Global| Feb 01 2018

Global| Feb 01 2018Asia Flounders; China Fails to Mount Momentum

Summary

China's PMI as reported by the China Federation of Logistics and Purchasing shows a weaker result in February. (The Caixin Index for China's manufacturing is unchanged month-to-month at 51.5). China and the Philippines weakened in [...]

China's PMI as reported by the China Federation of Logistics and Purchasing shows a weaker result in February. (The Caixin Index for China's manufacturing is unchanged month-to-month at 51.5). China and the Philippines weakened in January relative to December. But Indonesia logged a PMI below 50, signaling contraction. South Korea and Thailand each have weak raw diffusion values shy of 51. Asia is not contracting but it is lethargic, posting low diffusion readings and failing to find a spark.

China's PMI as reported by the China Federation of Logistics and Purchasing shows a weaker result in February. (The Caixin Index for China's manufacturing is unchanged month-to-month at 51.5). China and the Philippines weakened in January relative to December. But Indonesia logged a PMI below 50, signaling contraction. South Korea and Thailand each have weak raw diffusion values shy of 51. Asia is not contracting but it is lethargic, posting low diffusion readings and failing to find a spark.

Only Japan and Vietnam have any semblance of truly strong readings. Japan has a queue standing in its 92nd percentile on a raw diffusion score of 54.8 and Vietnam has a queue standing in its 90th percentile on a diffusion value of 53.4. These two countries pair strong queue standings with substantial raw diffusion values. In contrast, Thailand is not authentically strong. It has a queue standing in its 88th percentile and that is elevated, but that reading is paired with a modest diffusion reading of 50.6. South Korea has a similar pairing. These two countries may be stirring after a long period of weakness but they are not strong, despite their queue standing metrics.

While everyone is focused on Europe and the U.S. and the nice recovery that is developing there, Asia is lagging. And Asia has been the marginal, or low cost supplier, in this cycle for the global economy. Asian countries continue to have lots of spare capacity and have none of the 'tight' labor market issues that the U.S. and Germany both are dealing with. It is probably a very strong reason to expect the reflation in the West to drill a dry hole; that is, to occur without stimulating inflation.

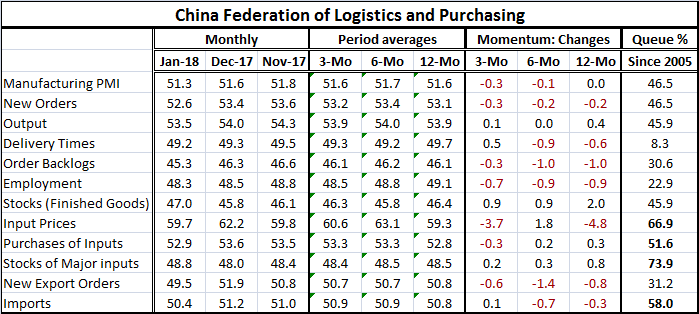

China's PMI chart (on top) shows a recent loss of momentum. Its own PMI survey (see Table below) shows a great deal of weakness. China's PMI headline has a 46th percentile standing over an extended period back to January 2005. Its January headline value of 51.3 is low and weaker than in December. China shows a loss in PMI headline momentum over three months and six months; on balance, it is only even with its value of 12-months ago. China has four PMI components that are net lower on all three horizons: they are new orders, order backlogs, employment and new export orders. These are important categories to be lacking so badly. China's best PMI component strength is unfortunately in inventories, which are probably overbuilt.

The queue standings of China's PMI components show only four above their median values since January 2005. These are for input prices, the purchase of inputs, imports, and stocks of major inputs. This is not an impressive collection of strength; in fact, it suggests the presence of imbalances.

Orders have a 46th percentile standing and new export orders have a very weak 31st percentile standing, although paired with a diffusion reading of 49.5. That pairing underscores just how much China has been depending on exports. A diffusion reading that is barely showing any export decline at all is a relatively rare bottom one-third result for China!

China still has not made much of shift to empower its services sector. The Belt and Road strategy that is so highly touted is not really a transformative policy for new China but rather is a policy aimed to develop trade routes and to keep old China chugging ahead. China has not made some of the more important changes to stimulate the part of the economy that the services sector depends on. Information flows are still highly regulated and controlled. Banks are overly protected and lending is still directed. Firms are not free to engage the foreign exchange market. In short China's Belt and Road strategy is simply meant to sound like something new that will in fact allow China to postpone making the changes it is promising. It is not a program intended to stimulate domestic demand and to wean itself off of export-led growth. It is quite the opposite. The Belt and Road program is meant to grease the skids for China's exports. It is in support of old China. New China is still little more than lip-service. And right now, old China is floundering.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief