Global| Mar 03 2005

Global| Mar 03 2005Chinese Inflation Falls Below 2% in January; Economy Becoming More Demand-Oriented?

Summary

China's inflation is slowing further. In January, the 12-month change in the CPI was 1.9%, the third consecutive weaker pace and the slowest since October 2003. As noted in the table below, a slowdown in food prices accounts for a [...]

China's inflation is slowing further. In January, the 12-month change in the CPI was 1.9%, the third consecutive weaker pace and the slowest since October 2003. As noted in the table below, a slowdown in food prices accounts for a significant portion of the moderation in overall inflation.

The last couple of months have also seen less rapid increases in fuel prices. These are actually included in the separate group of data, "retail prices", that is, the prices for merchandise sold in stores. The broader consumer price data, as those for other countries, also includes services, such as health care, recreation and so on. However, fuel prices are definitely related to trends in the broad CPI. A quick correlation analysis reveals that fuel price inflation with a one-month lead, has a 50% correlation with the movement of the CPI. Thus, while the Chinese government was concerned about rapid demand growth in China pressuring inflation, it seems more that food and fuel prices have greater force. At the same time, one can also argue that particularly in China, food and fuel prices might in fact be demand-driven as Chinese consumers are able to afford better diets and more fuel-using activities, such as heating and driving.

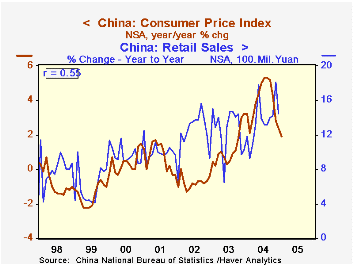

In the accompanying graph, we examine another facet of the Chinese consumer economy. Retail sales data, as in most countries, are quoted in nominal terms. For many years, then, retail sales and consumer prices moved in tandem, as the value of consumer purchases paralleled consumer prices. The correlation between the two for some periods was more than 90%. However, since 2002, this relationship has broken down. In 2002, retail sales sustained strong growth even as inflation was low. Last year, sales sagged in the summer and autumn in the face of higher consumer price inflation. This new pattern suggests a more demand-oriented response, in which slower prices encourage more buying and stronger prices send value-minded consumers away from the stores. Such a broad interpretation of a brief cycle of these monthly statistics is probably not warranted, but it's a phenomenon worth further scrutiny as the Chinese economy becomes more open and liberal in general.

| China: CPI 12-Mo % Changes |

Jan 2005 | Dec 2004 | Nov 2004 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Overall CPI | 1.9 | 2.4 | 2.8 | 3.2 | -0.4 | -0.3 |

| Food | 4.0 | 4.9 | 5.0 | 8.6 | 0.5 | -0.8 |

| Clothing | -1.6 | -1.7 | -1.8 | -1.8 | -2.9 | -1.7 |

| Housing | 5.5 | 5.6 | 6.3 | 3.5 | 0.2 | 0.7 |

| Fuel* | 16 | 17 | 22 | 6 | 12 | -5 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief