Global| Jun 11 2018

Global| Jun 11 2018A Souring of UK IP and The Outlook

Summary

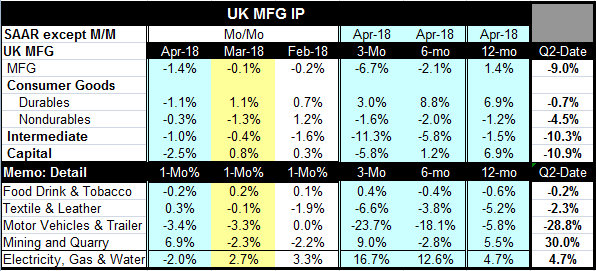

UK manufacturing sector IP growth fell sharply in April and declined for the third month in a row. Sequential rates of growth for manufacturing IP are getting progressively weaker and in the quarter-to-date (April’s growth positioned [...]

UK manufacturing sector IP growth fell sharply in April and declined for the third month in a row. Sequential rates of growth for manufacturing IP are getting progressively weaker and in the quarter-to-date (April’s growth positioned and annualized over the Q1 average). IP growth in the UK is contracting sharply. The decline in UK IP was unexpected but it fits in with a rash of IP weakness across Europe that also dove-tails with weakening European PMI gauges. And this is happening in a big week of central bank meetings where it is expected that central bankers will declare themselves to be on the yellow brick road to growth and adopt more policy normalcy…but should they?

UK manufacturing sector IP growth fell sharply in April and declined for the third month in a row. Sequential rates of growth for manufacturing IP are getting progressively weaker and in the quarter-to-date (April’s growth positioned and annualized over the Q1 average). IP growth in the UK is contracting sharply. The decline in UK IP was unexpected but it fits in with a rash of IP weakness across Europe that also dove-tails with weakening European PMI gauges. And this is happening in a big week of central bank meetings where it is expected that central bankers will declare themselves to be on the yellow brick road to growth and adopt more policy normalcy…but should they?

The European and global economies are dealing with any number of subtle shocks at the moment. I call them ‘subtle’ because while some of them are a subtle as a blow by a sledgehammer they are also effects that stem from fears of events that have not yet happened. It is always difficult to judge how far ahead of an act markets or economies are going to react. It is not clear what discount factor will be applied to events that have not yet happened and especially to events that speculatively may not even come to fruition. And we have such things hanging in the balance now.

Special events The most pressing concern for the UK is the transition under Brexit. This is a well-known phenomenon with a relatively firm transition period. But while the transition point is relatively well pinned down, the new terms and conditions of life under a Brexit regime are not determined. Markets reacting to Brexit are reacting to the unknown and in some cases firms are switching the domicile of their business to ensure that whatever Brexit brings they will be able to continue to perform. More subtle are the restive populist political movements in Europe especially in Italy where the Five Star Movement has become the dominant political party. After some saber rattling about leaving EMU, adopting the lira, or initiating a referendum on EU and EMU membership and wanting debt forgiveness the Five Star coalition with the Northern League has put the toothpaste back into the tube but there is no certainty about how long this coalition that has nurtured some harsh language in the past will continue to be passive. Finally there are the new US pressures over trade and the clear and present dangers of tariff threats and Europe’s own threats of reprisals against the US. This also includes ongoing US angst about funding so much of Europe’s defense when many nations of Europe do not pay their way in NATO as they had once agreed.

The CBI on Brexit On the issue of Brexit, the Confederation of British Industry (CBI), has weighed in today; it warns that the UK economy will shift to a slower gear this year and that risks have risen that growth will remain undernourished because of the Brexit transition. The CBI says it has cut its growth forecasts for the year, because of heavy snowfall in the opening months of 2018 and lingering fears over Brexit. The group now expects the growth rate for the British economy to slow to 1.4%, from 1.8% last year. GDP growth is expected to slip again, to 1.3% the next year, as the UK bids a fond (or not so fond) farewell to the EU.

Add in the ills from the ongoing and heightened trade spat with the US that became intensified by the G7 summit and there are ample reasons to expect that businesses might not be planning and investing for a better future despite solid global growth and broadly lowered rates of unemployment globally.

This is much bigger than Brexit and the UK My view of much of this is that we are still transitioning from the Post War period. World War II was devastating thing to the European area and to much of Asia. The US was never geographically a site of conflict. In the post war period a lot of effort was made to rebuild relationships and to repair physical properties ranging from factories to infrastructure to simple housing. There were also massive population relocations, post-war. The US cut the combatants- both allies and former enemies some slack is setting up post war trade relationships. Europe that has always been more socialistic than the US and was allowed to keep some market protections that the US did not demand for itself in trade, But now the Post War period is far behind us. While Europeans are used to this system and their special exceptions (like imposing tariffs on US goods when the US imposes no tariffs on theirs) the time for special treatment is past. Each and every G7 country with the possible exception of the UK runs consistent and stable trade surpluses in their bilateral trade with the US. Exchange rates do not change to remove or ameliorate this condition. The affluent US market is a source of demand for everyone to tap. But the US is not as rich or as competitive as it once was- especially not at current exchange rate levels.

Moreover, the once-accepted view of "unilateral Free trade" espoused by many US economists has proved itself an Achilles heel for US growth. With the US running a system of free trade for imports but others engaged in less than free trade on US exports and with exchange rates not being allowed to adjust to clear imbalances the US has become specialized in demand while Asia has become a supply center for the global economy. AND that is NOT what free trade means. It is not what ‘specialization’ means. Donald Trump’s desire to restore better-balanced two way trade flows is not being embraced overseas where changes will be needed. And as we see today with French farmers setting up blockades because imported palm oil will be allowed to be mixed in local gasoline stocks Europeans are activists protecting their ‘historic’ interests justified or not. A Bosnian blockade is also in play in Europe over high fuel prices. Europe does suffer economic activism over change. In France PM Macron has suffered through a persistent nationwide rail strike as he has tried to introduce modernization and as workers resist. Europe is hopelessly stuck in the socialistic Post War period and attempts to jolt it out of its niche find the European press referring to Trump’s plea for Free trade as ‘spew’ (here for an example from Reuters).

US President Donald Trump seems to make enemies much faster than he makes friends. He is arrogant, narcissistic and ham-handed in his political dealings. But none of that makes him wrong in this policy pursuit. While the US has ample reason to lash out at the way its trade is affected, Trump’s choice of National Security to protect metals trade pushes the envelope of logic. But maybe that is his plan as well, to use an outlandish WTO-allowed trick to drive his point home about how the US has been treated and cheated. Sometimes it is better simply not to try to understand Mr. Trump, but to treat him and his actions as simply existential.

Any way you slice it the US has been the protector of Europe for 60-years on. Angela Merkel dissed Mr. Trump as a ‘bad ally’ for his taunts suggesting that US obligations under NATO were in some way malleable when he first took office. He made it clear that he expected European and German obligations would be paid in to support of NATO as they had agreed. And after that spat and after calling the US a ‘bad ally’ Germany this year is CHOOSING to run a budget surplus instead of paying in its full share to its NATO commitment. So who is the real bad ally here? Who are the real unfair traders? Why does Trump’s rooting around in the legacy of Post War custom and practice makes him a bad guy? Oh his demeanor? Yes I get it. But what about the substance of the issues at hand? How does Europe justify any notion of ‘retaliation for all the support that the US given it and continues to give it? And is it any wonder that firms are pulling back in the UK and elsewhere in the wake of this kind of selfishness? If Trump is ‘spewing’ by pointing out Europe’s structural intransigence, what is Europe guilty of? And is Europe really going to try to hide from its lapsed responsibilities by playing tit-for-tat each time the US does something to try to even the very uneven playing field that is made clear every month when new trade figures report further European surpluses in trade with the US?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief