Global| Aug 14 2018

Global| Aug 14 2018EMU Growth: Is it on Shakier Ground?

Summary

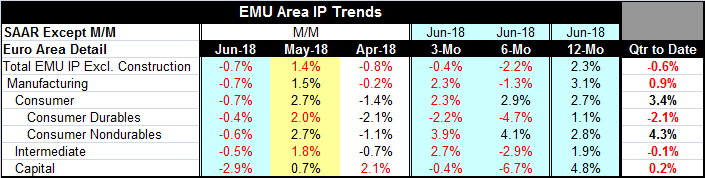

EMU industrial production fell 0.7% in June with the year-on-year pace at 2.3%. But in the QTD (quarter-to-date, which now refers to the full second quarter), output is falling at an annual rate of 0.6%, led by weakness in the output [...]

EMU industrial production fell 0.7% in June with the year-on-year pace at 2.3%. But in the QTD (quarter-to-date, which now refers to the full second quarter), output is falling at an annual rate of 0.6%, led by weakness in the output of consumer durables.

EMU industrial production fell 0.7% in June with the year-on-year pace at 2.3%. But in the QTD (quarter-to-date, which now refers to the full second quarter), output is falling at an annual rate of 0.6%, led by weakness in the output of consumer durables.

Intermediate goods show weak output in the QTD as outlook slips at a 0.1% pace and capital goods output is not driver of growth as it is up at only a 0.2% annual rate.

Despite what are relatively healthy year-over-year metrics for EMU IP, the shorter term results are sputtering and there are all sorts of reasons to not dismiss this unevenness.

The trade war, Brexit, recent geopolitical turmoil centered on Turkey and a planned ECB exit from its program of super stimulus, all raise warning flags on the outlook and create opportunities for ‘something’ to go wrong.

And there is also good old fashioned entropy.

Italy is showing strains as a bridge collapse in Genoa has resulted in a multitude of deaths. Years of budget cutting forced on Italy by German-inspired austerity has left its infrastructure in poor shape. You can ‘cheer’ the ‘success’ of austerity in lowering Italy’s inflation rate, but that has been done at a cost, a real cost. The bridge collapse is only the most recent evidence that this infrastructure neglect is a clear and present danger. The Five Star Movement ran on a platform of fixing the failing infrastructure. The EU Commission must approve the new government’s budget. Of course, Italy has budget constraints imposed by its membership in the EU as the EU Commission constantly reminds it. But Italy also has a banking sector that is living on borrowed time which is not good as Turkey begins to spiral out of control. Austerity meant not just cutting out the fat from the Italian budget’s diet, but ruining the nutrition and imparting the equivalence of osteoporosis to the very bones of the economic framework. Italy remains as one of the biggest threats to euro area prosperity and continuity and it’s not just because Italians are profligate. They are needy.

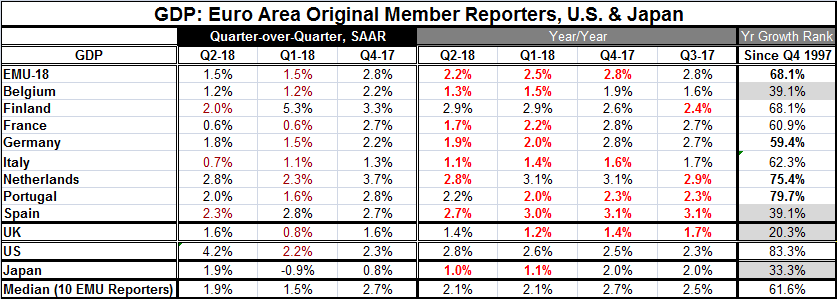

On the GDP front all of the original member current EMU reporters show GDP is expanding in the current quarter. There are quarterly decelerations in Finland, Italy and Spain. But more broadly there are decelerations in six of the eight reporting EMU members in terms of their year-over-year GDP growth rates. The EMU itself has slowed its year-on-year growth rate for three quarters in a row from 2.8% in Q3 2017 to 2.2% currently in Q2 2018.

New Jolt City...Is Goldilocks dead?

The new jolt to global growth prospects from troubles in Turkey has spread and has prompted investors to consider that the Goldilocks environment may be in its final daze. Argentina and Venezuela are in the news, not because of any link to Turkey but because it’s time to begin to look for trouble spots and so we are beginning to look at the lumps in the carpet instead of ignoring what we previously swept under it.

Of course, the whole of EMU sits on a shaky foundation since there is a lot of dissent about what countries are forced to do because of EU membership that has percolated to the surface over the issue of migrants. Of course, only the U.K. had a nationwide vote on EU membership and we know how that ended. But it is not the only EU member with a lot of dissent about how it is treated by the EU. This conflict often is referred to as concern over the rule by the elite- the stuff our elected officials or appointed officials set as policy. The existence of this sort of dissent has become clear in Italy. It popped to the surface then was suppressed at the time of the French elections. It undermined and has permanently crippled Angela Merkel in Germany. The EU and EMU still have their foundations sunk deeply into the ground where the tectonic plates are still shifting.

Turkey or trade could be the catalyst to bring out more problems. There is just no telling what might unravel next. India, a country that seemed to be doing well, may now be drawn into a destabilizing vortex of interest rate hikes. China, the truly big - or huge- enchilada, is showing signs of slowing but is not yet any kind of threat to growth. But China has its own festering issues. Policies launched by Donald Trump are shaking the global mercantilist tree. And what falls from it may be more than too-ripe fruit.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief