Global| Jul 26 2018

Global| Jul 26 2018Confidence Mostly Is Slipping in Select European States

Summary

Consumer confidence across Europe remains a relative bright spot around midyear. The assessments here range from August for the forward-looking GfK survey for Germany to June for the United Kingdom. The U.K. is still toiling under the [...]

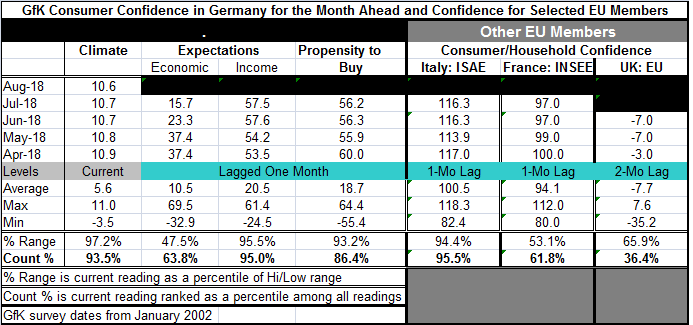

Consumer confidence across Europe remains a relative bright spot around midyear. The assessments here range from August for the forward-looking GfK survey for Germany to June for the United Kingdom. The U.K. is still toiling under the uncertainly of Brexit and that has taken a toll on confidence. The U.K. confidence measure is the lone weak reading in the table. At a reading of -7 in June, the U.K. confidence metric has a 37.6 percentile queue standing, marking it as below its historic median (medians by design locate at the 50th percentile level on this metric).

Consumer confidence across Europe remains a relative bright spot around midyear. The assessments here range from August for the forward-looking GfK survey for Germany to June for the United Kingdom. The U.K. is still toiling under the uncertainly of Brexit and that has taken a toll on confidence. The U.K. confidence measure is the lone weak reading in the table. At a reading of -7 in June, the U.K. confidence metric has a 37.6 percentile queue standing, marking it as below its historic median (medians by design locate at the 50th percentile level on this metric).

More broadly all metrics have slipped since at least April. And most have fallen –and some quite sharply- from January.

The GfK climate reading has fallen by 0.2 points, generating a 5.5 percentage point drop in its queue ranking since January. However, in Germany, the biggest hit came to economic expectations with that metric dropping by 3.7 points from its January level and seeing 31.2 percentage points shaved from its queue standing. However, income expectations in Germany continue to climb rising some 0.7 points since January and adding on percentage point to its queue standing. However, the propensity to buy has been adversely affected in Germany, dropping 4.2 points from its January level and shaving 10.6 percentage points off its queue standing.

Elsewhere, in Italy, consumer confidence is less than one point higher and the queue standing is higher by 1.2 percentage points. Italy has had a new government installed during this period and there has been a shift in the mood there that has dwarfed the change in global macroeconomic developments. But in France and the U.K., there is erosion in confidence. In France, confidence has fallen by 7 points since January, reducing the queue standing of confidence to 61.8% from 91.0% in January- a huge drop. The U.K. has seen a demonstrable drop on that period as well as the U.K. confidence reading shed 2.2 points, causing the confidence ranking in June to drop to a 36.4 percentile points as it transited lower from a 54.0 percentile standing in January of this year.

On these measures, a few things stand out. The first is that confidence has been substantially shaken since January with huge drops in the confidence standing in France and the U.K. and with economic expectations in Germany cut sharply along with a significant setback to the propensity to buy in Germany. The U.K. also saw a huge confidence drop on this horizon, but it has Brexit to blame for the most part.

Europe and the United States have been on the cusp of a trade war and that could account for a lot of the setback to confidence in Europe although there are other potential causes as well. Fortunately, the U.S. and the EU went to the brink on trade war then stepped back after a White House meeting just yesterday. The U.S. and Europe have decided to negotiate their differences (what a concept!) instead of going to a trade war. That is a very positive development. There is no deal but there is an agreement to deal and no deadline, so if both parties bargain in good faith, that should be the end of the trade conflict.

The U.S., of course, still has other trade conflicts with China and with NAFTA members in progress. As for Europe, it is still nursing a limping economy and at the same time the ECB seeks an end to its policy of very low rates and bond purchases. At the ECB meeting today, the ECB decided to kick the can down the road at least to the end of summer. Europe is looking at recently reduced growth prospects.

The U.S.-European agreement to step back from the brink is a good start to calm global tensions. But there are still many things to be tense about including U.S.-China on trade and China’s new obsession with how airports and airlines refer to Taiwan. You know, it’s always something.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief