Global| Feb 13 2018

Global| Feb 13 2018Dutch Retail Sales Lose Traction As Economic Transition Looms

Summary

Dutch retail sales are volatile, but the series on retail sales has always had a high degree of volatility. Still, even by these standards, Dutch retail sales are volatile. The six-month volatility in sales is the highest it is been [...]

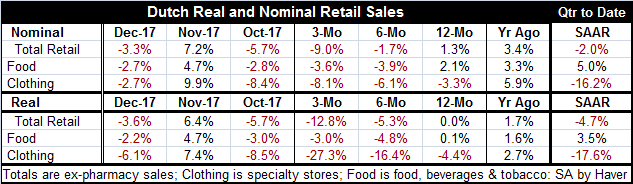

Dutch retail sales are volatile, but the series on retail sales has always had a high degree of volatility. Still, even by these standards, Dutch retail sales are volatile. The six-month volatility in sales is the highest it is been since September 2012. In the last three months, Dutch sales had fallen by 5.7% in October, risen by 7.2% in November, fallen by 3.3% in December. The volatility in real sales has been just about as bad.

Still, the hallmark of Dutch sales trends now is not just volatility but ongoing weakness. Dutch sales are falling at a 9% annual rate over three months and off at a 1.7% annual rate over six months. They are up by just 1.3% over 12 months.

In real terms, the progressive deterioration is even more severe with the pace of sales eroding consistently from flat over 12 months to declining at a 12.8% annual rate over three months.

Over the quarter-to-date, Dutch sales are off a 2% rate in Q4 2017 while real sales are falling at a 4.7% annual rate.

Despite the volatility and weakness in overall spending trends, consumers report that all is well. Consumer confidence has flattened out but remains at a relatively high level in the neighborhood of its strongest readings since 2007. And the willingness to buy indicator in that report has been on an up-cycle tear since late-2013 and now stands at a reading that is among the very highest readings since 2007. Yet, actual sales are contracting.

The Dutch economy is doing well in terms of the EU Commission indexes and in terms of the Markit manufacturing PMI. Imports and exports in and out of the Dutch economy are still growing, but growth is gradually slowing to single digits.

The Dutch consumer is not abnormal

There is a sense in the indicators that conditions are better than what we see in retail sales, but it's not just a case of 'indicators' being out of sync with more traditional reports that actually survey firms and assess the precise value of their contribution to growth, as even Dutch industrial output has remain strong. Still, the recent volatility in consumption and the weakness in retail sales remain as missing elements to a truly strong picture. Topical retail sales reports in the EMU, Germany and the U.K. all have recently weakened. So far, this is the same kind of troubling recovery that it has been for a while. It is one in which output measures are relatively strong and where consumption measures continue to show lethargy, weakness or simply failure to keep pace with output growth. That is something to be concerned about since everything that is made and sold has to be sold to someone. And capital spending will only take you so far.

Beyond the Dutch and Europe

In Europe conditions are further handicapped by constraints on the government through Maastricht debt and deficit parameters. The U.S. has no such rules (although it had some such guidelines that it has chosen to blow up) and we are about to see if the U.S. is going to let the dogs out and allow fiscal policy to run rampant after a period of some restraint. Even though the U.S. has showed some fiscal restraint in recent years (apart from the adoption of fiscal stimulus when mired in the Great Recession), it has failed to deal with its off balance sheet liabilities. What the Trump Administration is proposing for infrastructure spending coupled with the recently adopted Democrat-Republican debt deal that kept the government open has put the U.S. economy on a much more dangerous long-term fiscal course. It's no wonder markets are getting unsettled. The government has also raided the balance sheet at the Fed. You don't even need to look at market instability to begin to recognize how dangerous the times have become. And Fed officials want to claim that their outlook is unchanged by the market volatility. Maybe they need to more broadly scan the horizon. If the U.S. goes to fiscal excess and has to clamp down, the global repercussions will be much worse than those transmitted from Europe when Maastricht rules were suddenly and forcefully observed.

It is not a good time to be drawn into optimism by the boastful government officials or by a new willingness to skate closer the edge of a debt disaster. With a new finance minister in Germany, the application of German vigilance in Europe might be reduced as well. Central banks still are not getting traction to reach their inflation goals. But that is not to say that conditions can't change. It is only true that such a period of change is not underway yet. But even in the absence of rampant consumer spending, the government itself can provide all the fuel you need to set an economic wildfire if the rest of government will let it. Markets seem to sense the cusp of change and fear it. China remains in full reflation still being led by great debt creation. The U.S. is threatening to join it. The risk to inflation does not come from the labor market, believe me. But that doesn't mean that it isn't growing. Fiscal policy is the new bogeyman.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief