Global| Oct 31 2018

Global| Oct 31 2018China’s Manufacturing Stumbles More Than Expected

Summary

China’s manufacturing PMI fell for the second month in a row, clinging to a value barely in the zone that signals that output is expanding (PMI values above 50). China’s manufacturing PMI has not had a reading as strong as 52 since [...]

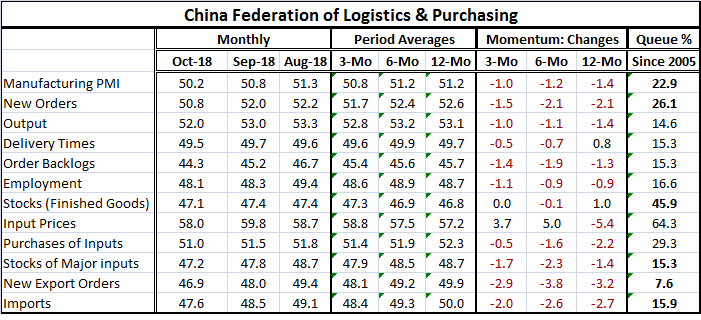

China’s manufacturing PMI fell for the second month in a row, clinging to a value barely in the zone that signals that output is expanding (PMI values above 50). China’s manufacturing PMI has not had a reading as strong as 52 since September 2017. It fell to 50.8 in September 2018 and now it has slipped again to 50.2 in October 2018.

China’s manufacturing PMI fell for the second month in a row, clinging to a value barely in the zone that signals that output is expanding (PMI values above 50). China’s manufacturing PMI has not had a reading as strong as 52 since September 2017. It fell to 50.8 in September 2018 and now it has slipped again to 50.2 in October 2018.

Momentum is eroding for manufacturing and across manufacturing components. Among the headline and its 11 components, all but three are showing momentum declined from 12-months to six-months and from six-months to three-months as well as from 12-months compared to 12-months ago. This is a broad representation of slowing across nearly all the manufacturing components and over significant and encompassing timelines.

In addition to momentum being exceptionally weak, the current strength across the sectors, as represented by the queue standings of the diffusion indexes, is extremely weak (The queue standings position this month’s reading in the entire pool of data expressing this month’s value as a percentile position in the ordered queue of monthly readings). The manufacturing PMI itself has a queue standing of 22.9. That means it has been this weak or weaker only 22.9% of the time. Seven components have queue standings in their ‘teens’ below their 17th percentile standing. The weakest of all is “new export orders” where the trade war is showing its teeth and the queue standing is at its 7.6 percentile.

The impact of the trade war is being felt in China. I have argued that this war will hit producing countries harder than consuming countries because these are tariffs being imposed on items with relatively high (in absolute value) price elasticities (price elasticities are generally negative; when prices rise we buy less of something). That economic jargon means that when prices shift, consumers tend to shift away from such items relatively easily. Think of food in the aggregate and oil as the polar opposite cases. While consumers may bemoan higher prices on TVs, computers, and cell phones as well as on clothing and household items, they have choice. They can buy other goods or shift to services. Or they can postpone purchases and wait for tariffs to be removed. Meanwhile, producers produce what they produce in the short run and have a hard time switching to make other goods (which may in this case still have tariffs applied to them as well). As a result, I expect any producer nation facing tariffs on its exports to feel the impact.

Apart for the economics, there is the policy question of how a damaged country responds. China can retaliate (as it has), but U.S. exports are not nearly as important to the U.S. economy as they are to China and other Asian economics. China is not just in the grip of the trade war but an example for others in the region. Trade needs to be a two-way street to be sustainable. Current global trade patterns are not sustainable. While some are fearful of where trade wars will lead, I am fearful of what might have happened had we not pursued this course of action to put trade on a firm footing where it might become sustainable for all parities again, instead of being co-opted for the domestic goal of a few selfish nations. Trade is intrinsically an international activity and must be fair to all parties. That means commercial policy (traffic and quota) needs to be fair and harmonized and exchange rates must be set by markets or in fashion to allow trade to follow the course it would if exchange rates were market-determined. Failing in any of these actions is failing to put trade on a fair and sustainable course.

Of course, the risk is that China may take its ire to the next level and strike out in a noneconomic way. It has, in fact, already done this by grabbing and entrenching its position in the South China Sea and becoming more vocal and aggressive about its claim on Taiwan. It has become more aggressive about challenging U.S. ships that purposely navigate the waters China has unilaterally expropriated to make it clear what we do not acquiesce to that claim – as we must if we do not to have that claim stand. While U.S. policy has tried to keep its economic and political relationship with China separate even by trying to get China to help the U.S. push North Korea to give up its nuclear arms, China has been willing only to agree to help on the surface while it has undercut the U.S. embargo on North Korea behind the scene. The U.S. relationship with China is very important and certainly it is in flux. It impinges on the rest of Asia where the U.S. has allies but where a ‘U.S. First’ policy has made them less certain how much the U.S. would back them against an increasingly ambitious China with an expansive belt and road program it has used to spread its influence. What is happening with China on the trade front will not be contained to trade - make no mistake about that. It is about much more than just trading relationships. And there are signs that the Trump administration is waking up to the adverse fall out from its America first program and that U.S. aid is starting to flow again. It is a situation in considerable flux and of immense importance to our future and to the future of Asia.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief