Global| Mar 22 2010

Global| Mar 22 2010Canadian Retail Sales Are On A Roll

Summary

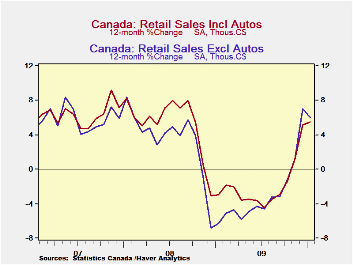

Canadian Retail sales rose a sharp 0.7% in January. Deflated by the CPI the retail sales rise comes back to a still respectable 0.4% gain. The year-over-year plot in the chart shows the acceleration in nominal retail sales is slowing. [...]

Canadian Retail sales rose a sharp 0.7% in January. Deflated by the CPI the retail sales rise comes back to a still respectable 0.4% gain. The year-over-year plot in the chart shows the acceleration in nominal retail sales is slowing. And that sort of thing is inevitable as growth rates climb. But it is also inevitable as recovery progresses and the recession gets pushed farther into history. In January the Yr/Yr gain is marked from January a year ago when sales rose by 1.7%. The December base for the year –over-year calculation is December 2009 when retail sales fell by 5% month-to-month. No wonder there is a noticeable backtracking there in the Yr/Yr rate of growth!

But the shorter sequential growth rate progression ( 3-M, 6-M 12-M) demonstrates that nominal sales growth has actually cooled over the past three-months compared to the 6-M and 12-M pace. On closer inspection that seems to have more to do with inflation as CPI-deflated retail sales accelerated to 3% over 6-months from 0.9% over 12 months and then to 3.9% over three months compared to six months. In the new quarter (2010-Q1) sales are rising at a 3.7% annual rate so the stronger growth rate seems to be mostly holding up.

The nominal sales data also show much more momentum in sales with motor vehicles excluded. The evidence there is of much stronger consumer spending in train. Retail less MV sales have accelerated from 5.5% over 12-months to 7.9% over 6-months to 10.1% over three months. In the current quarter the pace for sales is an even stronger 14%.

So there are various ways to assess the Canadian consumer. For the most part the consumer seems to be back to the store had shopping with gusto. Of course the Olympic Games came to Canada in February and so there could be a further boost to these figures at that time with the influx of tourists. For the moment, without the Olympic effect Canada’s consumers appear to be back on a spending path. Only auto purchases are lagging.

| Canada Retail Sales | ||||||||

|---|---|---|---|---|---|---|---|---|

| Mo/Mo | Saar | New QTR | ||||||

| Nominal % | Jan-10 | Dec-09 | Nov-09 | 3-Mo | 6-Mo | 12-MO | Yr-Ago | Saar |

| Total RTL | 0.7% | 0.5% | -0.4% | 3.5% | 6.0% | 6.0% | -6.3% | 5.7% |

| New Car Dealers | -2.3% | -0.4% | -2.3% | -18.2% | -0.6% | 10.6% | -19.5% | -18.3% |

| Supermarkets | 2.0% | -0.7% | 1.0% | 9.6% | 4.6% | 0.7% | 8.2% | 11.7% |

| Clothing Stores | 0.2% | 1.5% | -2.5% | -3.5% | 1.3% | -0.7% | -3.0% | 1.9% |

| Retail less MVs | 1.8% | 0.7% | 0.0% | 10.1% | 7.9% | 5.5% | -3.0% | 14.0% |

| CPI defalted Retail | 0.4% | 0.0% | 0.5% | 3.9% | 3.0% | 1.9% | 1.1% | 3.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief