Global| Aug 25 2017

Global| Aug 25 2017Durable Goods Orders Ride the Wild Monthly Roller Coaster to Nowhere; Moderate Expansion Continues Under the Thin [...]

Summary

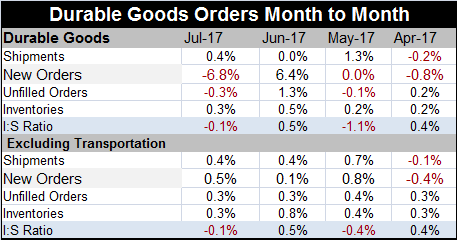

U.S. durable goods order plunged 6.8% in July, more than offsetting their 6.4% surge in June. Excluding transportation orders gained pace, rising by 0.5% in the month after gaining a thin 0.1% in June. Orders (ex-transportation) are [...]

U.S. durable goods order plunged 6.8% in July, more than offsetting their 6.4% surge in June. Excluding transportation orders gained pace, rising by 0.5% in the month after gaining a thin 0.1% in June. Orders (ex-transportation) are now up for three months running. Shipments are also rising at a moderate pace both overall and excluding transportation. Ex-transportation backlogs have a steady 0.1% gain per month in progress. The inventory-to-shipment ratio (ex-transportation) is seesawing.

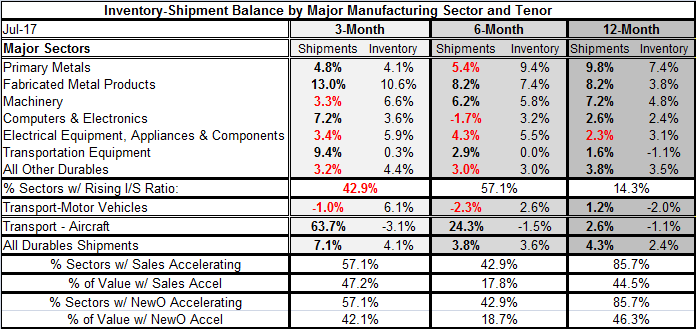

Digging inside the report and focusing on trends as depicted by sequential growth rates from 12-month to six-month to three-month, we find that inventory-to-shipment ratios are mostly contained with less than half the sectors showing inventories growing faster than sales on most horizons.

At the bottom of the table, several breakdowns provide insight into relevant trends. Overall durable goods shipments are generally stable over longer periods then accelerating with a step up in the pace over three months to a 7.1% annualized rate compared to growth rates of about 4% over the other horizons. However, aircraft is a big part of that development (three-month shipment pace up a 63.7% rate, annualized). Looking at the diffusion of sales acceleration (% sectors with sales accelerating), we find that sales are accelerating in 57.1% of the sectors over three months, in 42.9% over six months, and over one year orders accelerate in 85.7% of sectors. Those sector results are pretty solid-looking metrics. However, when we weight the results for sector size, we find that the value of sales in sectors that are accelerating accounts for only 47.2% of shipments over three months, 17.8% over six months and 44.5% over 12 months. Acceleration is not really as important or broad-based when size is accounted for. It is mostly the smaller sectors that are doing the best for now.

We make the same pairings of calculations for orders and find the same set of results again: that the order acceleration looks good when we count by sector and yet it is much less important when we weight the results by industry size. Over three months orders are expanding in 57% of the sectors and those sectors have 42% of the sectors' orders. Year-over-year the results show orders accelerating in 85% of the sectors with only 46% of total orders. These percentages are identical percentages for unweighted orders and shipments. This is a statistical oddity that occurs because we look at only seven sectors, limiting the range of options for unweighted diffusion. The value-weighted results show more diversity since value by sector is more varied. Still, the message is also that what is happening with shipments and with orders is very similar. The value of new orders accelerating is under 50% on all horizons as it is for shipments. Acceleration is not yet a widespread phenomenon.

On balance, these metrics point to a sector that is still expanding, but there is not convincing evidence of acceleration. The headline is much more volatile than the guts of the report which tell a more consistent story of ongoing and mild growth. If I could summarize things inductively, I would note what is NOT happening: sales are not broadly accelerating and inventories are not getting out of kilter relative to sales. This leaves the salient trends somewhere in the middle creating neither excitement nor apprehension. Industry remains is a sort of sweet spot if mild growth is a satisfactory objective. As always, all durable goods numbers are in nominal terms.

Financial Stability a Decade after the Onset of the Crisis from the Federal Reserve Board is available here.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief