Global| Dec 15 2015

Global| Dec 15 2015Car Registrations No Longer Zoom Ahead in Europe; Volkswagen Is Another Problem

Summary

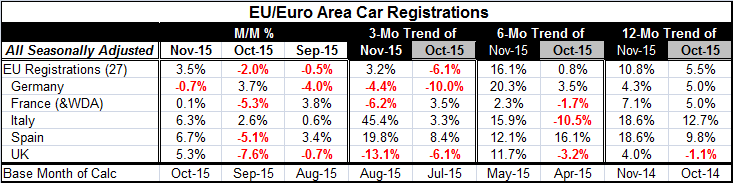

European car registrations are showing some strength in November as there are gains in four of five of the countries in the table plus a strong headline gain. Germany is lagging, where Volkswagen and its assorted name plates are [...]

European car registrations are showing some strength in November as there are gains in four of five of the countries in the table plus a strong headline gain. Germany is lagging, where Volkswagen and its assorted name plates are struggling in the wake of its environmental test tampering. But elsewhere sales are strong, at least for the month.

European car registrations are showing some strength in November as there are gains in four of five of the countries in the table plus a strong headline gain. Germany is lagging, where Volkswagen and its assorted name plates are struggling in the wake of its environmental test tampering. But elsewhere sales are strong, at least for the month.

Of course, auto sales/registrations are volatile measures. To underline that, we show in the table various horizons of gains but also show the relevant growth rates for November and October.

The growth progression of sales in November is from 10.8% over 12 months to 16.1% over six months to a sharply weaker 3.2% over three months. These annualized growth rates show a slowing in sales despite the strength in November. In October, sales rose by only 5.5% over 12 months compared to 0.8% over six months and -6.1% over three months. On both timelines, there is a tendency for registrations to slip, but by different magnitudes. While the stories about auto sales are still relatively upbeat, the trend is no longer a good one.

European registrations have been rising strongly for some time. This performance echoes what we have seen in the U.S. where auto sales have recovered more or less linearly once they got going in the recovery. Auto sales frequently are supported by nonbank lending and there has been strong usage of subprime loans in auto credit more so than in other forms of lending allowing auto sales to outstrip sales in many other sectors. In Europe, the auto sector has been a bright spot.

Despite the sales growth, however, European sales are still well below their prerecession levels. Since most journalists write stories from the perspective of the companies, we continue to read very upbeat stories about the auto sector. But economics is about sales growth. And in the U.S., for example, the same sort of thing is in train. U.S. vehicle sales have reached 18 million units, a level that the economy has never been able to sustain in the past. U.S. auto companies pared back capacity and are able to make profits at a lower pace of sales. As long as sales stay this strong, these companies will make profits and will be happy. Auto sector stories will remain upbeat. But that will not help economic growth much.

In Europe, we do not see any sales barrier in play, but we do see that for each of the last two months there is an indication of registrations getting tired and slowing. Early on, various nations had put auto sales incentives in place to spur sales. But these promotions have runoff and auto sales are losing some vigor. The European economy has been doing badly enough that the ECB did implement a new round of stimulus. But monetary stimulus has been notoriously impotent in this cycle and has resulted in interest rates scraping zero or in some cases dipping below zero to try to create some lift. Monetary stimulus has been most effective when it has been applied early in a slowdown. The ECB is bucking this trend and that may become a problem for auto sales.

Auto registrations in Europe have been a bright spot. It is part of a global trend. But even this robust sector appears to be showing some signs of slowing in Europe over the last several months. If the sector continues to slow, it will be even harder for monetary policy to make headway. The European market has the additional problem of housing Volkswagen whose sales are under pressure for corporate-specific reasons. But Volkswagen is such a large company that its problems could also add to the malaise in Europe. Europe's auto sector is in play. Will it be a force for growth, or an impediment to be overcome?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief