Global| Jul 15 2020

Global| Jul 15 2020Canadian Orders Make Modest Rebound

Summary

After a sharp fall in April and a plunge in March, Canadian factory orders sprang back to life in May. The 9.4% gain is sharp by historic standards, but it comes in the wake of the declines orders have seen in previous months and the [...]

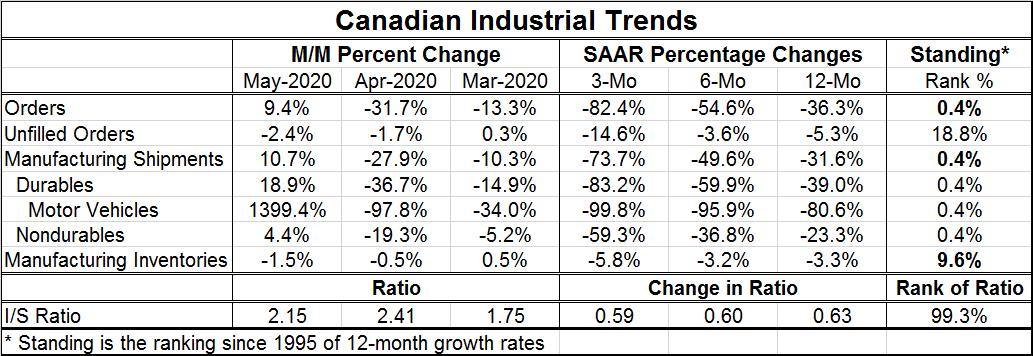

After a sharp fall in April and a plunge in March, Canadian factory orders sprang back to life in May. The 9.4% gain is sharp by historic standards, but it comes in the wake of the declines orders have seen in previous months and the rise is only a very modest step toward recovery compared to that reality.

After a sharp fall in April and a plunge in March, Canadian factory orders sprang back to life in May. The 9.4% gain is sharp by historic standards, but it comes in the wake of the declines orders have seen in previous months and the rise is only a very modest step toward recovery compared to that reality.

Shipments also are recovering in May, rising by 10.7% after a 27.9% April drop. Motor vehicle shipments have been hit especially hard but also have had the strongest relative gain in May.

Sequential growth rates from 12-months to six-months to three-months show progressively faster annualized rates of decline over shorter (more recent) periods. The exceptions to this are unfilled orders where the six-month rate of decline is less than the 12-month pace and for inventories that have the same characteristic. In both cases, the exceptions are minor and the three-month annualized drops are in place and are much larger that the six-month or 12-month rates of decline.

Ranking percentile standings tell a uniform story all factory metrics in the table; all are weak. In fact, all reside in the lower one-half of one percentage point of their respective queues of results except unfilled orders that has a lower 18.8 percentile standing and inventories that have a lower 9.6 percentile standing. Still, all of these readings are exceptionally weak.

Like most nations, Canada is still digging its way out of the wreckage caused by the spread of Covid-19 and by the efforts to stop it. Canada’s unemployment rate had been stable in a range of 5.4% to 5.7% or so before the virus struck. When the virus hit and actions to stop it were engaged, unemployment shot up to 13.7% and has only come down to 12.3% in June. Housing starts were impacted but have sprung fully back to life as of June. Export and import trends remain greatly impacted. Canada’s recovery looks like many others on the world scene. Actions continue to be taken to try to boost growth, but central banks and governments can only do so much especially if people are wary that it is dangerous to engage in economic activity. In Canada, like everyplace else, the outlook is speculative and prospects for better growth are going to continue to unfold day by day with the threat of reinfections and backtracking always looming.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief