Global| Dec 07 2017

Global| Dec 07 2017EMU GDP Slows in Quarter

Summary

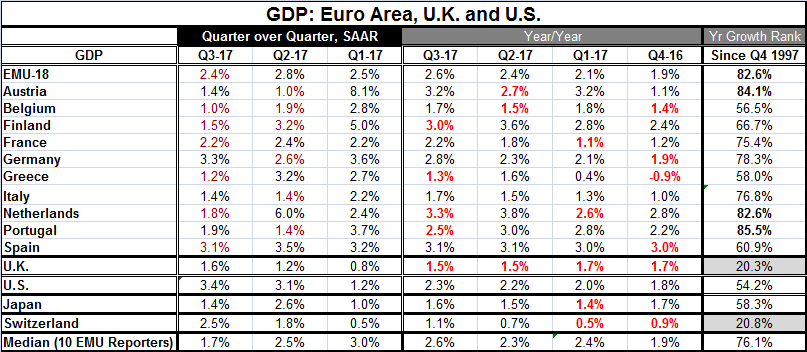

EMU growth rates are now 'finalized' for Q3 2017. There are no negative growth rates among these 'first' EMU members over the last three quarters and the last year-over-year negative growth rate among the group was in Q4 2016 for [...]

EMU growth rates are now 'finalized' for Q3 2017. There are no negative growth rates among these 'first' EMU members over the last three quarters and the last year-over-year negative growth rate among the group was in Q4 2016 for Greece, the last among first members. The median growth rate (unweighted) for these ten EMU members has fallen in each of the last two quarters, but the year-on-year median has risen not quite monotonically since Q4 2016 (and more broadly since Q1 2013). The EMU growth rates have performed more or less the same as the median on those same timelines.

EMU growth rates are now 'finalized' for Q3 2017. There are no negative growth rates among these 'first' EMU members over the last three quarters and the last year-over-year negative growth rate among the group was in Q4 2016 for Greece, the last among first members. The median growth rate (unweighted) for these ten EMU members has fallen in each of the last two quarters, but the year-on-year median has risen not quite monotonically since Q4 2016 (and more broadly since Q1 2013). The EMU growth rates have performed more or less the same as the median on those same timelines.

In the EMU, net exports added to GDP in Q3 as private consumption and public consumption both slowed on a quarterly basis. Exports outpaced imports by a small amount. Capital formation slowed quarter-to-quarter, as well. On a year-over-year basis, trade also stepped up its contribution to growth while private consumption and public spending were steady. Capital formation accelerated year-over-year. The EMU is still benefitting from export-led growth even though the global environment is still weak.

Growth in the EMU is firming and stabilizing. It has become more broad based which is the clear message from the manufacturing PMIs and perhaps, to a lesser extent, the message from the service sector PMIs as well. PMI gauges are measures of breadth rather than of strength and they have been rising.

Still, EMU member growth rates in the table, which feature the original members that have reported GDP (Luxembourg has not reported; plus we include Greece as a near-original member), show decelerations in their quarterly GDP rates for Q3. Only four members showed a stepped up pace and overall EMU GDP decelerated. In Q2, EMU GDP accelerated while only four members in this table (EMU membership is much broader than the table, of course) saw GDP growth accelerate. However, for year-over-year growth rates that are less fickle, there are four decelerations in Q3 2017 compared to six accelerations including an acceleration for the EMU overall in Q2. There was even better breadth in Q1 2017.

Year-on-year EMU growth has surpassed U.S. growth in each of the last seven quarters. However, U.S. growth has stepped up is pace considerably in just the last two quarters while EMU growth has ticked up then backed off.

In terms of relative standards, EMU growth is doing extremely well. Its year-on-year growth rate for Q3 2017 is in the top 82.6 percentile of all its growth rates back to Q4 1997. However, within the EMU, only Austria, the Netherlands and Portugal have growth rates in the top 80% of their respective data queues. They are doing well on growth rates that are beefed up over four quarters, but in each case they demonstrate withering quarterly results. As for the largest economies in the EMU, Germany's GDP has a solid 78th percentile standing, France has a 75th percentile standing, Italy has a 76th percentile standing, and Spain has a 60.9 percentile standing. Compare this to the U.S. whose year-on-year growth standing is only in its 54th percentile. Europe has been much closer to getting all it can from its economy while the U.S. has been performing in a relatively mediocre fashion.

Oddly, despite this mediocre U.S. performance - and over an extended period - economists judge the U.S. economy to be running at full tilt. This underlines the extent to which U.S. growth has bumped up against constraints, not because of rapid growth, but because of poor capacity expansion and labor force sluggishness.

Turning to EMU GDP trends, we are not surprised to find that the EMU has had substantially different impacts on different economics The table below fleshes that out.

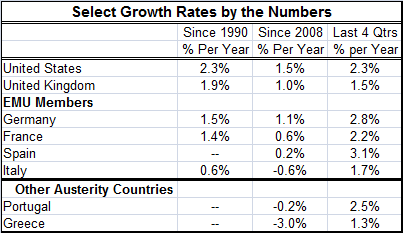

Since the EMU was formed, the U.S. and the U.K. have grown at a rate of 2.3% and 1.9%, respectively. Germany has averaged 1.5% growth. France has been at Germany's side with a 1.4% growth rate. Italy has expanded only by a pace averaging 0.6% per year. Since the financial crisis hit and some countries (Italy, Spain, Portugal and Greece) were forced into an austerity straight-jacket, the results are even more revealing. On this timeline, U.S. growth averaged only 1.5% as the U.K. averaged 1.0%. Germany averaged 1.1% as France gained just 0.6% per year. Spain averaged just 0.2% growth per year. And Italy still has not recovered to its Q1 2008 GDP level and averages a decline of 0.6% per year. Portugal and Greece, two other countries put on severe austerity diets, also have average negative growth rates for this period with Portugal at -0.2% and Greece averaging a stunningly weak -3.0%.

I'm not sure that this adds up to a happy ending just yet. But over the last four quarters U.S. growth is back to averaging 2.3%. German growth is all the way to a pace of 2.8% with France at 2.2%. Spain has come roaring back, averaging 3.1% with Italy at 1.7%. Portugal is averaging 2.5% growth and Greece is averaging 1.3%. Greece, of course, wins the kewpie-doll for its turnaround followed by Spain, Portugal and Italy.

Clearly, the global recession and the following financial crisis plus Germany's strict debt diet and no nonsense adherence to Maastricht deficit rules hit some EMU members much harder than others. It is not surprising that this period has spawned so much political turmoil in Europe. And it is interesting how hard the financial crisis hit the U.K. knocking its GDP growth rate nearly a full percentage point lower in just the post 2008 period compared to the full period. It is not surprising that populist (anti-elite) movements sprang up in Italy, Spain and Portugal or that the Catalan independence movement got traction during this period. Perhaps what is surprising is that even in Germany political movements have upset the apple cart and weakened Angela Merkel. This has happened even though the financial crisis seemed to have touched Germany less than other places and left it nonetheless much stronger.

Interestingly, the U.K. has been outgrowing EMU and Germany since the EMU was formed. It did take a hit from the financial crisis - that's not too surprising given that the financial sector was hit hard and that is a principle industry of London. Still, the U.K. outgrew Germany in this period. It is only in the last year with the U.K. adopting a Brexit attitude that U.K. growth has slipped. Clearly, EU membership had been good for U.K. growth as the U.K. outgrew Germany on the period. However, the decision to opt out of EU was not an economic one. The U.K. 'knew' there would be a cost in growth. And no one is yet sure what that cost will be. But Brexit is going to cost the U.K. dearly as some of its financial institutions are only now really finding out. The U.K. is paying a huge price to gain sovereignty over its borders and over immigration policy and as part of its Brexit deal it may have to cede some of that back still.

Although this is not part of the current Brexit discussion, it isn't clear that it is not the EU that overstepped its bounds on border issues since there is also a lot of dissention within the EU over its policies toward immigrants. 'Border countries' like Italy and Greece are bearing a disproportionate price, especially since other 'inland' EU members shut their borders to migrants that at one point had targeted Germany. Germany is accepting migrants but in a much more controlled way. In Italy and Greece, migrants simply hit the beach unannounced and have to be dealt with.

On balance, European growth seems to be well on the mend. It is still not clear what the potential for growth might be and how all the austerity may have improved member countries' potentials. But there are still legacy issues from the crisis mostly in the financial sector where there remain problems that have to be dealt with. We will learn much more about where Europe is as we see what sort of Brexit deal the U.K. can cobble together. For now it is very clear that the remaining EU members consider any EU governmental agencies that were in the U.K. 'the spoils of war' and they are scrambling to get them relocated in their own countries well as trying to attract U.K. banking business. Clearly, the post Brexit rule will be sure to red line the U.K. over much of banking. All in all, the U.K. treatment in the wake of its peoples' Brexit vote seems much more like the treatment of vanquished foe after a lost war. The U.K. will even have to pay 'reparations.'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief