Global| Aug 08 2018

Global| Aug 08 2018BOF Sentiment Index Has Small Setback in July

Summary

While the Bank of France saw enough in its monthly survey to announce that it was consistent with a small pick-up in GDP growth in Q3, the total industry index fell in July, dropping to 100.9 from June’s 101.4. That same survey [...]

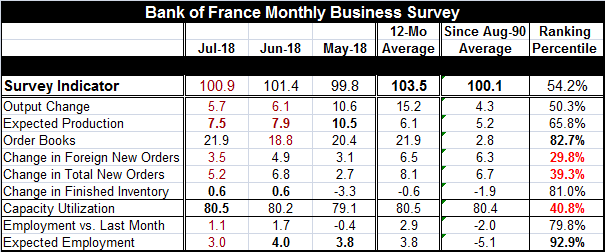

While the Bank of France saw enough in its monthly survey to announce that it was consistent with a small pick-up in GDP growth in Q3, the total industry index fell in July, dropping to 100.9 from June’s 101.4. That same survey barometer has a 54.2 percentile standing in its queue of data back to August 1990 and is below its 12-month average.

While the Bank of France saw enough in its monthly survey to announce that it was consistent with a small pick-up in GDP growth in Q3, the total industry index fell in July, dropping to 100.9 from June’s 101.4. That same survey barometer has a 54.2 percentile standing in its queue of data back to August 1990 and is below its 12-month average.

Among components, the queue ranking is the strongest for expected employment; it has a standing in its 92.9 percentile. Order books and change in finished inventories also have queue standings in their lower 80th percentiles. But neither rising inventories on hand nor expected employment drive business decisions in a positive direction. However, the relatively high standing for orders is good news.

The overall BOF industrial queue rank stands at a low barely above its median level for a reason. The strength in overall order books is reassuring, but changes in new and in foreign orders both show standings well below their respective 50th percentiles (which marks the median in all cases). Capacity use remains slack with a 40.8 percentile standing. Output change is above its median reading at a 50.3 percentile standing – but barely so. Expected production is better off with a 65.8 percentile standing. Current employment sports nearly an 80th percentile standing. For now the labor side of the equation remains strong.

Momentum

Five of nine of the index’s components are below their respective 12-month averages. Two others stand right on top of those averages in July. That leaves just two components that stand above their 12-month averages. They are: expected production and the change in finished inventories. However, the change in expected production has moved lower for two months in a row. A larger-than-recent change in finished goods inventories is not a good thing when the rest of the survey is slowing down. In that circumstance, the inventory building looks to be unintentional. That sort of build usually leads to production cutbacks and that is what is now in train as expected output readings – while still showing growth- have been nonetheless slipping.

Policy outlook

The Bank of France is upbeat on the outlook. But the percentile standings of the individual survey responses are not upbeat nor is the overall index itself. Also the survey seems to be losing momentum like so many other series these days. The Bank of France, like seemingly every other central bank, is not quick to take up the message that growth might be slowing. The business cycle is now somewhat long despite its expansion’s relative lethargy. And there are trade wars progressing and there is also the new issue of U.S. sanctions on Iran and the fall-out from that. If you were prone to worry, there is plenty to worry about. But central bankers seem only concerned about adjusting their rates upward and looking for the next opportunity to do that. I always warn that markets need to pay attention to the risk that central banks are not paying attention to because that one is the more dangerous one. Slowdown anyone?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief