Global| Nov 28 2008

Global| Nov 28 2008EMU CPI in Near-Record Drop HICP is Barely Over the ECB Ceiling-Freeing Bank to Slash Rates

Summary

The Euro Area reported a dramatically deflated CPI (HICP, Harmonized index of consumer prices) for November. The index dropped its rate of inflation back to 2.1% from 3.2%, a huge deceleration (in one month!) for yr/yr inflation that [...]

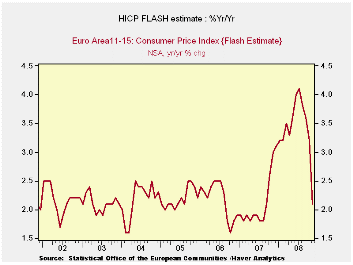

The Euro Area reported a dramatically deflated CPI (HICP,

Harmonized index of consumer prices) for November. The index dropped

its rate of inflation back to 2.1% from 3.2%, a huge deceleration (in

one month!) for yr/yr inflation that owes to the plunge in world oil

and energy prices. With a self-imposed limit for headline consumer

inflation of 2% the ECB can now feel it is no longer in violation of

the spirit of its ‘guideline’. And with inflation falling so sharply a

forward-looking expectation of being inside the target would be prudent

and reasonable.

Core inflation in the EMU is still not available. But the

history shows that that measure has been much better corralled overall.

Through October the three-month pace for core inflation was 2.4%

compared to 2.4% for Yr/Yr core inflation.

Of course the ECB has long since jettisoned any such technical

concerns of being in violation of its ceiling, as it has joined other

central banks in a round of international rate-cutting. The ECB

recognizes the downside risks but still has had this issue with the

inflation rate being so far over its ceiling. The drop in the rate this

month may be all the more important as the Federal Reserve in the US is

pulling out even more stops to lend to banks and issue liquidity as

well as to target mortgage rate reductions with a panoply of moves that

have some Fed critics warning of inflation consequences even as the

economy faces what could be a quarter of -5% real growth (annualized).

In such an environment the ECB at least has the comfort of

getting its inflation rate back close enough to target range that it

can again feel that it is making policy with some degree of comfort,

prudence and discretion.

Still, there should be no sense that all is well. The drop in

headline inflation merely gives the ECB its appearance of propriety

back - not its ‘Mo-Jo.’ The Federal Reserve in the US has made the most

moves of any central bank but part of its mix of policies has been to

provide swap facilities for dollars to aid central banks abroad.

Central banks are still ‘riding the tiger’. About a week ago US

Treasury Secretary Paulson dared to commit the ‘in-crisis’ error of

saying that banks had been stabilized, only to find that that they had

not as Citigroup saw its stock drop and a new special action by the

Fed/treasury was required. Clearly the financial situation remains

fragile though it appears to be less degenerative than it was. Now

policymakers are turning attention more to the economy. At a time like

this with Europe looking weaker and the German economy set to import a

good deal of weakness from trade as its exports drop, the ECB can use

an extra-measure of flexibility. It is hard to say that this drop in

inflation came ‘just in time’ but at least we can say ‘better late than

never’.

| Trends in EMU HICP; Flash Index | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Nov-08 | Oct-08 | Sep-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | -0.3% | 0.0% | 0.1% | -0.8% | 0.7% | 2.1% | 3.1% |

| Core | #N/A | 0.2% | 0.1% | 2.4% | 2.2% | 2.4% | 2.1% |

| Goods | #N/A | 0.0% | 0.8% | 1.4% | 1.4% | 3.5% | 2.6% |

| Services | #N/A | 0.1% | -0.7% | -1.3% | 2.5% | 2.6% | 2.5% |

| HICP | |||||||

| Germany | 0.0% | -0.3% | 0.2% | -0.4% | 1.1% | 1.5% | 3.3% |

| France | #N/A | 0.1% | 0.0% | -0.7% | 1.8% | 3.0% | 2.1% |

| Italy | -0.4% | 0.3% | 0.0% | -0.4% | 1.7% | 2.8% | 2.6% |

| UK | #N/A | -0.4% | 0.6% | #N/A | #N/A | #N/A | 2.1% |

| Spain | #N/A | -0.3% | 0.0% | -1.5% | 2.6% | 3.6% | 3.7% |

| Core:xFE&A | |||||||

| Germany | #N/A | -0.1% | 0.0% | 0.8% | 1.7% | 1.5% | 2.1% |

| Italy | #N/A | 0.5% | 0.0% | 4.6% | 3.0% | 3.0% | 2.1% |

| UK | #N/A | #N/A | 0.0% | #N/A | #N/A | #N/A | 1.8% |

| Spain | #N/A | 0.1% | 0.1% | 2.4% | 3.1% | 2.9% | 3.1% |

| Blue shaded area data trail by one month. | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief