Global| May 15 2009

Global| May 15 2009EMU GDP Drops Sharply

Summary

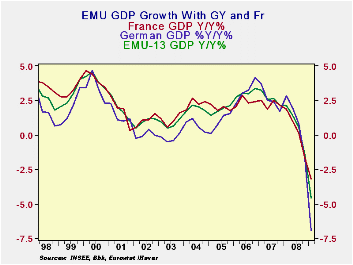

The EMU region’s sharp drop in GDP has turned out to be worse than expected for the region as well as for most countries. Germany is showing the deepest GDP drop since 1970. The drop that The Netherlands is experiencing is the [...]

The EMU region’s sharp drop in GDP has turned out to be worse

than expected for the region as well as for most countries. Germany is

showing the deepest GDP drop since 1970. The drop that The Netherlands

is experiencing is the sharpest drop in GDP since the end of WWII.

Greece is the sole county in this table with positive growth yr/yr.

GDP continues to decelerate across Europe. We knew these GDP

reports would be weak after viewing the weakness in industrial output

ahead of the release of this GDP report. Germany’s Q1 decline is so

large it is not looking for much if any further decline in GDP for the

rest of the year.

The Swedish Finance Minister Anders Borg has said that Europe

may be in need of some further stimulus. Of course Europe also labors

under the constraint of the Maastricht rules that restrict fiscal

deficits and cap ratios of government debt to GDP. Not only does Europe

lack a central fiscal authority comparable to its central bank, but the

fragmented nature of fiscal responsibility makes it hard for Europe to

be involved in fiscal stimulus in a coordinated way. Instead of a

central fiscal authority the Maastricht rules stand in to restrict

individual nations from going overboard with fiscal policy actions that

could create too many government liabilities that might undermine the

value of the euro. Of course recessions naturally put pressure on

Maastricht rules since growth slows or declines, pushing tax revenues

down at a time that social safety new spending rises. Countries that

have room under the Maastricht ratios can engage in fiscal stimulus in

times like theses, but often it is the high debt countries that are in

greater need of the stimulus and must risk running afoul of the rules

if they act.

This down turn has exposed problems in the Euro Area. The Euro

Area is asymmetric. Its Central Bank has a mandate for price stability

only. Meanwhile there is no fiscal authority to step in when things get

tough. In this cycle the ECB actually joined in on an coordinated

international rate cut with its inflation rate well over ceiling on the

basis of a forecast that inflation would drop (of course the spot oil

price had dropped sharply and that was not a very risky forecast at the

time). Still it was an action that seemed to violate the rule if not

the spirit of having and inflation ceiling. Europe has not been able to

confront the problem that only the ECB can move fast in a crisis yet

its mandate is price stability.

After seeing these GDP reports markets did not react very

strongly. The weakness in GDP was expected. The degree of weakness has

turned out to be a bit worse than expected. It sill is not clear what

steps Europe will take next and if more fiscal stimulus will be part of

the approach or not.

| Euro Area and Main G-10 Country GDP Results | |||||||

|---|---|---|---|---|---|---|---|

| Quarter over quarter-SAAR | Year/Year | ||||||

| GDP | Q1-09 | Q4-08 | Q3-08 | Q1-09 | Q4-08 | Q3-08 | Q2-08 |

| EMU-15 | -9.6% | -6.3% | -1.0% | -4.6% | -1.5% | 0.6% | 1.4% |

| Austria | -8.5% | -2.6% | -1.3% | -4.6% | 0.3% | 1.8% | 2.3% |

| France | -4.7% | -5.7% | -0.7% | -3.2% | -1.7% | 0.1% | 1.0% |

| Germany | -14.4% | -8.6% | -2.1% | -6.9% | -1.8% | 0.8% | 2.0% |

| Greece | -4.6% | 1.2% | 1.5% | 0.3% | 2.4% | 2.7% | 3.4% |

| Italy | -9.4% | -8.3% | -3.2% | -5.9% | -3.0% | -1.3% | -0.3% |

| The Netherlands | -10.7% | -4.7% | -1.8% | -4.5% | -0.8% | 1.8% | 3.4% |

| Portugal | -5.9% | -6.2% | -0.8% | -3.0% | -1.8% | 0.4% | 0.6% |

| Spain | -7.0% | -3.8% | -1.2% | -2.9% | -0.7% | 0.9% | 1.8% |

| UK | -7.4% | -5.9% | -2.8% | -4.2% | -2.0% | 0.4% | 1.8% |

| US | -6.1% | -6.3% | -0.5% | -2.6% | -0.8% | 0.7% | 2.1% |

| Japan | #N/A | -12.1% | -1.4% | #N/A | -4.3% | -0.2% | 0.5% |

| Switzerland | #N/A | -1.2% | -0.3% | #N/A | -0.1% | 1.3% | 2.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief