Global| Jun 16 2017

Global| Jun 16 2017Car Registrations Bounce Back in May; But What About Everything Else?

Summary

In Europe, both car registrations and retail sales are engaged in a long post-recession rebound. Both recoveries seem to be in train. Car registrations jumped by 13.4% in May reversing a sharp 8.7% drop in April. Sequential growth [...]

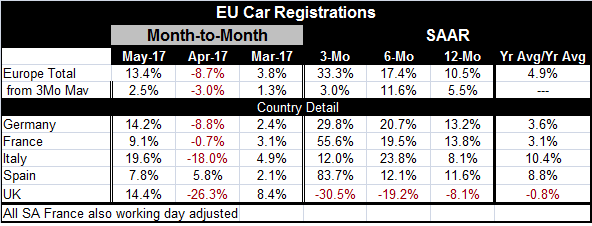

In Europe, both car registrations and retail sales are engaged in a long post-recession rebound. Both recoveries seem to be in train. Car registrations jumped by 13.4% in May reversing a sharp 8.7% drop in April. Sequential growth rates now have car registrations on an accelerating path, according to the headline for the report. Growth rates are up from 10.5% over 12 months to a 17.4% pace over six months to a 33.3% pace over three months. However, having just jumped out of a hole in May, we may want to withhold snap judgements on whether sales are really accelerating or not or whether this is just an artifact in the data. Except for Italy, all the EMU members in the table echo the acceleration conditions of the headline. In Italy, the three-month pace is still above the 12-month pace. The report is tempting to believe.

In Europe, both car registrations and retail sales are engaged in a long post-recession rebound. Both recoveries seem to be in train. Car registrations jumped by 13.4% in May reversing a sharp 8.7% drop in April. Sequential growth rates now have car registrations on an accelerating path, according to the headline for the report. Growth rates are up from 10.5% over 12 months to a 17.4% pace over six months to a 33.3% pace over three months. However, having just jumped out of a hole in May, we may want to withhold snap judgements on whether sales are really accelerating or not or whether this is just an artifact in the data. Except for Italy, all the EMU members in the table echo the acceleration conditions of the headline. In Italy, the three-month pace is still above the 12-month pace. The report is tempting to believe.

The UK: brewing more trouble than tea?

Contrarily, Brexit seems to have severely wounded the U.K. economy where car registrations were once a real bright spot. The U.K. now shows the opposite sequential deterioration in rates of growth for registrations. And not only is there deterioration, but it isn't just weaker growth rates, its contracting growth rates with the contraction becoming ever more severe. There may be more trouble than tea brewing in the U.K. economy.

Reality TV gives way to the view out the front window

Reality is springing a bad trap on Europe. On the verge of Brexit talks and all the chaos, that implies the IMF's Christine Lagarde reports today that the IMF would prefer a predictable exit for the U.K. but that it does not have enough information to make any judgement on the matter. But the Bank of England seems to see its way clear to taking a step to withdraw its emergency stimulus and even to consider seriously hiking rates. At yesterday's BOE meeting a deeply split decision kept policy on hold for now. Yet, U.K. retail sales also were reported to be quite weak in yesterday's report and now we have weakness in U.K. car registrations as well. It seems to me that weakness in the economy is making any restrictive action from monetary policy to fight inflation unnecessary, but the BOE seems to be slipping off that page.

Euro-growth hits more singles than homeruns

In the rest of Europe while consumer spending is still advancing and car registrations are rising. But inflation, the sole focus of the ECB, is still not hitting its mark. The German ZEW index weakened in the current month and ZEW readings on the rest of Europe show some prevarication.

Wrong-way Fed leads the way

Amid all of this gyrating and shifting and the awaiting of a sea change in monetary policy, should we be wearing our lifejackets? Are we really prepared for this sea-change? The U.S. is providing leadership for the move to rescind monetary stimulus, but once again like the knight said in the movie 'Indiana Jones and the Last Crusade,' the Fed seems have 'chosen poorly.' The Fed has this problem with adverse selection and it has been dogging the Fed ever since it decided that the time was ripe to begin to hike rates in 2015. That misguided decision was so premature that another 12 months passed before the Fed could execute its second rate hike and one of only 25bp. Now with the Fed having managed two more hikes after the December 2016 resumption of its tightening mode, economic data are coming up weak. Some weak data were released on the day of the Fed meeting (which it ignored). And, today, both housing starts the U of M consumer sentiment survey exhibit a more severe back tracking, taking the sentiment reading and its components back to their October/November levels to a period just before excitement over a Trump win began to stimulate and excite markets. So Europe is prepared to follow the Fed down this rabbit hole, but with its own inflation readings not fully in support.

Inflation lags as Germans nag

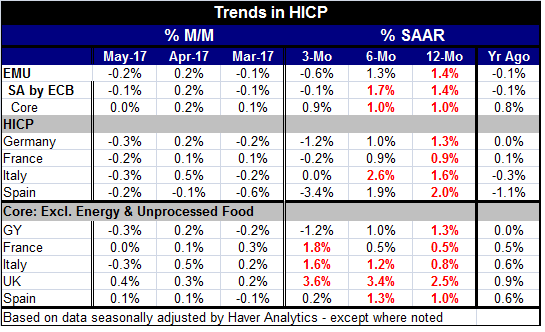

Europe's own inflation news finalized for May does not support a change in ECB policy, but various German policy officials are calling on the ECB to begin to move and the ECB has already eliminated some of its accommodative language paving the way for such a policy tilt. But the headline inflation rate in the EMU is up by just 1.4% and the core is running at a 1% pace. Headline inflation in the EMU is decelerating while core inflation has a soft side but is relatively stable at a 1% pace. France and Italy show some core inflation acceleration. Spain shows a mixed tend. And it is deliciously ironic to point out that in Germany core inflation is in a clear decelerating pattern with three-month (headline and core) inflation not just weaker but logging a negative rate; yes prices are falling on balance in Germany over three months as German officials clamor for the ECB to reverse its accommodation. The overall EMU-wide HIPC is also is falling over three months.

The policy upside-down cake

So who is responsible for publishing this recipe for policy? I thought that the inflation target and inflation performance for the ECB was supposed to inform policy there? I thought that the Fed's dual mandate was supposed to inform policy in the U.S.? Instead, we seem to have a situation where accommodation reversal has become the 'policy goal' regardless of the circumstance of the economy with its targets (such as inflation). The Fed has missed its inflation target for five years running; in its SEP 'forecasts' delivered just yesterday the Fed demonstrated that it will continue to miss its inflation target by even more. Yet, the Fed hiked its key rate in June and kept language in place about its intent to keep hiking plus it announced a plan to begin to shrink its balance sheet that seems relatively aggressive. The Fed in doing this is shifting its policy focus. It is making less accommodation and balance sheet shrinkage the policy goals rather that its stated objectives for its policy parameters like inflation. When did this happen? When did policy turn itself upside-down? When did the chicken become the egg? When did the hunter become the hunted? And how has this plan become so readily acceptable on both sides of the Atlantic?

Internet recipes for monetary policy?

I don't know what internet site Janet and Mario have visited, but I wonder if they were lured there by Russian hackers. Well, maybe not. We can't go blaming everything on the Russians... can we? Some times our bad judgement is simply our own. But clearly the economic circumstance in the U.S. has moved down a notch and yet Fed policy like the Titanic is racing to meet its own self-set rendezvous with time and one that seems to be less than cognizant of the prevailing risks.

Euro Data vs U.S. Data

To be sure economic data for Europe seem relatively more solid than the recent data releases for the U.S. that bear an uncanny resemblance to Swiss cheese. There are holes in the argument that the data are strong to the Fed's position that all is well enough and that it is time to add balance sheet contraction to a program of stepped up rate hikes. To be fair, Europe has not yet decided on this path, but it clearly has been making steps in that direction and the Germans appear to have worn Draghi down to some extent.

Surcharge for 'special sauce'

Meanwhile, we have yet to see what toll Brexit will take on the rest of Europe. The U.K.'s slippage is profound even in the presence of a diving exchange rate. Japan, for its part, is not getting any better or any worse. China has slowed down and debt, its main lever to manipulate the economy, seems to be a less reliable lever these days. But it apparently is the time of season for less accommodation. Even as various political storms rage in the U.S. and undercut the case to bank on stimulus before yearend, the Fed is setting its new course North by North-worst. And if the U.S. slows, there will be knock-on effects. And, if the U.S., U.K. and the EMU all begin to withdraw their special sauces of stimulus at the same time, that too will have consequences. So I'll ask again. Are we really ready for this sea-change in policy? Are you wearing your life preserver?

Clash of the Titans: markets vs. central banks

We could be sealing the fate of a stealth tsunami that will sweep away much of the progress that has been made in recovery. The bond market certainly is not acting like it is getting priced for the evolution of the Fed's rate hike balance sheet shrink offensive. The bond market is acting more as it does at the end of a rate-hike cycle. For some time, the markets and the Fed have been in conflict about what is right. Pardon me if I point out that the markets not the Fed have won all of these bets in this cycle. There has been an ongoing cacophony from economists about whether or not the Fed will able to get the Fed funds rate to its long run neutral positon. Many think that it cannot. The bond market trades like it thinks that the Fed cannot. And all that has profound implications for Europe and for ECB policy. Is Mr. Draghi paying attention? Could we get the Germans to stop making and drinking the rate-hike Kool Aide for a while? Once in a while it's important to pull your head out of the sand and actually look at what's going on. On the other hand, some just keep their noses buried in the cookbook and look for the next ingredient needed to make this upside-down cake expecting it to be so fine. At this point, that approach is looking to be less and less appropriate. The Fed at least needs to pull its head out of the cookbook and look out the window. Between inflation that won't rise and faltering economic reports there is plenty of reason to reset the menu.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief