Global| Jan 22 2009

Global| Jan 22 2009E-Zone Orders Drop Sharply...Again

Summary

E-Zone orders are dropping sharply in November. Based on some more topical country level reports, it is not surprising that the EMU orders series made another sharp fall – and more those lie ahead. Today, in fact, the UK CBI survey of [...]

E-Zone orders are dropping sharply in November. Based on some

more topical country level reports, it is not surprising that the EMU

orders series made another sharp fall – and more those lie ahead.

Today, in fact, the UK CBI survey of industry posted another sharply

weaker result with its up minus down diffusion index falling to -48 in

January compared to -35 in December. That’s right, in January.

Diffusion data are generally out a month or more ahead of the actual

underlying series that they describe and, as such, they provide a road

map of where we are headed. Still, the variables themselves tell the

actual story of industry.

In November the EMU series is telling us of increased pain in

the zone. The carnage is widespread. For Germany, France, Italy and the

UK Yr/Yr orders are dropping in November by 20% or more from November

of one year ago. In the quarter to date (Q4) the country level growth

rates for orders are more like a negative 50% at an annual rate

compared to Q3 2008.

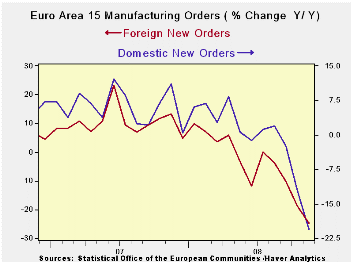

The weakness is spread more or less equally across domestic

and foreign orders in the EMU series. Foreign orders are down by more

over 12-months but the drop in November is worse for domestic orders.

For the moment we are in the worst of the grip of the

downturn. As we admit this, the international banking crisis is not

getting any better. The ‘Dutch boys’ with their fingers in the dikes

are calling out for more recruits --for more stop-gap plans. Others are

crying out for a more permanent solution and for mindful attention to

what all this interventionism will mean for the future. The US has just

completed its transition to new leadership. Japan is eroding faster

after showing some resilience. The strength in the yen is finally

creating more distress there. The data from the industrial sector in

EMU are telling. The pressure on the financial sector is bad and it is

going to get worse. We were already in a financial mess before this

recession began. Now the recession is global in nature and it is going

to spawn and spread the usual credit mess that comes hand in hand with

recession- and this recession is severe. So be prepared, because things

will get worse... That is the main message from the day’s weak

industrial data in Europe.

| E-zone-13 and UK Industrial Orders And Sales | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Nov-08 | Oct-08 | Nov-08 | Oct-08 | Nov-08 | Oct-08 | ||

| Ezone Detail | Nov-08 | Oct-08 | Sep-08 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| MFG Orders | -4.5% | -5.7% | -5.4% | -47.3% | -40.3% | -27.6% | -28.3% | -21.0% | -15.2% |

| MFG Sales | -0.9% | -1.9% | -1.9% | -17.0% | -17.0% | -10.5% | -8.6% | -2.6% | -1.7% |

| Consumer | 0.1% | 0.0% | -0.2% | -0.3% | -1.4% | -0.7% | -1.2% | -0.5% | -0.6% |

| Capital | -0.3% | -0.6% | -0.6% | -5.8% | -6.7% | -5.3% | -5.2% | -1.5% | -1.2% |

| Intermediate | -7.0% | -5.5% | -6.0% | -53.6% | -38.7% | -28.6% | -26.9% | -20.5% | -12.2% |

| Memo:MFG | |||||||||

| Total Orders | -4.5% | -5.7% | -5.4% | -47.3% | -40.3% | -27.6% | -28.3% | -21.0% | -15.2% |

| E-13 Domestic MFG orders | -7.0% | -5.5% | -6.0% | -53.6% | -38.7% | -28.6% | -26.9% | -20.5% | -12.2% |

| E-13 Foreign MFG orders | -3.5% | -6.9% | -5.9% | -48.9% | -46.5% | -30.3% | -32.3% | -24.8% | -18.9% |

| Countries: | Nov-08 | Oct-08 | Sep-08 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| Germany (MFG): | -7.2% | -7.1% | -8.0% | -60.3% | -39.7% | -37.5% | -29.6% | -24.4% | -16.6% |

| France(Ind): | -5.7% | -11.8% | 0.6% | -50.8% | -55.2% | -33.7% | -38.5% | -25.5% | -18.8% |

| Italy (Ind): | -6.3% | -6.6% | -3.8% | -49.7% | -39.0% | -27.2% | -23.2% | -21.1% | -12.1% |

| UK (Engineering Ind): | -8.4% | -24.0% | 28.8% | -35.6% | -35.3% | -38.9% | -35.2% | -21.7% | -8.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief