Global| Jul 16 2015

Global| Jul 16 2015Auto Registrations and Retail Sales Show Broad European Recovery

Summary

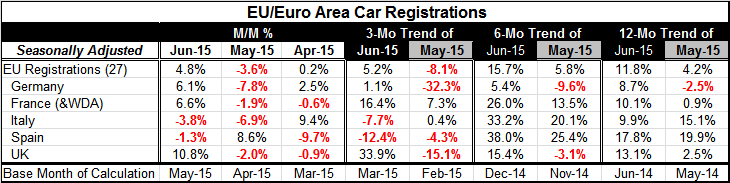

EU auto registration rose in June, advancing by 4.8% month-to-month and by 11.8% year-over-year. The country data range from a monthly gain of 6.6% in France to a 3.8% drop in Italy. Year- over-year registration gains range from 17.8% [...]

EU auto registration rose in June, advancing by 4.8% month-to-month and by 11.8% year-over-year. The country data range from a monthly gain of 6.6% in France to a 3.8% drop in Italy. Year- over-year registration gains range from 17.8% in Spain to 8.7% in Germany, pretty solid data.

EU auto registration rose in June, advancing by 4.8% month-to-month and by 11.8% year-over-year. The country data range from a monthly gain of 6.6% in France to a 3.8% drop in Italy. Year- over-year registration gains range from 17.8% in Spain to 8.7% in Germany, pretty solid data.

The monthly gyrations in registrations are substantial. The table below offers growth rates by horizon for June, the topical month, and for May, the lagging month. The annualized growth rates for these two months vary by 13.3 percentage points over three months, by 9.9 percentage points over six months, and by 7.6 percentage points over 12 months. What a difference a month makes! Is the June gain the right baseline, or would that be last month?

The overriding message here is that sales are advancing and are doing so at a rapid pace. The year-over-year gain of 11.8% is the highest such gain since January 2010.

Despite the relatively weak German gain year-over-year (8.7%), it is the strongest such gain in Germany since May 2014. Germany is the odd country here as it had even stronger registrations in 2011 when these other countries were experiencing year-over-year declines in registrations. Germany has been locked in a different cycle. German registrations have a 0.28 correlation with registrations in France (% year-over-year) and a 0.22 correlation with Italy. But with Spain and with the U.K., the German correlations are negative. Germany is on an opposite cycle with these countries (correlations are weak, however, and range from -0.15 to -0.11).

Despite the common currency (except the U.K.), the auto cycles are not in sync. Of course, one reason is that some of austerity countries put auto sales incentives in place to boost sales when economic conditions were grim.

Despite all that, the chart shows a nice correlation between auto registrations and overall retail sales volume in the EU. The rise in the two series is encouraging. At long last, the pace of sales and of registrations is getting back near the levels last posted in 2010. The metrics are still very far from their 2007-08 peaks. But just getting back to the 2010-2011 levels is an accomplishment.

Greece

With Greece finally approving its austerity package, much of the drama is now gone from Europe. But the bickering will remain as will other challenges. For now, the U.K. and other EU non-EMU members are upset that the authorities want to use an EU fund to support Greece putting non-EMU members at risk of loss. But because of time constraints there is little choice in this matter. The members are trying to hash-out a solution. Down the road, the U.K. will have a vote coming up to decide if it will stay in the EU.

Meanwhile just because Greece has a deal does not mean all will be well. Greece can now service its debts, but conditions there will continue to be grim. Much of the monies they have bargained to get will simply round trip back to the lenders to whom debts are owed. That should sure help expose the grand state of the charade this has been. The IMF is still leaning hard on Germany to give Greece debt reduction. The German position is that it is against the EU/EMU charter. Other austerity countries may have their own issues in coming months. But the tough treatment of Greece, of course, has been meant to deter any follow-the-leader uprising. Who would want to follow in Tsipras' footsteps?

Summing up

We have some signs of a true expansion in the EU/EMU. We see the end of formal hostilities (linked to negotiations) between Greece and the EU and Germany. But we still have many interesting days ahead. They will be much less `interesting' if Europe can stay on this recovery pace for retail sales and auto registrations, but that is a lot to ask. Unfortunately, Greece is only one of Europe's problems and addressing it does not eliminate all the risk to growth in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief