Global| Oct 29 2004

Global| Oct 29 20043Q US GDP Light at 3.7%

by:Tom Moeller

|in:Economy in Brief

Summary

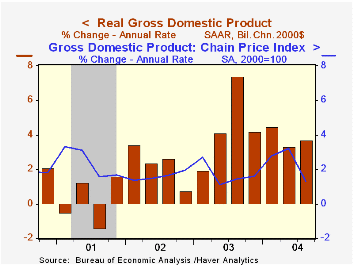

US real GDP grew 3.7% (AR) last quarter versus the Consensus expectation for growth of 4.5%. Nevertheless, 3Q growth was a slight acceleration from 3.3% in 2Q. The shortfall in GDP growth relative to expectations reflected meager [...]

US real GDP grew 3.7% (AR) last quarter versus the Consensus expectation for growth of 4.5%. Nevertheless, 3Q growth was a slight acceleration from 3.3% in 2Q.

The shortfall in GDP growth relative to expectations reflected meager contributions from residential investment (0.2 percentage points versus 0.9 points in 2Q) and from government spending (0.3 percentage points versus 0.4 points in 2Q).

Weakness in these categories limited growth in domestic final demand to 4.6% versus 3.5% in 2Q. Personal consumption growth sped up to 4.4% versus 1.6% in 2Q with spending on motor vehicles up 27.2% after a slight 2Q decline. Spending on apparel also recovered after a 2Q decline and furniture spending continued to boom at a 10.3% rate (9.7% y/y).

Business investment growth also continued strong at an 11.7% rate (9.8% y/y) with spending on equipment & software up 14.9% (12.2% y/y). Spending on information processing equipment & software rose only 4.4% (12.7% y/y), however, spending on industrial equipment rose 30.1% and transportation rose 27.0%.

Slower accumulation of inventories subtracted 0.5 percentage points from GDP growth, the first negative contribution since 2Q03 though it was dominated by a huge drawdown of motor vehicle inventories. (Real motor vehicle output rose 10.0% (1.1% y/y) last quarter, the net of the boom in vehicle sales and the drawdown of inventories.)

Foreign trade again subtracted from GDP growth as a 5.1% (9.2% y/y) rise in exports was outpaced by a 7.7% (11.9% y/y) gain in imports.

Expanded detail indicated that GDP less motor vehicles rose 3.5% (4.0% y/y) and that GDP less computers rose 3.7% (3.9% y/y).

Price inflation was quite tame at 1.3%, about as expected. Lower prices for consumer durables and for business investment in equipment & software as well as a light 1.6% increase in prices paid by the federal government held back the increase.

| Chained 2000$, % AR | 3Q '04 (Advance) | 2Q '04 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| GDP | 3.7% | 3.3% | 3.9% | 3.0% | 1.9% | 0.8% |

| Inventory Effect | -0.5% | 0.8% | 0.5% | -0.1% | 0.5% | -0.8% |

| Final Sales | 4.2% | 2.5% | 3.4% | 3.1% | 1.4% | 1.6% |

| Trade Effect | -0.6% | -1.1% | -0.7% | -0.3% | -0.7% | -0.2% |

| Domestic Final Demand | 4.6% | 3.5% | 4.1% | 3.4% | 2.1% | 1.8% |

| Chained GDP Price Index | 1.3% | 3.2% | 2.2% | 1.8% | 1.7% | 2.4% |

by Tom Moeller October 29, 2004

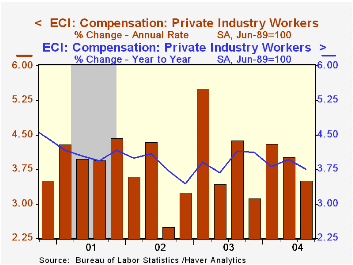

The employment cost index for private industry workers rose 0.9% last quarter, in line with Consensus expectations for a 1.0% gain.

Wages and salaries, which account for roughly 70% of the compensation index, accelerated from 2Q and rose 0.9%.

Benefit cost inflation in 3Q decelerated to 1.0% as the y/y cost of health benefits eased to 7.3%, the slowest since late 1999.

| ECI- Private Industry Workers | 3Q'04 | 2Q'04 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Compensation | 0.9% | 1.0% | 3.7% | 4.0% | 3.2% | 4.2% |

| Wages & Salaries | 0.9% | 0.6% | 2.6% | 3.0% | 2.7% | 3.8% |

| Benefit Costs | 1.0% | 1.7% | 6.8% | 6.4% | 4.7% | 5.1% |

by Tom Moeller October 29, 2004

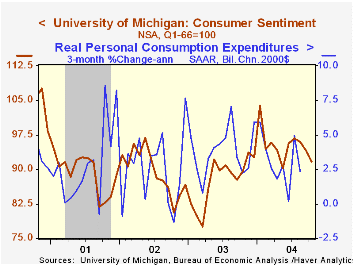

The reading of consumer sentiment for the full month of October from the University of Michigan did fall 2.7% m/m to 91.7, but that reflected a sharp improvement from the mid-month read of a 7.1% plunge to 87.5. Consensus expectations for a reading of 88.0.

The continuing decline in claims for unemployment insurance may have bolstered confidence following earlier concerns over the War in Iraq, the rising price of gasoline and several hurricanes which hit Florida.

During the last ten years there has been a 75% correlation between the level of consumer sentiment and the y/y change in real PCE.

The reading of current economic conditions improved 0.3% m/m versus the mid-month read of a 4.0% slump. Consumer expectations shaved the mid-month decline in half and fell 4.8% m/m.

The University of Michigan survey is not seasonally adjusted.The mid-month survey is based on telephone interviews with 250 households nationwide on personal finances and business and buying conditions. The survey is expanded to a total of 500 interviews at month end.

| University of Michigan | Oct | Sept | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Consumer Sentiment | 91.7 | 94.2 | 2.3% | 87.6 | 89.6 | 89.2 |

| Current Conditions | 104.0 | 103.7 | 4.1% | 97.2 | 97.5 | 100.1 |

| Consumer Expectations | 83.8 | 88.0 | 1.0% | 81.4 | 84.6 | 82.3 |

by Tom Moeller October 29, 2004

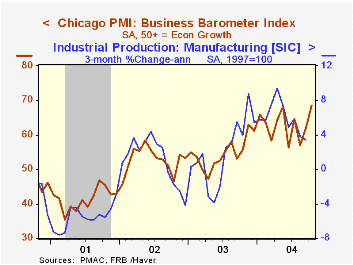

The October Chicago Purchasing Managers Business Barometer jumped 6.6 points from September to 68.5, just nosed out the prior high and was at the highest level since July 1988. Consensus expectations had been for a slight decline to 59.0.

During the last ten years there has been a 73% correlation between the level of the Chicago Business Barometer and the three month change in factory sector industrial output. That correlation has risen to 86% during the last five years.

The new orders index jumped to 79.4, the highest since 1983. The employment index rose slightly to 54.1, a five month high. During the last twenty years there has been an 80% correlation between the level of this employment index and the three month change in factory sector employment.

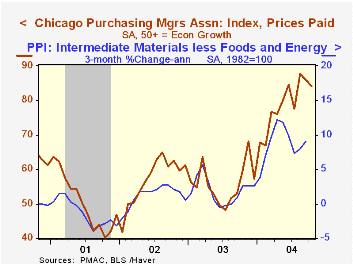

The index of prices paid remained firm at 84.1. During the last ten years there has been an 88% correlation between the Chicago price index and the three month change in the "core" intermediate goods PPI.

| Chicago Purchasing Managers Index, SA | Oct | Sept | Oct '03 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Business Barometer | 68.5 | 61.9 | 55.8 | 54.7 | 52.7 | 41.4 |

| New Orders | 79.4 | 69.7 | 61.6 | 58.0 | 56.2 | 42.3 |

| Prices Paid | 84.1 | 85.9 | 59.8 | 55.8 | 56.9 | 50.4 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief