Global| Dec 20 2017

Global| Dec 20 2017EMU Current Account Surplus Shifts Lower

Summary

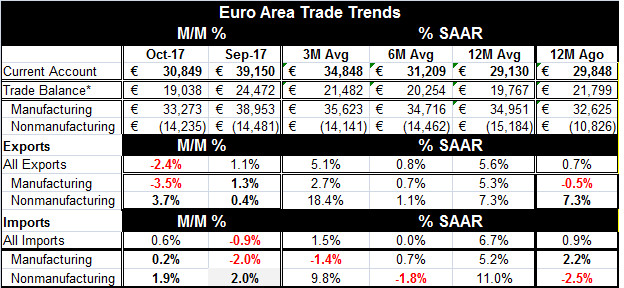

The EMU current account and trade surpluses contracted in October with the current account falling to 30.8 billion euros from 39.15 billion euros and the trade surplus falling to 19.0 billion euros from 24.5 billion euros. The balance [...]

The EMU current account and trade surpluses contracted in October with the current account falling to 30.8 billion euros from 39.15 billion euros and the trade surplus falling to 19.0 billion euros from 24.5 billion euros.

The EMU current account and trade surpluses contracted in October with the current account falling to 30.8 billion euros from 39.15 billion euros and the trade surplus falling to 19.0 billion euros from 24.5 billion euros.

The balance of trade on the manufacturing account has slipped to 33.3 billion euros in October from 38.95 billion euros in September. Nonmanufacturing trade sees a very slightly lowered deficit in October, lower by only 0.2 billion euros. Most of the current account adjustment is being made in the trade account but some also is in train in the income account of the current account.

Year-on-year the current account surplus is still slightly larger. However, year-on-year the trade surplus is slightly lower, standing at 19.0 billion euros compared to 21.8 billion euros 12 months ago. That balance shrinkage is totally in the realm of nonmanufactured goods where the deficit on trade expanded to 14.2 billion euros in October from 10.8 billion euros 12 months ago. The surplus on manufacturing trade, while lower month-to-month, is higher year-over-year, but by less than one billion euros.

Trends show that exports of manufactures are slowing down as the 12-month growth rate of 5.3% has withered to 2.7% over three months. Owing to volatile and still higher oil prices nonmanufactures show growth of 7.3% over 12 months that accelerates to an 18.4% annual rate over three months.

Import trends are quite different. Manufacturing imports for the EMU slow more sharply from a 5.2% pace over 12 months to a contractionary -1.4% pace over three months. Imports of nonmanufactures slow too, but only slightly from a pace of 11.0% over 12 months to a still vibrant pace of 9.8% over three months.

Imports in total at 6.7% growth do outpace exports at 5.6% over 12 months, but that margin is small. Meanwhile, the fall-off in the imports of manufactures raises questions about the state of domestic demand in the EMU where growth has been chronicled by a host of country specific as well as EMU-wide measures which appear to show that growth has been picking up. In such an environment, we would expect domestic demand to firm as well and that should lead to stronger imports, not weaker imports. The lower trade and current account surplus in the EMU suggests that the region is not as dependent on stimulus from its external trade accounts as it was last month, but there is little change year-over-year in that reliance. That is what the aggregate export and import trends tell us as well. However, the composition of exports and imports raises questions about the state of domestic demand since the imports of manufactures, while solid over 12 months, have weakened steadily over six months culminating in an outright decline over three months. In sum, while the overall tends for the EMU suggest some needed adjustment is in train other trends simply deny it. Here we see very different short-term and longer-term trends as well as compositional oddities such as weakening manufacturing imports.

Global growth trends are shifting. And as the IMF looks for China to focus more on repairing its composition of growth and reducing its dependence on debt, China's incoming data do not suggest that such a thing is in train. Nor did China's five-year party Congress seem to place the weight on this adjustment either.

However, central banks are looking ahead to hiking rates. Germany today reported its lowest PPI inflation in four months and reported a headline PPI that is up by only 2.5% over 12 months and a core PPI that is up by 2.3% over 12 months. German core PPI and core CPI trends remain flat or tending to weakness, despite what has generally been solid news on growth in Germany as well as in the EMU. But forecasts see higher inflation ahead.

In the U.K., the agents' survey is looking for faster wage growth but with Brexit in train and uncertainly about the decisions of foreign workers from other EU members on whether to stay in Britain or to leave as Brexit talks progress make the advance sorting out of labor market effects hard to do.

Among central bankers, generally, there is an assumption that growth will remain solid and perhaps get stronger. With that inflation pressures will return, or so forecasts opine. But in fact, there is very little to go on to suggest that this is actually what is happening. Still, markets are wary and there is a growing sense that the risk is to the upside. Yesterday Jens Weidmann roiled markets a bit with his forecast that wage pressures would be building in 2018. But this forecast emerged on the very same day that Q3 unit labor costs in the EMU decelerated from a 1.8% pace to a 1.6% pace. Granted... the future is not the past. But central bankers, especially in the U.S., have been very good at projecting a future to justify the rate change they want to make today. And despite those ongoing forecasts, real world data continue to defy central bankers' prognostications and expectations. Nowhere is that more evident than in the U.S. where inflation continues to languish below target and yet the Fed continues to ramp up rates...based on its 'expectations.' Is Europe in that same rut? Or will the Bundesbank's fears be founded?

Both exports and imports slow; exports decelerate more

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief