Global| Oct 19 2018

Global| Oct 19 2018Canadian Retail Sales Weaken As Inflation Slows

Summary

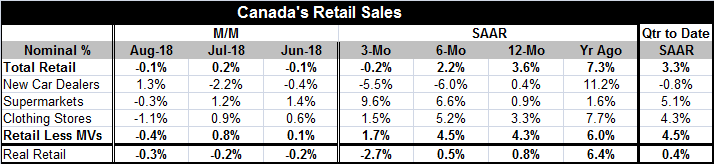

Canada's retail sales show relatively widespread deceleration. The headline shows growth one year ago at 7.3%, down to 3.6% over the most recent 12 months, dropping further to a pace of 2.2% over six months, and contracting over three [...]

What Is a Central Bank to Do?

Canada's retail sales show relatively widespread deceleration. The headline shows growth one year ago at 7.3%, down to 3.6% over the most recent 12 months, dropping further to a pace of 2.2% over six months, and contracting over three months at an annualized pace of -0.2%. That's not a good progression.

Canada's retail sales show relatively widespread deceleration. The headline shows growth one year ago at 7.3%, down to 3.6% over the most recent 12 months, dropping further to a pace of 2.2% over six months, and contracting over three months at an annualized pace of -0.2%. That's not a good progression.

Not all categories show such monotonic slowing. But all show slowing from the 12-month pace of one year ago to the pace over the last 12 months and all show weaker (generally much weaker) growth over three months than over 12 months. The lone exception to this is supermarket sales that are accelerating from 12-months to six-months to three-months. Real sales show a steady sequential step down in rates of growth and log a growth rate over three months of -2.7%.

In the quarter-to-date, nominal retail sales log a growth rate of 3.3% that seems adequate on its own. But in real terms, retail sales are up at just a 0.4% pace in Q3.

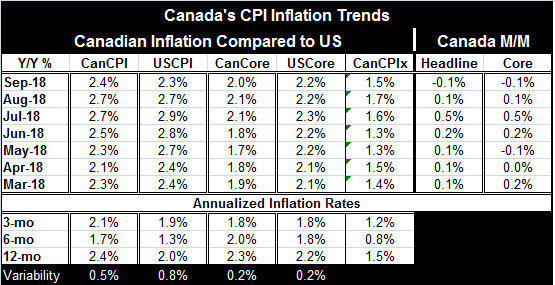

Against this background of slowing sales, we find Canada's inflation data somewhat less disturbing. Headline inflation is at 2.4% with a core expansion at 2% and the CPIx at a much more modest 1.5%. Both headline and core measures have fallen month-to-month in September, knocking down the stronger rates of growth each experienced in August. Canada's headline CPI pace slowed to 2.4% in September from 2.7% in August; the core slowed to 2% from 2.1%; and the CPIx decelerated to 1.5% from 1.7%.

Central bankers, policy limitations and inflation

A major problem for all central bankers globally has been how to treat inflation in this period when growth has been weak and oil prices have been gyrating. With every oil gyration higher, there is some inflation impulse transmitted to the headline rate and central banks tend to favor that rate as the policy rate. The Bank of Canada has an alternative approach as it monitors three different inflation gauges in a broad 1% to 3% target range. In the U.S., the Federal Reserve has a sort of back of the envelope emphasis on core inflation so long as it deems the headline as distorted but there is no formal announcement on that and officially the U.S. targets the headline of the PCE deflator. In the EMU, the headline HICP is the basis for ECB policy, period! But ECB head Mario Draghi has made it clear that with oil prices as an issue and with the core pace vastly undershooting the headline pace, he will continue to be advised by performance of the core rate.

The Bank of Canada emphasizes three inflation measures: the CPI trim (2.1% in September), the CPI median (2.0% in September) and the CPI common (1.9% in September). The Bank maintains a target range of 1% to 3% with the objective of keeping inflation in the middle of this range. As central bank inflation targeting goes, this range is a much more pragmatic approach than the stringent and somewhat-strange ‘a bit less than 2%' objective of the ECB and the point targeting of 2% by the Fed. The Fed's single point target approach has necessitated all sorts of additional arm-waving when inflation has deviated from the 2.0000% mark (the zeros are for sarcasm, rather than for precision) since inflation will almost always deviate from any point target.

Dealing with limitations

As odd as this may seem economics really has no good measure for two of the most important events in economics: recession and inflation. There is no quantitative definition of recession. Journalists use the rule-of-thumb (often, laughably, called a ‘technical definition of recession) of two consecutive quarters of negative GDP growth to chronicle a recession. But if you look at charts with recession bands in the U.S., these bands are decided by the NBER's Business Cycle Dating Committee. Formally, the declaration of recessions in the U.S. is made by a judgmental human decision. The NBER tells us that a recession occurs in a period when economic activity has be disrupted deeply enough, broadly enough and for a long enough period to call it a recession. So recession determination has a framework but not an actual measure. In Canada, it is much the same; the C.D. Howe Institute's Business Cycle Council establishes the parameters for recession and recovery cycles.

As for inflation, my comment may see strange or just outright wrong. After all, am I not writing about inflation statistics? Indeed I am. But what do they mean? And if we ‘know' inflation so well, why are there so many measures being juggled by the Bank of Canada and why are the basic inflation measures massaged to exclude certain things? And aren't these measures- all measures- of what inflation HAS BEEN rather than WHAT IT IS? Answer: they are. And that is a big part of the problem.

Most economists agree that the most important measure of inflation is what is expected, but we never observe that and never measure it! We can infer it from certain securities prices and we can survey groups to ask them what they think. The central bank can in models estimate future inflation but all of this is stabbing in the dark. And we know central banks individually and as a whole have not forecasted well. Yet, the Fed's own inflation expectations guide policy and in the U.S., the Fed's certainty that inflation is rising back to path and its concern that it might rise too much is dominating policy. In Europe, Draghi's insistence on emphasizing the core undershoot is keeping ECB policy easy. In Japan, no measure of inflation is restarting making the policy choice obvious except for those who fear that rates have been too low for too long. And there are a lot of those concerns everywhere.

The best policy approach is...

So what is the right thing to do? Economists, never lacking in confidence, would probably call for better modeling, better data and perhaps better more focused consumer/investor surveys. But in the end, we have flawed metrics, whatever we choose to do. If we choose to use surveys of expectations, we need to be alert to things that might change the opinions of those who we survey. If we use models, we need to pay attention to current conditions and ask if the model's forecasts remain on track every month. If we use various lagging inflation measures, we constantly need to reassess past trends and data that affect future trends. In short, whatever a policymaker chooses to do, he or she must remain flexible. Past trends may not be the future trends and our view of future trends held today may prove to have been wrong when the future comes. Are we really prepared to change our forecast in a timely way when its underpinnings shift? These are the main reasons that the policy of forward guidance is so peculiar. Forward guidance is only as good as each central bank's last policy mistake and for most that makes the value of forward guidance pretty low. Still, what is useful about forward guidance is having a more specific of idea of what the central bank thinks will happen so that when something different happens the investor knows to brace for a policy change. Forward guidance is not meant to be swallowed whole without any chewing.

BOC policy framework

In Canada, policy is more centered on its three main measures of backward-looking inflation: the CPI trim, CPI median, and CPI common. The median rate is the rate of the CPI component that has many components above it as below it. The trim rate takes out the most volatile elements (20% of the most volatile weighed elements), while the CPI common uses a model to identify common price changes across components and to eliminate movements that seem to be intrinsic to particular component. All of these approaches have pluses and minuses. The measures do not always tell the same story. But neither is the story that each tells usually very different.

With three inflation gauges and a broad band, the Bank of Canada has latitude to impose judgement and to communicate to markets what it thinks is going on with inflation given the various metrics it puts forth (in addition to the headline, the core and the CPIx). The primary gauges all show a rise in inflation in 2018, but most of them simply cluster around the fabled 2% pace (here). Coupled with weakness in retail sales and global slowing conditions, that suggests that the Bank of Canada should bide its time. However, like in the U.S., Europe and Japan, many are concerned that Canada has left rates too low for too long. So Canada's policy choice remains in limbo with a meeting coming up the end of the month. With it emphasize getting rates back toward ‘normal' as the Fed has done or will it give more weight to changing and weakening conditions at home and abroad? After all, the Bank of Canada, more than most, has wide latitude for judgement.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief