Global| Oct 23 2015

Global| Oct 23 2015Can Europe Prosper on Services Alone?

Summary

Manufacturing in Europe has come up lame again in October. The sector has decelerated for the second month in a row and holds to a reading of 52.0, not much elevated from the neutral reading of 50.0. Still, Europe has been so weak [...]

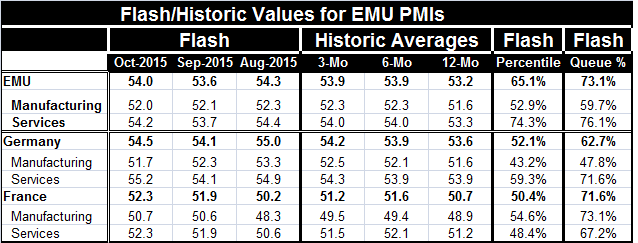

Manufacturing in Europe has come up lame again in October. The sector has decelerated for the second month in a row and holds to a reading of 52.0, not much elevated from the neutral reading of 50.0. Still, Europe has been so weak that at a reading of 52.0 in that index stands in the 59th percentile its historic queue of data. That is not a very strong standing, but it is higher than a reading of 52 should generate. In contrast, Germany's manufacturing PMI reading of 51.7 is a three-month low with a 47th percentile standing. For Germany, a reading of 51.7 in manufacturing is below its median (which occurs at the 50th percentile). France, on the other hand, has a persistently lethargic manufacturing sector and its reading 50.7 - just 0.7 points above the neutral reading of `50' - has a 73rd percentile standing. Manufacturing in France is better than this only 27% of the time. For France, lethargy is bliss.

Manufacturing in Europe has come up lame again in October. The sector has decelerated for the second month in a row and holds to a reading of 52.0, not much elevated from the neutral reading of 50.0. Still, Europe has been so weak that at a reading of 52.0 in that index stands in the 59th percentile its historic queue of data. That is not a very strong standing, but it is higher than a reading of 52 should generate. In contrast, Germany's manufacturing PMI reading of 51.7 is a three-month low with a 47th percentile standing. For Germany, a reading of 51.7 in manufacturing is below its median (which occurs at the 50th percentile). France, on the other hand, has a persistently lethargic manufacturing sector and its reading 50.7 - just 0.7 points above the neutral reading of `50' - has a 73rd percentile standing. Manufacturing in France is better than this only 27% of the time. For France, lethargy is bliss.

Manufacturing in the EMU is simply stuck at a low level. Yet, this is the high productivity sector of every modern economy. With underperformance in manufacturing, productivity gains will be limited as well as overall economic growth. But for now that is Europe's lot. Europe's growth is being driven by services. And how long can that last?

Fortunately, Europe is still highly competitive. The euro exchange rate is dropping. While global growth is too weak to allow Europe to exploit its competitive advantage and too weak to rev-up its manufacturing sector, it allows Europe to maintain a positive balance of trade which avoids any erosion of wealth.

Europe's services sector advanced in October to a 76th percentile standing in its historic queue of data. Germany's services sector advanced to 55.2 in October from 54.1 in September. The German series stands in its 71st percentile, a much higher relative standing than for German manufacturing. Cleary services are carrying Germany forward. In France, services rose for the second month in a row to a level of 52.3, leaving it only in its 67th percentile. While France's diffusion standing for services is higher than for manufacturing, the relative position of manufacturing is stronger. Neither reading is impressive.

For EMU overall services stand in their 76th percentile while the manufacturing sector stands only in its 59th percentile. And the raw score for services is a diffusion reading of 54.2 compared to 52.0 for manufacturing. Services are driving growth in the EMU.

An economy propelled by its services sector is simply not going to be as dynamic as one that relies more on manufacturing. Few services are tradeable thereby limiting the ability to tap foreign demand to expand the sector. Services productivity is low, hampering the ability of the sector to advance GDP very far. Services are not storable so the sector is always hand-to-mouth. When economic times get tough, a lot of what the services sector provides is a set of services that can be postponed or done by one's self instead of being purchased. The sector is vulnerable.

Although the EMU has advanced itself in October, it is not doing so in a way that contributes to the idea that strength in building. The reliance on services and the setback to manufacturing growth are troubling phenomena. For now growth in services is helping to preserve and advance growth in the euro area. But it is doing so in a way that is not reassuring about the future. And this is why the ECB is preparing to up its invention with more monetary stimulus. Europe is simply not kicking into high gear or even into a gear that is sustainable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.