Global| May 25 2017

Global| May 25 2017Belgium Struggles to Gain Critical Mass in Recovery

Summary

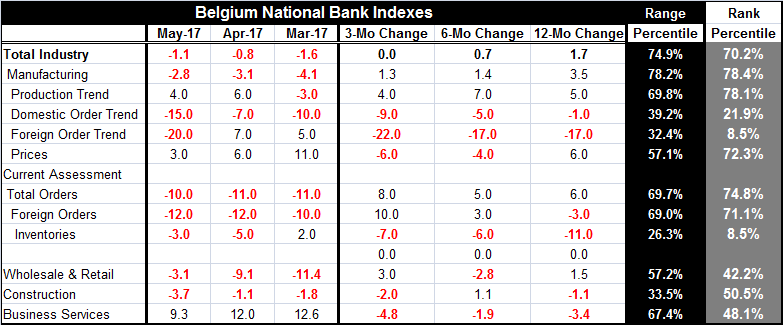

The Belgian National Bank indexes reveal a picture of an economy still trying to corral growth. The total industry, manufacturing, wholesale & retail, and construction sector indexes all log negative values in May. Only business [...]

The Belgian National Bank indexes reveal a picture of an economy still trying to corral growth. The total industry, manufacturing, wholesale & retail, and construction sector indexes all log negative values in May. Only business services post a positive value. However, if we rank the various sector indexes in their historic queues of data, we find that the services sector with its strong-looking positive value is historically weak and holds the second weakest sector ranking among all sectors in May. Manufacturing with a negative reading comparable in magnitude to those for wholesale/retail and construction nonetheless has a much higher sector ranking that is 'comfortably' at the 78th percentile of its historic queue of data. Meanwhile, the negative raw readings for wholesale/retail and construction are in their 42nd and 50th percentiles, respectively, below their historic means. The sector data essentially admit that the Belgian economy is not doing very well especially in its services sector and construction. The lethargy in manufacturing in some sense 'simply is what it is' and that is a 'business as usual performance' for that sector that has historically weak readings.

The Belgian National Bank indexes reveal a picture of an economy still trying to corral growth. The total industry, manufacturing, wholesale & retail, and construction sector indexes all log negative values in May. Only business services post a positive value. However, if we rank the various sector indexes in their historic queues of data, we find that the services sector with its strong-looking positive value is historically weak and holds the second weakest sector ranking among all sectors in May. Manufacturing with a negative reading comparable in magnitude to those for wholesale/retail and construction nonetheless has a much higher sector ranking that is 'comfortably' at the 78th percentile of its historic queue of data. Meanwhile, the negative raw readings for wholesale/retail and construction are in their 42nd and 50th percentiles, respectively, below their historic means. The sector data essentially admit that the Belgian economy is not doing very well especially in its services sector and construction. The lethargy in manufacturing in some sense 'simply is what it is' and that is a 'business as usual performance' for that sector that has historically weak readings.

For manufacturing, the production trend has a positive reading of 4 in May which translates to a queue percentile standing in its 78th percentile, the same queue standing as for manufacturing overall that reports a negative raw diffusion score in May. However the order standings for Belgium are much more worrying with negative readings of -15 for the domestic order trend and -20 for the foreign order trend. These two barometers post a 21st percentile queue standing for the domestic side and a much weaker 8th percentile standing for the foreign side. These are worrisome levels of standings. The price gauge for Belgian manufacturing prices has been on the decline, easing from 11 in March to 6 in April to 3 in May which nonetheless has a firm 72nd percentile standing. Just a few months ago, the Belgian price gauge was clearly overheating, now that has passed. While the overall manufacturing gauge has been making small increases over 12-month, six-month and three-month, and while the production trend supports those gains, domestic and foreign orders as well as prices show ongoing deterioration. Something will have to give here. These trends are inconsistent.

Apart from the trend results, the current assessment shows negative readings for total orders, foreign orders and inventories. The current assessment shows a sequential progression of improving orders even as trends fall and deteriorate faster. This is quite odd too. One indicator to keep an eye on is the trend reading for foreign orders which saw a complete collapse in May when it fell to -20 from 7 in April. If that outlier proves to be a fluke, the rest of the report looks a little less dour and could line up a little better internally that it does now. And while the order and pricing trends might still register some decay, the current assessments show the opposite improving path and that might work to provide support to the decaying trends in the months ahead. The report as it stands just has too sharp of a deterioration in trends that is inconsistent with an improving current assessment.

The other sector gauges show negative readings over each of the last three months for wholesaling/retailing and construction vs. three positive indications for services but with the monthly gains getting progressively smaller. The sequential trends across 12-month, six-month and three-month show a 12-month gain for wholesale/retail vs. declines in the construction and services. Business services show steady declines in momentum across the periods with the sector's strength becoming less pronounced. However, for construction and wholesale/retail, the broader patterns are less clear.

Geographically Belgium is nestled in the euro area sharing borders with France, Germany and the Netherlands. It sits amid some of the euro area's most competitive economies with straightforward across the channel access to the U.K. as well. There has been a ramp up in activity around Belgium in Germany, France, and in the EMU as a whole that does not seem to be benefiting Belgium at all, especially judging from the May collapse in the foreign order trend.

The BNB report raises as many questions as it answers. It reveals a lot of mixed trends with little in the Belgian economy that looks truly solid. And the weakness in the manufacturing sector seems 180-degreees apart from what the recent Markit indexes for the EMU, France and Germany have been doing. The EU Commission indexes, available through April, show much the same overall assessment of manufacturing as the BNB index and the same ongoing erosion in services. But some of the BNB components are still a bit puzzling especially in their weakness. I don't know about Denmark, but this report makes it look like there is something rotten in Belgium.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief