Global| Dec 27 2018

Global| Dec 27 2018Confidence in Finland Begins to Show Some Unevenness

Summary

Consumer confidence in Finland has been steadily slipping. It remains relatively strong, but momentum has definitely soured. The levels for confidence across the various categories are quite mixed. Confidence values are ranked on [...]

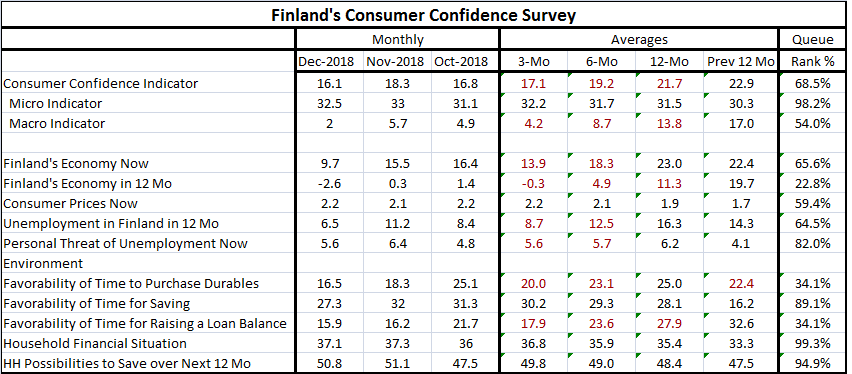

Consumer confidence in Finland has been steadily slipping. It remains relatively strong, but momentum has definitely soured. The levels for confidence across the various categories are quite mixed. Confidence values are ranked on observations back to January 1996. On that timeline,* the components in the table have standings ranging from their 99th percentile to their 22nd percentile (* The exception is the line-item ‘personal threat of unemployment now.’ That question only emerged in March 2004 so that response is ranked on a shorter timeline than the other components).

Consumer confidence in Finland has been steadily slipping. It remains relatively strong, but momentum has definitely soured. The levels for confidence across the various categories are quite mixed. Confidence values are ranked on observations back to January 1996. On that timeline,* the components in the table have standings ranging from their 99th percentile to their 22nd percentile (* The exception is the line-item ‘personal threat of unemployment now.’ That question only emerged in March 2004 so that response is ranked on a shorter timeline than the other components).

Still, the overall reading for confidence as well as for the macro indicators has slipped steadily. For both series, confidence is lower over the most recent 12 months than it was over the previous 12 months. Confidence is lower over six months than over 12 months and confidence is lower over three months than over six months. After all this slippage, the queue or rank standings have the overall indicator at its 68.5 rank percentile and the macro index just above its median at its 54th percentile.

In contrast, the micro reading has continued to improve and has a standing in its 98.2 percentile. So survey respondents are seeing their individual fortunes improve, but there has come to be a creeping degradation in the perception for economy as a whole.

Finland’s economy now has a ranking in its 65.6 percentile, reasonably firm but by no means a strong reading. But in contrast, the outlook for 12 months ahead has a rank standing in its 22.8 percentile. It has been weaker only somewhere between one-quarter and one fifth of the time. That is a strikingly negative result.

Inflation assessment has crept up over more recent readings, but it has only done just that, ‘crept.’ The current inflation assessment ranking is in its 59th percentile, only 9 percentile points above the median reading. Unemployment prospects have a 64th percentile standing, but people seem to feel a higher personal threat with an 82nd percentile standing. The personal threat statistic, however, is exaggerated. It is based on data back to March 2004 when this question was first introduced. And if we evaluate the overall unemployment metric on the same timeline as the personal one, the ranking is elevated to the 79.2 percentile level, putting the two readings on more or less the same footing. So the personal reading is actually not any (or not much) worse off that the overall macro view when the two are evaluated on the same basis.

The environment shows as extremely high standing for the household financial situation (99.3%) as well as for the possibilities for the household to save over the next 12 months (94.9%). The current evaluation for saving is at its 89.1 percentile, also a strong reading. However, it is not a propitious time to purchase durable goods as that rank standing is in its 34th percentile, near the lower one third of its historic band. Nor is it considered to be a favorable time to raise a loan balance with that standing also in its 34th percentile. In fact, both of these two environmental responses with the low rankings have been seeing deterioration fairly consistently over the past two years and in recent sub periods.

Not surprisingly, Finland as an EMU member feels some of the risk that we see exhibited in the overall EMU area’s sector assessments from Markit. The EMU is also feeling strains from exchange rate gyrations, an ongoing and as yet unsolved set of Brexit negotiations and from both existing and pending trade war tensions. The current and individual assessments remain in the solid to strong camp. But assessments of future prospects are less positive and more guarded. The simple outlook for the year ahead is depressingly weak. The personal threat to unemployment is still not as elevated as the slowing may seem to imply. But there is still some significant deterioration in train that should have an eye kept on it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief