Global| Jul 31 2018

Global| Jul 31 2018EMU Early Growth Results Show Slowdown

Summary

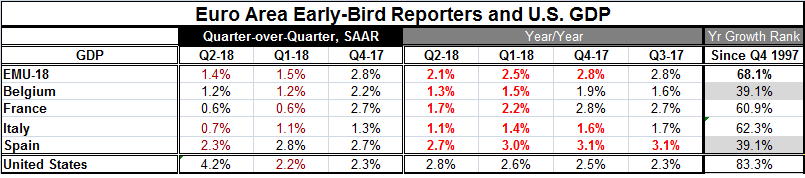

EMU area GDP slowed in Q2 2018 to an annualized pace of 1.4% from 1.5% in Q1. The year-on-year pace slowed to 2.1% from 2.5% previously. It’s the slowest GDP pace for the euro area since it gained 1.1% in Q2 2016. At this point, there [...]

EMU area GDP slowed in Q2 2018 to an annualized pace of 1.4% from 1.5% in Q1. The year-on-year pace slowed to 2.1% from 2.5% previously. It’s the slowest GDP pace for the euro area since it gained 1.1% in Q2 2016.

EMU area GDP slowed in Q2 2018 to an annualized pace of 1.4% from 1.5% in Q1. The year-on-year pace slowed to 2.1% from 2.5% previously. It’s the slowest GDP pace for the euro area since it gained 1.1% in Q2 2016.

At this point, there are only four reporters offering official early GDP estimates. These are Belgium, France, Italy and Spain; we have in this group three of the four largest EMU economies (Germany has not yet reported).

The table below flags slowdowns in year-over-year growth rates (compared to the previous quarter) with bold type and bright red text. The EMU year-on-year growth rate has slowed for three quarters in a row. Spain has slowed for four quarters in a row. Italy has slowed for three quarters in a row. Belgium and France each have slowed for two quarters in a row. In marked contrast, U.S. growth has speeded-up for eight straight quarters. But U.S. growth has only overtaken the EMU in the past two quarters on a year-over-year basis.

In terms of annualized quarterly growth rates, the U.S. is in a world of its own in Q2 2018. But policy is not made on these numbers. We do not know if strong U.S. growth will have staying power. And U.S. growth has been accelerating for some time. Its run may be over or not. In the case of the EMU and the EMU economies, it is the slowdown that catches our eye. Inflation in the EMU has gone to and above 2%, but core inflation is still lagging and oil is still a problem for headline inflation. But clearly there is less room for Mario Draghi to maneuver and just as clearly Europe is not as weak as it was, but it is not underpinned by growth acceleration as it would like to be.

Policy

The ECB is getting ready to dismantle its stimulus programs. And while growth is solid enough, momentum is poor. The Bank of Japan today announced a more flexible approach in the context of its same policy, holding to same policy goals and using the same policy tools. The Fed in the U.S. meets this week and is expected to stay on the sidelines before taking rates up again later this year. Central bank policy is in flux. Right now the U.S. seems to have the clearest path to higher rates, but the performance of the U.S. yield curve could become an issue for the Fed. For now the Fed is trying to deflect eyes from that signal, but as time goes on, rates go up and the curve flattens further that may not be possible. It seems to me at some point the Fed really has to confront directly the signal of the yield curve.

Growth evaluation

Meanwhile, the table gives us a way to evaluate growth. The far right hand column ranks the current year-over-year growth rate in a queue of data since 1997. This ranking shows that even at 1.4%, EMU growth ranks in the top 32% of all annual growth rates for GDP back to 1997. France and Italy, even with weak 1.7% and 1.1% annual growth gains, rank in their respective lower 60th percentiles. Belgium and Spain rank much lower, in their respective 39th percentiles each. These standings are below median growth rates for Spain and Belgium. The U.S. growth rate at 2.8% ranks in its 83rd percentile, higher only about 17% of the time.

The percentiles are a way to account for difference in structural growth rates for each economy. Spain has been logging what looks like good solid growth rates; yet, it is underperforming with growth rates below its historic median. Belgium has a weak looking growth rate and it is in fact struggling. Italy has a lower year-on-year pace than Belgium but it reflects more progress for Italy with a higher ranking but that is only because the Italian economy has been struggling so badly. Germany has not reported yet, but its GDP should be solid and its unemployment rate is low. German inflation is rising and above 2% and Germans are nervous about it. The ECB is going to be caught again between a rock and soft place as Italy does not need higher rates but Germany does. Welcome to the Twilight Zone...I mean the eurozone, of course.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief