Global| Sep 22 2025

Global| Sep 22 2025AI, Baumol, and the Healthcare Hump

by:Andrew Cates

|in:Viewpoints

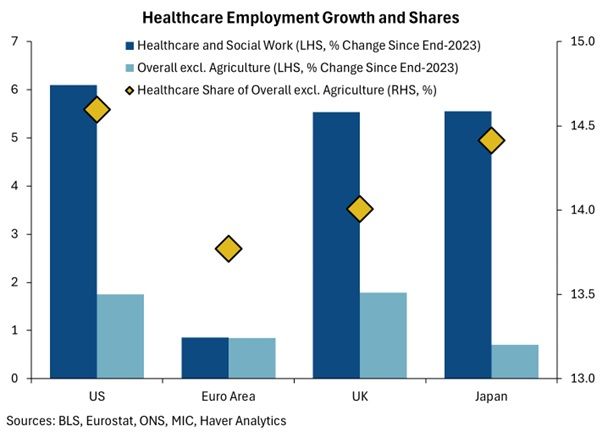

The AI boom has revived the old promise that a wave of general-purpose technology will lift labour productivity everywhere. But sector mix matters. The chart below shows where recent job growth has actually happened: healthcare and social care. Since end-2023, employment in that sector has grown 3–4x faster than overall payrolls in the US, UK and Japan, pushing healthcare’s share of total jobs toward 14–15%. The euro area has been softer, but the direction is similar. Ageing populations and long-COVID backlogs are doing the heavy lifting. But the composition effect is awkward for macro optimists: healthcare is labour-intensive, highly regulated and only partly tradable—characteristics that usually come with lower measured productivity growth.

Economists have a name for this tension: Baumol’s cost disease. When high-productivity sectors raise wages, low-productivity sectors must follow to retain staff, even if their output per worker doesn’t rise much. As labour shifts toward these “stagnant” sectors, aggregate productivity growth can slow.

That sectoral shift isn’t hypothetical; it shows up in official outlooks. The US Bureau of Labor Statistics projects that healthcare and social assistance will drive the bulk of US employment growth over the next decade. Across the OECD, roughly one in ten jobs is now in health or social care, and health spending has risen as a share of GDP compared with the pre-pandemic period.

So where does AI fit? At the micro level we already see productivity wins—administrative automation, documentation, triage, imaging decision-support—yet the macro evidence remains thin. Economy-wide gains require adoption, complementary capital and organisational redesign; without those, effects stay local. Put differently: if most incremental hiring lands in healthcare, even sizeable AI improvements inside clinics may offset rather than lift the headline productivity trend.

Measurement complicates the story further. Public-service productivity is hard to pin down because health output isn’t priced; recent UK data show healthcare productivity still below pre-pandemic levels despite bigger budgets. That underlines how capacity constraints (staffing, beds, diagnostics) and workflow frictions can swamp technology inputs. If AI is to register in the macro stats, it has to clear these bottlenecks, not just add tools at the margin.

There’s also the infrastructure bill. Training and running frontier AI models is energy-hungry; international energy agencies expect global data-centre electricity use to roughly double by 2030, with AI workloads a key driver. US forecasters now see record national power demand through the mid-2020s, citing data centres as a major contributor, and private surveys show record data-centre construction. Those are real costs that must be financed and fed by grids already straining under electrification and connection queues.

Investment test. For AI to be unambiguously profitable at scale, aggregate income formation must keep pace: either because AI lifts productivity in large, tradable sectors enough to overcome Baumol-type dilution, or because it raises quality-adjusted output in healthcare (shorter waits, fewer errors, better outcomes) in ways our statistics will actually capture.

Bottom line: AI can still be a major productivity force, but the macro path runs through the sector mix. If labour keeps migrating toward healthcare while measured productivity there remains weak, aggregate gains will be muted—even as costs for compute and power climb. So it’s worth watch three gauges to judge whether the optimistic case is materialising: healthcare’s employment share; healthcare productivity in official stats (are backlogs and outcomes improving for the same inputs?); and AI infrastructure intensity—data-centre spend and electricity use—relative to realised efficiency gains. Until those lines move together, the “AI will rescue trend productivity” story could struggle.

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.