Global| Aug 09 2017

Global| Aug 09 2017Canadian Housing Starts Claw Their Way Back to Pre-Recession Levels of 'Normalcy'

Summary

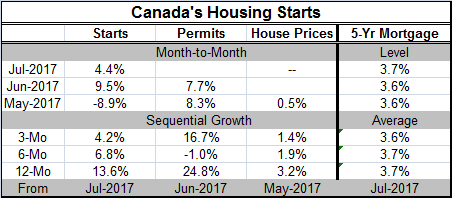

Housing starts in Canada rose by 4.4% month-to-month and are up for the second month running. The pace of starts is the third strongest in the last two years. Starts, in fact, have not been able to sustain or surpass this pace on a [...]

Housing starts in Canada rose by 4.4% month-to-month and are up for the second month running. The pace of starts is the third strongest in the last two years. Starts, in fact, have not been able to sustain or surpass this pace on a consistent level since before the Great Recession in 2008 and earlier. Permits data, which lag, are nonetheless robust, pointing to the continued expansion of housing.

Housing starts in Canada rose by 4.4% month-to-month and are up for the second month running. The pace of starts is the third strongest in the last two years. Starts, in fact, have not been able to sustain or surpass this pace on a consistent level since before the Great Recession in 2008 and earlier. Permits data, which lag, are nonetheless robust, pointing to the continued expansion of housing.

The house-price data lag by two months; house prices continue to rise on this basis but are not rising at a stronger pace. The pace of house price gains has slowed to a 1.4% annual rate over three months from a 1.9% pace over six months and a 3.2% pace over 12 months.

Canada, like the U.S., Europe and Japan, has muted inflation trends with its CPI and CPIx both running at a pace below 1% and with its core pace having downshifted to a 1.4% annual rate of expansion. Still, Canada, like the U.S., has embarked on a rate-tightening cycle.

Housing has been one of the most resilient sectors in the global economy. It is also the sector that helped to jump start the Great Recession because of the bad market practices firms had engaged in with housing financing vehicles. Regulations have closed the gap on those financial irregularities. Canada has not been party to the financial excesses visited in the U.S. due to its reliance on different financing practices and tighter regulation in Canada. Still, the global housing market tends to be connected.

One irrepressible international force is the search for high quality housing in safe places by the newly wealthy. That has been drawing the Canadian housing market into the international mix. The U.S. mostly on both the East and West coastal areas, London, Canada, and other places, have been affected by this diaspora of new buyers. Vancouver has taken steps to try and damp the impact of foreign buyers on house prices. Foreign influence is mostly stoking housing values in selected markets and has helped to drive prices out of reach and beyond the grasp of the average family in some areas. This is not yet a nationwide problem, but it is an issue in some of the more developed and desirable housing markets internationally. Canada has not been let out of it as Chinese investors have been especially interested in Canadian real estate. The housing markets of Montreal, Vancouver, Toronto, and Calgary in that order are most commonly named as places of interest.

The implementation of a 15% foreign-buyers tax last August in Vancouver had a sudden negative impact on the interest of Chinese investors searching for Canadian properties in that domicile.

As the world tries to exist with more open borders, these kinds of issues are going to continue to crop up. Donald Trump wants to move to fairer trade and wants to renegotiate the U.S. NAFTA treaty with Mexico and Canada. Trump also wants to build a wall to stop illegal immigrants on the U.S. southern border with Mexico. The U.K. has voted to leave the EU as a way to get out from underneath EU rules that cost the U.K. control of its own borders. Border issues have become more important. And it is important what people, how much money and for what kinds of investment border crossings occur. When international transactions become more fluid, the impact of domestic policy gets watered down or made ineffective. All sort of policies work differently in a very open economy than in one that is relatively closed. The real estate market has been a prime example of this and many newly wealthy investors seek to escape the place where they made their fortune to live somewhere nicer, where the laws are fairer, the educational system is good, and the environment less polluted. It is no surprise that Canada made this list.

Canada right now is in the midst of a housing revival that has brought starts back to their pre-Great Recession level of normalcy. Yet, it's a strong level by more recent standards. While house prices are rising, the pace of gain has decelerated. At the same time, the main national inflation rate gauges have slowed. While the level of starts is impressive and the pace of gains is solid, the slowdown in the pace of house price gains hints of a less robust market. That will remain something to watch. While the Bank of Canada has started to move its policy rate up, the five-year mortgage rate continues to hold to a steady path. Policy is not yet impeding any process in housing.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief