country rankings show a great deal of difference across countries. The ECB is still expected to uncork more stimulus in December. Everything in this report says it still is needed.

In data released today, EMU money and credit growth are moving in the right direction. In October the M3 monetary aggregate rose by 5.3% from 4.9% last month. Loans to households rose by 1.2% up from 1.1% last month. It is the same story with these financial variables as with real sector variables. Yes, they are moving in the "right" direction but not fast enough and not convincingly.

Meanwhile, the geopolitical risks have generally worsened over the last month as the Paris terrorist attacks have raised new skepticism about the risk of refugees. Belgium all-but-closed Brussels for several days to accommodate their manhunt. And, in the Middle East, Turkey shot down a Russian jet for airspace violations. Tensions there still run high; now Russia is taking steps. Coal shipments are being withheld from Ukraine and Russia is subjecting food imports from Turkey to great scrutiny. Risks have amped up and there has been no pick-up in growth to ease our minds about any potential spoil over into the real economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief