Global| Feb 14 2018

Global| Feb 14 2018As Growth Ramps Up, Can Inflation Be Far Behind? Yes, It Can...

Summary

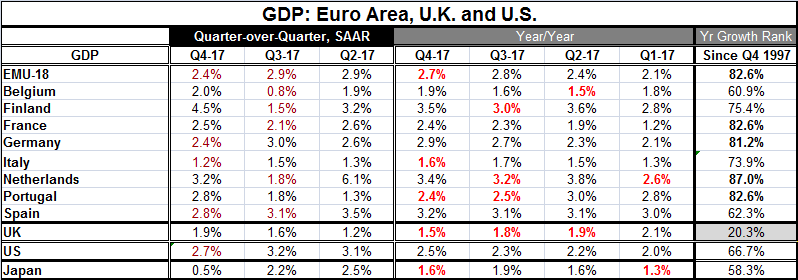

EMU GDP decelerated in Q4 2017 with growth tailing to a 2.4% compounded annual rate, compared to 2.9% in Q3 2017. The year-on-year pace of GDP growth is still quite solid as it decelerated by only a tick to 2.7% in Q4 from 2.8% in Q3 [...]

EMU GDP decelerated in Q4 2017 with growth tailing to a 2.4% compounded annual rate, compared to 2.9% in Q3 2017. The year-on-year pace of GDP growth is still quite solid as it decelerated by only a tick to 2.7% in Q4 from 2.8% in Q3 and strengthened from its Q2 pace of 2.4% and Q1 pace of 2.1%. Growth in the EMU is solid.

EMU GDP decelerated in Q4 2017 with growth tailing to a 2.4% compounded annual rate, compared to 2.9% in Q3 2017. The year-on-year pace of GDP growth is still quite solid as it decelerated by only a tick to 2.7% in Q4 from 2.8% in Q3 and strengthened from its Q2 pace of 2.4% and Q1 pace of 2.1%. Growth in the EMU is solid.

Big three EMU economies' quarterly growth

As for the Big Three EMU economies, in France growth accelerated Q/Q to a pace of 2.5% in Q4 from 2.1% in Q3; both Germany and Italy saw growth decelerations. Germany's growth slipped to a 2.4% pace in Q4 from 3% in Q3 while Italy slipped to a dismal 1.2% in Q4 from 1.5% in Q3. No wonder Silvio Berlusconi is having a come-back.

Solid trends for year-on-year growth in EMU

Focusing on the early reporting original EMU member economies, the table features eight of these earliest members and the aggregate for the EMU. In Q4 year-over-year growth is weaker in all of the EMU compared to Q3. We see this same development in Italy and Portugal. For most early-reporting original members in the table, growth is accelerating. In Q3 there are only three year-over-year decelerations and in Q2 and Q1 there are is only one deceleration in each of those periods. On balance, growth is EMU is on a firming track.

The best and worst of EMU member growth

However, there is only sequential accelerating growth across all quarters (based on y/y growth) for Germany, France and Spain. But that list contains three of the four largest EMU economics. Italy misses out with GDP slowing in Q4 relative to Q3; the same occurs for EMU growth overall. Portugal shows the most persistent weakening with growth slowing in Q3 as well as in Q4 but its Q4 pace at 2.4% is still relatively solid although it is tied for fourth slowest pace in Q4 (y/y).

Growth outside EMU

Away from the EU, the United Kingdom shows the most pernicious slowing with growth braking sequentially from Q1 to Q2 and in Q3 and again in Q4. U.K. year-on-year growth was only 2.1% in Q1 2017 and it now has slipped to year-over-year pace in Q4 of 1.5%, slower than the weakest growth rate in the EMU. The United States, on the other hand, shows growth speeding up sequentially, but only tipping the scales at a year-over-year pace of 2.5% in Q4.

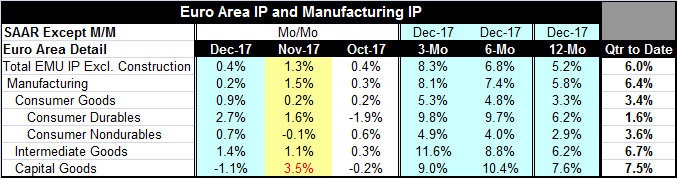

Industrial output in EMU gets hot

Euro area manufacturing output (IP) is now complete for 2017. Output has finally 'caught up to' the breadth readings in the manufacturing PMI. Manufacturing IP is up at an 8.1% annual rate in Q4 and by 5.8% year-on-year. In Q4 alone, it is expanding at a 6.4% annual rate. Year-on-year IP gains are led by capital goods and followed by intermediate goods; consumer goods are the weakest at a rise of 3.3%. All three sectors generally accelerate from three-month to six-month to 12-month. Although capital goods does slow a bit in three-month relative to six-month, its three-month pace remains much stronger than its pace over 12 months. As far as growth and momentum go, these are very solid numbers.

Got inflation?

Germany also has reported out inflation figures for January. Its consumer price index rose 1.6% year-on-year slower than its 1.7% increase in December. This is the final data from Destatis just released on Wednesday. The rate came in line with preliminary estimate and it shows that despite solid GDP growth and fast IP expansion, inflation is not being pressured in Germany and remains well away from the just-under-2% EMU-wide objective of the ECB.

Where's the slack, Jack?

However, Germany's output is back nearly to its past cycle peak. EMU shows a bit more slack while the U.K. is slightly tighter than the EMU overall. The U.S. shows slack of 4.5 percentage points while Japan is still nearly 10 percentage points below its past cycle peak. Lacking comparable data for China, I have benchmarked China to electricity usage as a proxy; China's electricity usage is still nearly 15% below its past cycle peak.

These statistics show that capacity is being taken up. They are not formal capacity use figures as they make no assessment about how much capacity might have changed since its last peak. Still, the numbers suggest encroaching tightness in Germany.

Is Keynesianism dead?

To me, the question remains whether local capacity matters much. In a global environment where goods and even some services can be supplied from outside sources, what is the meaning of capacity? Does it matter? And if it doesn't, does that mean Keynesianism is dead?

Less slack and still little inflation pressure

We have already seen unemployment rates fall to very low levels in the U.S, the U.K., and Germany without having a pronounced impact on wages. Now some German unions are negotiating richer settlements. In the U.K. the 'agents survey' (just released today) looks for wage increases of 3.1% on the year. The most recent U.S. jobs report revealed a headline wage proxy that rose by 2.9%, but when adjusted to focus on production workers (the better gauge of lasting wage pressures), that gain fell to just 2.4%. On balance, there is some stirring in wage pressures but not much more than that. So now we see evidence that capital has become more fully utilized as well. But will we continue to avoid 'bottle neck pressures' because essentially we can more easily choose to pour from a different bottle?

Will Globalization neuter Keynesianism?

If this globalism approach is correct, it does not imply that Keynesianism no longer applies or works but that it needs to be applied across a broader horizon. Of course, various kinds of local bottlenecks might still dominate. In the U.S., unions have slipped in importance and most of the unionized are now municipal workers. But the Teamsters still control trucking and the longshoreman. The ability to shut down transportation or the nation's ports will continue to confer to a union like that substantial market power. However, as a general statement, bottlenecks seem less relevant in the modern economy. And with improved communication, transportation and a much better-informed consumer, price discipline is still in its golden age. While there are concerns about inflation stirring and an ugly U.S. January CPI report has just been released, U.S. inflation headline and core are unaffected -unchanged- by this report. We have the same pace of year-on-year headline and core inflation in January as we had in December before this report was released. We continue to have more fear of inflation globally than we have evidence backing that fear. Central banks have still not decided how to react. We have relatively hawkish responses by the Fed in the U.S. and by the Bank of England. We have a more careful and watchful set of steps being taken by the ECB. Japan remains full tilt in the mode of pumping out stimulus. And markets are stuck in a new phase of uncertainty and seem to have lost much of their former nerve and bravado. It's a new game and we have to watch it carefully.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief