Global| May 14 2018

Global| May 14 2018Bank of France Business Survey Sags in April

Summary

The Bank of France business indicator continues to decline as it fell to 102 in April from 102.6 in March. The Bank of France used this survey to conclude that France's economy is set to expand at a steady pace of 0.3% in the second [...]

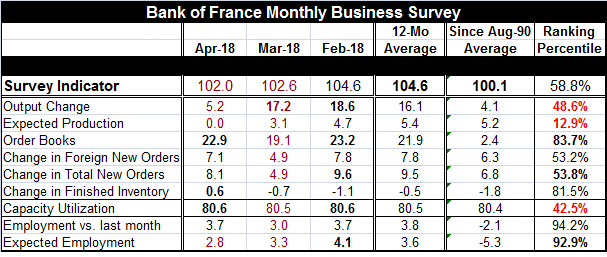

The Bank of France business indicator continues to decline as it fell to 102 in April from 102.6 in March. The Bank of France used this survey to conclude that France's economy is set to expand at a steady pace of 0.3% in the second quarter. However, the survey has been fading since reaching its peak in December. And while the BOF has held its estimate of growth in place, the path of the business indicator makes a reduction in the Bank of France’s next GDP estimate seem much more likely.

The Bank of France business indicator continues to decline as it fell to 102 in April from 102.6 in March. The Bank of France used this survey to conclude that France's economy is set to expand at a steady pace of 0.3% in the second quarter. However, the survey has been fading since reaching its peak in December. And while the BOF has held its estimate of growth in place, the path of the business indicator makes a reduction in the Bank of France’s next GDP estimate seem much more likely.

This cooling off also fits in with data from Europe that broadly has been in train for several months.

The French survey showed a sharp and widespread downturn in March followed by a less broad downturn in April but with weakness in key components. In April, for example, of the nine components in the survey, only three decline month-to-month. But what declines they were. The output change index fell to 5.2 from 17.1. This is the fourth worst month-to-month fall in this index in the last 26 years. And the Band of France’s response was to hold its estimate of Q2 GDP. Perhaps that was not most nimble forecast it might have made with these data in hand but it is one meant not to upset the apple cart. The gauge for expected production fell as well. Its drop is numerically less impressive falling to a small negative reading (that rounds to zero in the table) after posting a 3.1 reading in March. Expected production made its recent peak in June of last year and has undergone a herky-jerky decline ever since. The month-to-month fall in April is still large and has only been greater about 15% of the time. The final decline in the monthly components came from employment expectations that fell to 2.8 from 3.3. This is the weakest reading since June of last year, but it still represents a relatively high level reading for expected employment. Nonetheless, these three readings are the basis for the decline in the BOF business index month-to-month.

Yet, these data on changes are tempered by the standings of the some of the variables in terms of their levels. For example, employment last month has a response that is only higher about 6% of the time. Even with its drop, expected employment is a reading that is higher only about 7% of the time. Order books also have a relatively strong reading with an 83rd percentile standing (higher about 17% of the time). But output change with its outsized fall in April now has a 48th percentile standing, below its historic median. And expected production with a smaller fall has an extremely weak 12.9 percentile standing. It is stronger about 87% of the time.

This report has some very strong and very weak readings. Unfortunately, the (strong) labor market readings are not cutting edge and they tend to lag. More encouraging is that order books have a strong standing and recovered after a dip in March and are back above their 12-month average. But the change in orders and the change in foreign order series have standings that are both only in their 53rd percentile, a small margin above their respective historic medians (medians occur at a standing of 50). And somewhat disturbing also is the relatively high 81st percentile standing in finished inventories as that makes inventories seem high at a time that momentum is being lost.

The standing for the entire survey headline is only in its 58th percentile, a moderately positive reading. But this is a reading that is more moderate than positive especially with trend slippage in train. On balance, only order books, finished inventories and capacity utilization are above their respective 12-month averages in April.

The Bank of France survey clearly shows that the economy has been slowing down. For now the BOF chooses to hold its Q2 estimate for GDP in place. But all the trends for this survey point to a softening in train and a reduced outlook for French GDP seems to be the next likely step from the Bank of France.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief