Global| Apr 26 2002

Global| Apr 26 20021Q GDP Stronger Than Expected

by:Tom Moeller

|in:Economy in Brief

Summary

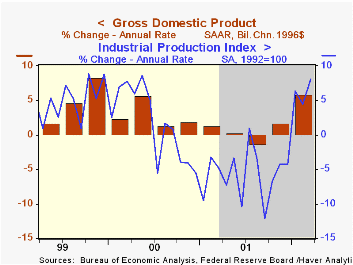

GDP surged more than expected last quarter owing to a reduced rate of inventory liquidation and surprising resiliency in domestic final demand. The rate of inventory liquidation eased to $36.2B from $119.3B, adding 3.1 percentage [...]

GDP surged more than expected last quarter owing to a reduced rate of inventory liquidation and surprising resiliency in domestic final demand.

The rate of inventory liquidation eased to $36.2B from $119.3B, adding 3.1 percentage points to GDP growth. Production must be raised in order to slow the rate of inventory decline if demand remains high.

Nevertheless, trade sector deterioration sapped considerably from GDP growth as exports, up 6.8% (AR), lagged imports which rose 15.5%. Service imports surged.

Domestic final demand growth was more resilient than expected, rising at about the same rate as in 4Q. Real PCE rose 3.5% (AR) versus 6.1% in 4Q. Residential investment surged 15.7% after a 4Q decline and fixed capital investment declined 0.5%, the most moderate rate of decline in six quarters.

Inflation was tame rising at half the rate expected by Consensus. The PCE deflator rose 0.6% while fixed investment prices fell.

| Chained '96 $, % AR | 1Q '02 (Advance) | 4Q '01 | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| GDP | 5.8% | 1.7% | 1.6% | 1.2% | 4.1% | 4.1% |

| Inventory Effect | 3.1% | -2.2% | 0.0% | -1.1% | -0.2% | -0.2% |

| Final Sales | 2.6% | 3.8% | 1.6% | 2.3% | 4.3% | 4.3% |

| Trade Effect | -1.2% | -0.1% | -0.4% | -0.1% | -0.6% | -0.9% |

| Domestic Final Demand | 3.7% | 3.9% | 2.0% | 2.3% | 4.9% | 5.2% |

| Chained GDP Price Deflator | 0.8% | -0.1% | 1.3% | 2.2% | 2.3% | 1.4% |

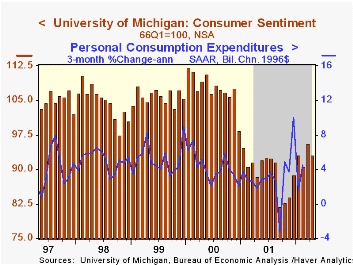

by Tom Moeller April 26, 2002

The April reading of Consumer Sentiment from the University of Michigan fell unexpectedly versus March.

Deterioration in sentiment apparently continued throughout the month.

The University of Michigan survey is not seasonally adjusted.

During the past five years there has been a 37% correlation between the level of consumer sentiment and the 3-month % change in real PCE.

| Univ. of Michigan | April | Mar | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Consumer Sentiment | 93.0 | 95.7 | 5.2% | 89.2 | 107.6 | 105.8 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief