Global| Apr 23 2013

Global| Apr 23 2013e-Zone PMIs Remain Under Pressure

Summary

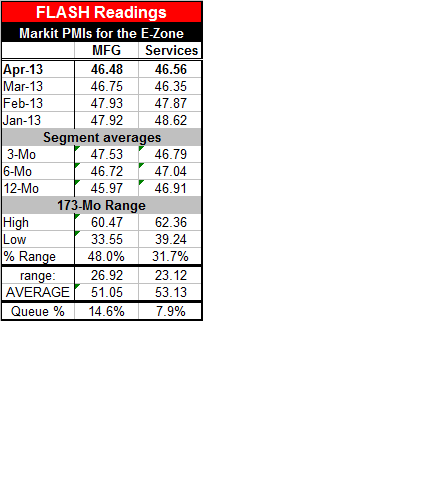

The euro-zone's private sector economy remains under pressure in April. The manufacturing PMI index fell slightly to 46.48 in April from 46.75 in March. At this level the manufacturing index historically has been weaker only about [...]

The euro-zone's private sector economy remains under pressure in April. The manufacturing PMI index fell slightly to 46.48 in April from 46.75 in March. At this level the manufacturing index historically has been weaker only about 14.6% of the time.

The euro-zone's private sector economy remains under pressure in April. The manufacturing PMI index fell slightly to 46.48 in April from 46.75 in March. At this level the manufacturing index historically has been weaker only about 14.6% of the time.

The services index, like the manufacturing index, continues to point to contraction as it hovers below the output-static level of 50. However, the services index improved very slightly in April moving up to 46.56 from a level of 46.35 in March. At its April level the service sector PMI has been weaker historically only 7.9% of the time.

Interestingly, using the monthly recession designation from ECRI, the German economy has been in recession 22% of the time during the period that the both the MFG and Services PMIs have been available for EMU. The EMU indices both are at levels that occur less often than Germany is in recession. That puts the extreme degree of weakness in perspective especially as it lingers.

Both of these EMU-wide indices are quite weak. Markets have been pointing to the release of these indices, hoping that they would show that some of the pressure on the euro economy is being relieved. But there's no sign of that in these reports.

A report for China continues to show headwinds for the Chinese economy with the manufacturing sector that is just barely showing expansion in terms of the PMI lexicon. China is engaged in a very difficult process of trying to wean its economy off of a dependence on foreign demand (alternatively: exports). With growth and debt problems such as those that exist in Europe and in the United States China's strongest (export) markets have turned flat. China's amazing output machine needs growing demand in order for it to have a reason to continue to churn out all that product. China's challenge for this year was to begin the transition to developing its own domestic demand. That process is not going smoothly. In order to develop its domestic demand China is going to have to pay its workers so that they can afford to buy what they produce. And, as China pays its workers enough to make them a force in domestic demand, it will raise their wages enough to damage China's international competitiveness. That's the rock and the hard place that China's between. It has come about partly because of the debt and growth problems in Europe and in United States that in turn came about in part because of aggressive Chinese exporting and because of China's reluctance to let its exchange rate play its proper role as an adjustment mechanism (to rise in value)

Problems in Europe continue to have several different dimensions. One of the ongoing stories is that Napolitano has been reelected as Italian President and he will now make another attempt to form a government there. In France the property market in Paris has seized up after what has been a very sharp run-up in prices. Prices now are off their peak by a tiny amount and property sellers are largely unwilling to cut their prices substantially to sell, while buyers don't wish to step up to the plate to buy. We can't help but wonder whether the new focus in France on taxing the rich, even though it failed, hasn't put the fear of the tax man into the wealthier Frenchman. In addition France is part of the Eurozone and can see the problems swirling all around it as well as the increasing difficulties France itself is having while trying to negotiate growth and maintain its budget pledge. France has been failing to meet its budget targets despite the fact that most of the extra taxing was used to cushion the blow to spending. France should be asking and wondering: what's next?

In Germany both the manufacturing and the services indices backtracked this month. The German manufacturing gauge fell to 47.9 from a level of 49.0 the previous month. The German services sector index fell to 49.2 50.9 the previous month. Now both sectors are pointing to declines in the German economy. The German MFG index is weaker than this only 23% of the time nearly the same as the period of time the German economy has been in recession since the two-sector PMI gauges have been available. The services PMI for German is also on the recession cusp as it has been lower only 20.3% of the time.

Spain's central bank is providing guidance for the first quarter; it is looking for a further contraction in GDP growth.

After all the troubles that the euro-zone is having, things are still not getting better. This distress has not been a down-payment on a remedy. The Zone still does not have a plan that will allow it to stay together and permit growth. It does not have a plan that will allow it to stay together and heal the competitiveness divergences that have developed. Instead, it continues to have deep North-South divisions and growing domestic schisms across many of its countries including those with strong as well as with weak finances.

The European crisis has not brought Europe closer together. The European crisis has driven wedges into splits that already existed and has worsened them. The weak countries blame the strong countries for exploiting them. The strong countries blame the weak countries for not having had responsibility.

Oh-zone or e-Zone? No one seems to be looking at the euro-zone and agreeing that they made a mistake while constructing it with an eye to proposing changes that can fix the Zone and make it work. All the proposals made to date show ways 'other countries' can address their problems while keeping 'my country' out of it. The fact that a cooperative tact is not being taken strongly suggests that the euro-zone is living on borrowed time. The fact that no nation wants to be the one that causes the euro-experiment to fail is only stretching out it's time on its deathbed. Unless attitudes among the rich or the poor changed dramatically, or unless they somehow agree that what they do have in common is worth some MUTUAL sacrifice and meet in the middle, the euro-zone is destined to be another failed economic experiment. In fact, it already is a failed economic experiment. The question is whether anyone cares enough about it to try to patch it together and make it work or whether it's time to just throw it in the rubbish bin.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief