Global| Jul 10 2017

Global| Jul 10 2017Do OECD LEIs Support the Policies Being Considered by Global Central Banks?; OECD LEIs Show Stability But Not Momentum

Summary

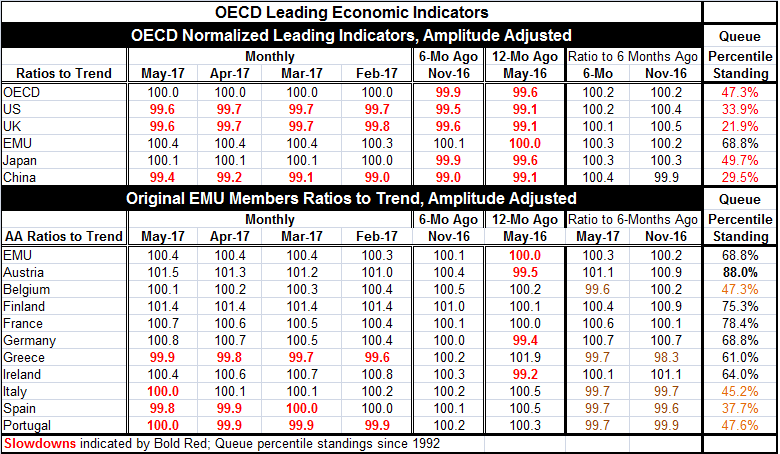

In May the overall OECD LEI logs a standing of 100, unchanged from April (and March, February and January). That's a long string of standstill and with the gauges right on top of the neutral standing at 100. These gauges are [...]

In May the overall OECD LEI logs a standing of 100, unchanged from April (and March, February and January). That's a long string of standstill and with the gauges right on top of the neutral standing at 100. These gauges are constructed so that readings above 100 indicate better than average growth while readings below 100 signal worse than average growth. The OECD likes to use the six-month change in the index as its most reliable signal. On that basis, the overall OECD index is slightly stronger over six months than it was six months ago. Still, the ratio of the current index to six-month ago at 100.2 (that is 1.002 times 100) shows only a minor twitch higher.

In May the overall OECD LEI logs a standing of 100, unchanged from April (and March, February and January). That's a long string of standstill and with the gauges right on top of the neutral standing at 100. These gauges are constructed so that readings above 100 indicate better than average growth while readings below 100 signal worse than average growth. The OECD likes to use the six-month change in the index as its most reliable signal. On that basis, the overall OECD index is slightly stronger over six months than it was six months ago. Still, the ratio of the current index to six-month ago at 100.2 (that is 1.002 times 100) shows only a minor twitch higher.

The table shows separately OECD indicators and their ratios to six-month ago for the U.S., U.K., EMU, Japan, and China. The U.S., U.K. and China each have readings slightly below 100 that point into to less than average growth conditions. In addition, the U.S. and U.K. readings slipped slightly in May while the Chinese reading has gained pace over four straight months. The EMU and Japan each have indicators above 100 and for each of them that indicator value is unchanged for three months running.

If we plot the six-month percentage change in the OECD indexes for these four countries plus the OECD area and the euro area, all of them are slowing down except China. Early this year, the six-month changes pointed to the strongest expansion for this grouping that we had seen since 2013. While the six-month changes are still positive, momentum is now fading instead of building.

Despite this fact, the U.S. has a monetary tightening program in effect at its central bank. U.S. rates are still low and below what would be construed as normal, but given the Fed's R-star view of the world, it is hard to say if this rate level is truly stimulative or not given the evolving economic circumstances. Since, as the Fed tells us, we do not observe R-star but only its consequences by watching the economy, that economy, through the lens of the OECD LEI, seems to be telling us the Fed funds level may have reached its limit for now. It is unclear if the Fed shares this judgement. In any event, we expect the Fed to soon announce it will begin to shrink its balance sheet and set in motion further contractive effects from monetary policy on top of a program of Fed funds rate hikes.

The OECD data essentially warn that EMU doing not much better than normal and is not significantly accelerating; there is some pick up over six months but not much. U.K. growth is underperforming and losing momentum. U.K. inflation is over the top, but economic momentum is fading plus the pending blow from Brexit will be slowing the U.K. and probably make monetary action against excess inflation unnecessary. Japan is just marking time. Activity is near dead normal with little change in momentum at a normal rate of growth that is essentially what this economy has been doing for a long time. This has not been enough growth to boost inflation hardly at all. The disappointment in Japan is not that Japan plans to do something that the data won't support but that Japan has been providing stimulus seemingly with no impact.

However, the percentile standings of the OECD LEIs show a firm reading only for the EMU with a 68th percentile standing of the OECD index. Japan has a near median 49.7 percentile standing. The OECD area as a whole has a 47.3 percentile standing. The U.S., U.K. and China each have much lower percentile standings. On balance, this really does not look much like the desired position from which we would expect a global unwinding of past policies of monetary stimulus to occur. But that appears to be what we are in store for. If the OECD LEIs are worth their salt, there is a strong suggestion here that any step up toward a monetary tightening or lessening of stimulus might not have far to run. Although the various central banks have their own favored metrics and each sees the world through its own lens, the lens offered by the OECD suggest that central banks are getting a case of nerves over their long period of super stimulus before their economics have really turned and before a tightening is warranted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief