Global| Jul 13 2015

Global| Jul 13 2015Dutch IP Growth Year-Over-Year Is on Withering Trends...and Dutch Treat for Greece

Summary

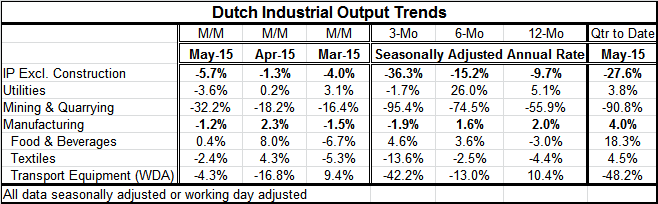

Dutch manufacturing IP has just made its third consecutive gain year-over-year. However, overall IP excluding construction (the headline series) is lower year-over-year for two months running. Shorter term trends, those inside one [...]

Dutch manufacturing IP has just made its third consecutive gain year-over-year. However, overall IP excluding construction (the headline series) is lower year-over-year for two months running. Shorter term trends, those inside one year, for overall Dutch IP actually are looking quite poor. The headline series for IP is decelerating sequentially with its three-month growth rate at -36% (SAAR). Manufacturing is decelerating, too but less dramatically. Manufacturing slips to a 12-month pace of 2%, then to a six-month pace of 1.6% and then to a three-month pace of -1.9%. Even for manufacturing series, the year-over-year gains do not look like the right signal for where it is headed next.

Dutch manufacturing IP has just made its third consecutive gain year-over-year. However, overall IP excluding construction (the headline series) is lower year-over-year for two months running. Shorter term trends, those inside one year, for overall Dutch IP actually are looking quite poor. The headline series for IP is decelerating sequentially with its three-month growth rate at -36% (SAAR). Manufacturing is decelerating, too but less dramatically. Manufacturing slips to a 12-month pace of 2%, then to a six-month pace of 1.6% and then to a three-month pace of -1.9%. Even for manufacturing series, the year-over-year gains do not look like the right signal for where it is headed next.

Of course, the oil sector figures in strongly to the Dutch economy. The mining and quarrying sector is showing colossal declines with a -95% pace (SAAR) over three months. Textiles and transportation equipment are showing full bore decelerations as well.

In short, the Dutch industrial sector is not looking very healthy. In the quarter-to-date, the headline IP series is falling at a 27% annual rate, but manufacturing is marking a positive 4% rate of growth.

Dutch Treat with Greece

No discussion of any European country is complete today without mentioning the over-the-weekend marathon negotiating session that appears to have produced a deal with Greece. I call this deal a `Dutch Treat' since each side will have to pay its own way. The EU group (yes, including Germany) will put in more money, although Germany did not want to do so. The Greeks will have to pass reams of new legislation memorializing and formalizing the austerity to which they will be yoked liked cows in the field for years to come.

I say that the weekend negotiations appear to have produced a deal because each side must ratify at home what has been agreed in its collective meeting. Tsipras, the fiery Greek leader, must sell Greece's total capitulation to even more draconian demands than before to a party and people that had stood against the continuation of austerity let alone a ratcheting up of it. Germany and Finland, among other members, must get their national parliaments to endorse further disbursements to Greece. Each side is pitching in here, but the Greeks will have a very heavy burden and their debt-to-GDP ratio would be a black diamond were it a ski slope. Greece has got no debt forbearance at all.

So life goes on. But the Euro-deal must yet be ratified in all parliaments and therefore we should not drink too may toasts to a successful conclusion until everyone has signed on their respective dotted lines. The Greeks will have little to celebrate as their living standards will fall in the hope that in the future they can rise sustainably. But that future is too far off for any politician to successfully sell it at the polls today. Greece has a very bitter pill to swallow. Stay tuned. The fat lady has yet to sing.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief