Global| Oct 26 2017

Global| Oct 26 2017ECB Meets and Makes Plan to Reduce Purchases; Germans Are Hot But Money and Credit Are Not

Summary

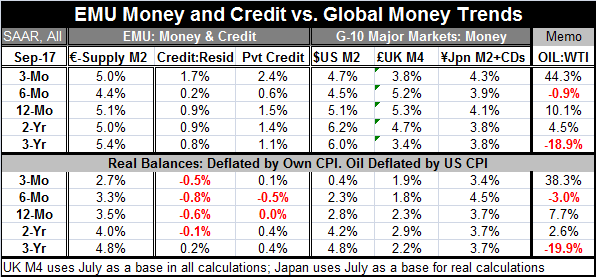

The chart shows that year-on-year growth rates for money and credit flows in the EMU have stabilized at less-than-strong growth rates. Both have steadied over the past year with money growth at a pace of about 5% and credit growth at [...]

The chart shows that year-on-year growth rates for money and credit flows in the EMU have stabilized at less-than-strong growth rates. Both have steadied over the past year with money growth at a pace of about 5% and credit growth at a pace of 1.5% for private credit. In real terms, credit growth has been flat or even contracting. Money growth in real terms has been at a 3.5% pace. Obviously, the growth in nominal money supply is more than sufficient to support economic growth, but there is a down shift in monetary velocity that is robbing even 5% nominal money growth from creating much stimulus. While some recent ECB comments have looked favorably at some categories of credit that have picked up, in the overall scene the gruel is thin. There is not much here to cheer about and that is the main reason that the ECB is so tentative in legging out of its stimulative policy.

The chart shows that year-on-year growth rates for money and credit flows in the EMU have stabilized at less-than-strong growth rates. Both have steadied over the past year with money growth at a pace of about 5% and credit growth at a pace of 1.5% for private credit. In real terms, credit growth has been flat or even contracting. Money growth in real terms has been at a 3.5% pace. Obviously, the growth in nominal money supply is more than sufficient to support economic growth, but there is a down shift in monetary velocity that is robbing even 5% nominal money growth from creating much stimulus. While some recent ECB comments have looked favorably at some categories of credit that have picked up, in the overall scene the gruel is thin. There is not much here to cheer about and that is the main reason that the ECB is so tentative in legging out of its stimulative policy.

Not much money surprise from global money supplies

Not much money surprise from global money supplies

While globally PMI gauges continue to post firm-to-strong readings, key monetary center countries are showing a steady-as-she-goes tact with no pick up for monetary stimulus. Japan is a minor exception here with a very gradual upturn in its money growth rate in train. But in the EMU, M2's growth rate has been flat. In the U.K., M4 is now decelerating relatively sharply. And in the U.S., money growth has been eroding around last year, coinciding with the Federal Reserve's commencement of rate hikes. In fact, the divergence in year-over-year money growth rates is extremely small. Since 1991, there is only one two-month period in early-1998 when money growth rate divergence has come anywhere close to the consensus pace of monetary expansion that exists today in the EMU, the U.S., Japan, and the U.K. Despite this convergence, credit expansion is quite varied in these economies.

At its policy meeting today, the ECB made the following announcements (ECB monetary policy decisions here).

ECB on rates: The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council continues to expect the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Nonstandard policy: As regards non-standard monetary policy measures, purchases under the asset purchase programme (APP) will continue at the current monthly pace of 60 billion euros until the end of December 2017. From January 2018 the net asset purchases are intended to continue at a monthly pace of 30 billion euros until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the APP in terms of size and/or duration.

Reinvestment: The Eurosystem will reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

Commentary on ECB action/statements

The ECB is not making any change or announcing plans to make any changes in interest rates. It will reduce its purchase program amount from January 2018 and will extend purchases at the reduced pace through September (as always depending on events). Repurchase programs will remain in place to maintain the size of the portfolio apart from the phase down activity.

Summing up

Despite the fact that this is a step to reduce ECB intrusion into the capital markets, German commentators are not happy that the program is going to be kept even though it is being shrunk. However, the ECB has undertaken its decision relative to events conditions in the EMU and should events change these policies could be altered as well. Inflation continues to undershoot the ECB's goal. Of course, there is unhappiness with these programs in Germany, partly for ideological reasons and partly because of German economic circumstances. German inflation is now one of the higher rates among EMU members and the German economy shows evidence of having little slack left with a record low rate of unemployment since German reunification. However, EMU-wide conditions show more resource and labor market slack than what exists in Germany alone.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief