Global| Nov 13 2020

Global| Nov 13 2020EMU GDP Growth Gets the Urge to Surge in Q3

Summary

EMU GDP and across the EMU made rousing gains in Q3. The percentage gains Q/Q exceeded the percentage losses for the previous quarter in every case except for Denmark and Finland. Despite that gap (and the illusory arithmetic of those [...]

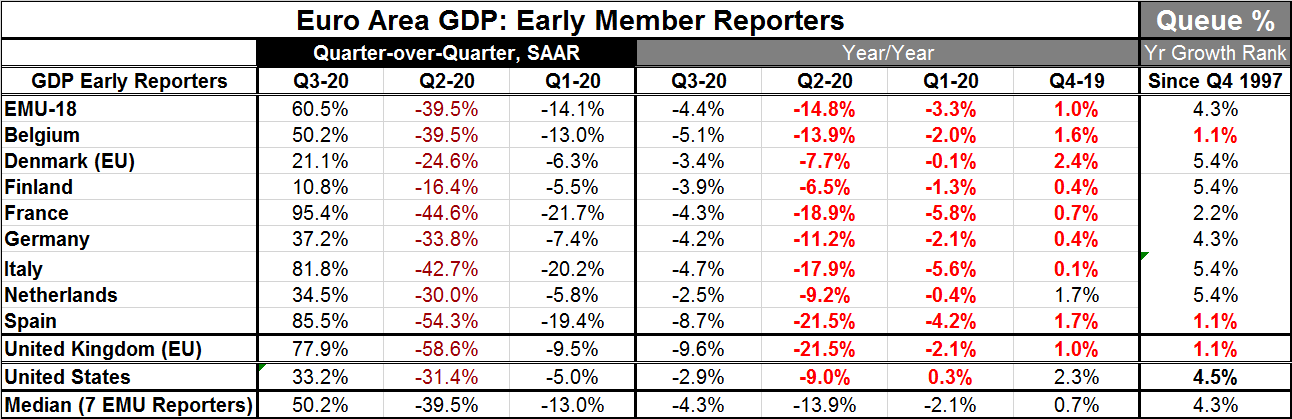

EMU GDP and across the EMU made rousing gains in Q3. The percentage gains Q/Q exceeded the percentage losses for the previous quarter in every case except for Denmark and Finland. Despite that gap (and the illusory arithmetic of those calculations), GDP in Q3 2020 lags behind GDP in Q4 of last year across the EMU by 4.4% and for each country in the table (not shown) by amounts ranging from 3% to 9.1%.

EMU GDP and across the EMU made rousing gains in Q3. The percentage gains Q/Q exceeded the percentage losses for the previous quarter in every case except for Denmark and Finland. Despite that gap (and the illusory arithmetic of those calculations), GDP in Q3 2020 lags behind GDP in Q4 of last year across the EMU by 4.4% and for each country in the table (not shown) by amounts ranging from 3% to 9.1%.

The persisting weakness also is borne out in the year-over-year calculations that show negative values across the board in Q3 2020. They are much reduced from the shortfalls reported in Q2, but they are nonetheless shortfalls. These year-on-year growth rates are plotted in the chart.

Even with the strong rebound on the quarter, GDP growth year-on-year carries a weak standing across the EMU with the strongest reading in their lower 5.4 percentile queue of historic results. There is no exception here. The queue percentage ranking stretches from a low of 1.1% in Spain and Belgium to a high of 5.4% in the Netherlands, Italy, Finland, and Denmark (an EU member). All of these are very weak readings. The year-on-year growth rates are still historically extremely weak and this is despite the strong – in many cases record strong- bounce backs in the quarter.

And yet challenges lie ahead

Despite the strong rebound of recovery in Q3, European economies face significant challenges. The virus has spread and the second wave is proving to be more of a problem in some ways than the first. And this is blunting the momentum generated by the Q3 rebound. The strategy is to fight ‘the spread’ with more localized and specialized actions to diminish the degree of economic disruption – still it is clear that the extent of the disruption will be substantial. Each country has its own approach. Portugal is taking further strong steps to contain the spread. The IMF is now projecting a less severe contraction for Spain in 2020 on the back of Spain’s strong Q3 rebound. France has a widespread lockdown in pace. Germany is using what is termed lockdown-light and is having success. In the United Kingdom, the National Institute of Economic and Social Research looks for 12% shrinkage in U.K. GDP in November following a weak estimated gain of 0.3% in October. It also looks for a 2.2% decline in U.K. GDP in the fourth quarter.

Outside Europe the virus also spreads

The United States is changing horses in midstream as Trump is out and Biden is in. Biden will not be making decisions that affect the economy until late-January. But until then, the same political forces from the last two years will remain in power and for now they still are not cooperating. However, India has launched another round of stimulus to fight off the impact of its national virus. There are places in the world that can get things done, but right now the U.S. does not appear to be one of them.

Meanwhile, the Biden transition teams and virus task force seem to have a lot of people on it that lean toward the preference of having lockdowns to deal with the virus spread. And we all know how costly that is and how much collateral damage it creates outside of its narrow virus containment objective. Time will tell what path Biden chooses, but the risk of more lockdowns could be mitigated by successful virus development.

The Future...

Of course, how all of these progresses is going to depend a lot on the development and quality of the vaccines that are now in progress. Even in a best case world, it looks as though it will take almost another year before Populations can be significantly immunized. For developing economies, it will probably take even longer. In the meantime, there are arguments about how to prioritize the inoculations among different groups looking at the young, the old, the vulnerable as well as frontline workers. A vaccine may be an eventual ‘panacea’ but it is going to take time getting there once vaccines are approved. The process of manufacturing, distribution and inoculation will require decisions on prioritization and logistics. The future remains in flux.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief