Global| Apr 21 2021

Global| Apr 21 2021Canada's CPI Shows Pressure, Just Part of the International 'Club' or a Misreading of the Tea Leaves?

Summary

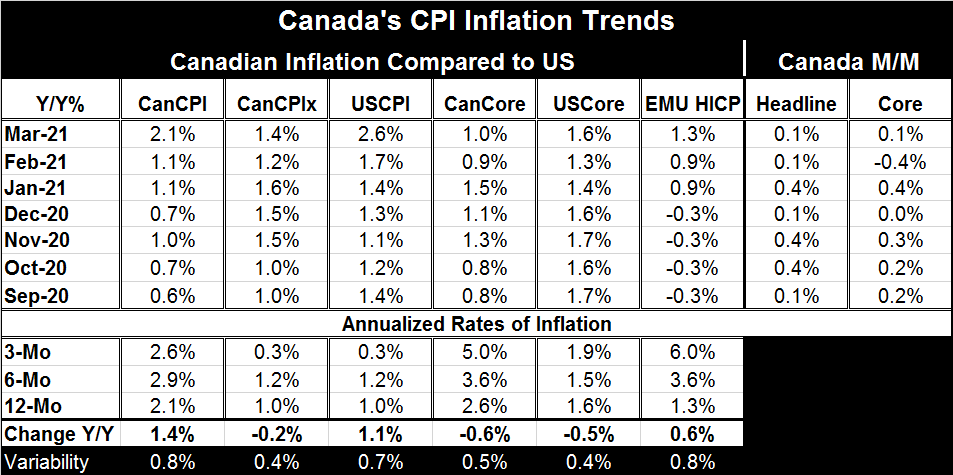

Canada's inflation is on the rise as are the inflation rates of the U.S. and EMU. The table shows that all 12-month inflation rates for the five of the six year-on-year categories are higher in March than in September. Five to one [...]

Canada's inflation is on the rise as are the inflation rates of the U.S. and EMU. The table shows that all 12-month inflation rates for the five of the six year-on-year categories are higher in March than in September. Five to one seems to be a pretty clear verdict. But sometimes even the simplest and seemingly clearest observations are not what they seem. Sometimes even Occam's Razor need to be sharpened.

Canada's inflation is on the rise as are the inflation rates of the U.S. and EMU. The table shows that all 12-month inflation rates for the five of the six year-on-year categories are higher in March than in September. Five to one seems to be a pretty clear verdict. But sometimes even the simplest and seemingly clearest observations are not what they seem. Sometimes even Occam's Razor need to be sharpened.

One problem here is that there has been a virus afoot globally. The virus has greatly impacted economic activity as we all know. And we also know that it has affected prices as we have all seen prices of some scarce consumer stable item rise strongly. On the other hand, other prices have become irrelevant. And despite being irrelevant, they are still in the market basket for prices. For example, with Broadway-type theaters closed and movie theaters closed, what is the relevance of theater and movie ticket prices? What about the price of a Caribbean cruise or a rock concert? And besides those sorts of examples, there is the question of the distortions in prices of those activities that have been allowed to barely operate such as restaurants that even now may or may not be open where you live and where businesses may or may not be open with restrictions in place. The question is when such distortions exist in an economy, what do prices mean? If no one is transacting at a price, is it even relevant? For this reason, these recent readings on inflation bear more scrutiny and less trust than usual.

The Bank of Canada has adopted a framework that explicitly focuses attention on processed views of inflation derived from the raw inflation statistic. It looks at the CPI-trim, the CPI-median and the CPI-common. You can find definitions of those gauges here and a discussion of what they are here. The names are descriptive as 'the trim' trims-off the excessive monthly moves, 'the median' looks at the middle of the distribution's price increase and 'the common' seeks to identify common trends and to jettison item specific price moves. The measures are intended to focus on the true trend for inflation and to reduce or eliminate pure variability or idiosyncratic moves in individual prices using differing methodologies. So Canada is trying to step away from drinking the Kool Aid of any individual monthly inflation headline. Of course, looking at the core inflation rate does the same thing in a crude way. The Bank of Canada's previous preferred gauge for accomplishing this objective, the CPI-X, eliminated eight of the most cantankerous CPI elements (plus indirect taxes).

Any way you slice it, prices are apt to have components each month that reflect a long delayed or anticipatory element that ought to be amortized over some period, annualizing the monthly change will simply blow a monthly anomaly up to 12 times its size. Spreading it over three months, six months or one year flattens it out but still might not flatten it enough (or flatten it too much). We do not know what the proper period is for discounting a rogue price increase when it emerges. Seasonal adjustment helps to remove price movements that occur at the same time each year such as annual price hike or hikes association with a new seasonal introduction of clothing or a new model of automobile. But many price wiggles are not so easily labeled.

This month BOC's CPI rises by 2.2% year-on-year (the calculations in the table uses Haver Analytics' seasonal adjustments). The trim CPI is up by 2.2% year-on-year. The median CPI is up by 2.1% year-on-year. The CPI-common is up by 1.5% year-on-year. Price increases are in the BOC's 1% to 3% range and near the range mid-point of 2% that the Bank seeks to hit.

Comparing inflation in the table to 12-month inflation of a year ago, we find the year-on-year change higher in just three-of-six categories and those are the categories with the greatest volatility. Considering just Canadian prices, the headline shows acceleration but the CPI-X and the core measure both show less inflation than a year ago and these are the measures designed to eliminate volatility.

Canada provides a framework by which to assess the simple incoming data against a number of measures that process raw inflation signals to remove excesses and pure variability. It is possible that when trends are shifting these measures will miss or diminish a true inflation shift until that shift is recognized as a new trend. All statistical filters can produce side effects. But for now Canada has a minor policy dilemma that, given the economic circumstances, certainly will keep monetary policy on hold. There is no clear and present danger from inflation just clear and present mixed signals involving some mild inflation that the processed indicators suggest may not be real. And with the economy still struggling and the virus still circulating economic help remains job-one in Canada as it does in most places globally. Inflation concerns remain a side show to economic reality. Still, they are a side-show that is moving markets and therefore not to be dismissed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief