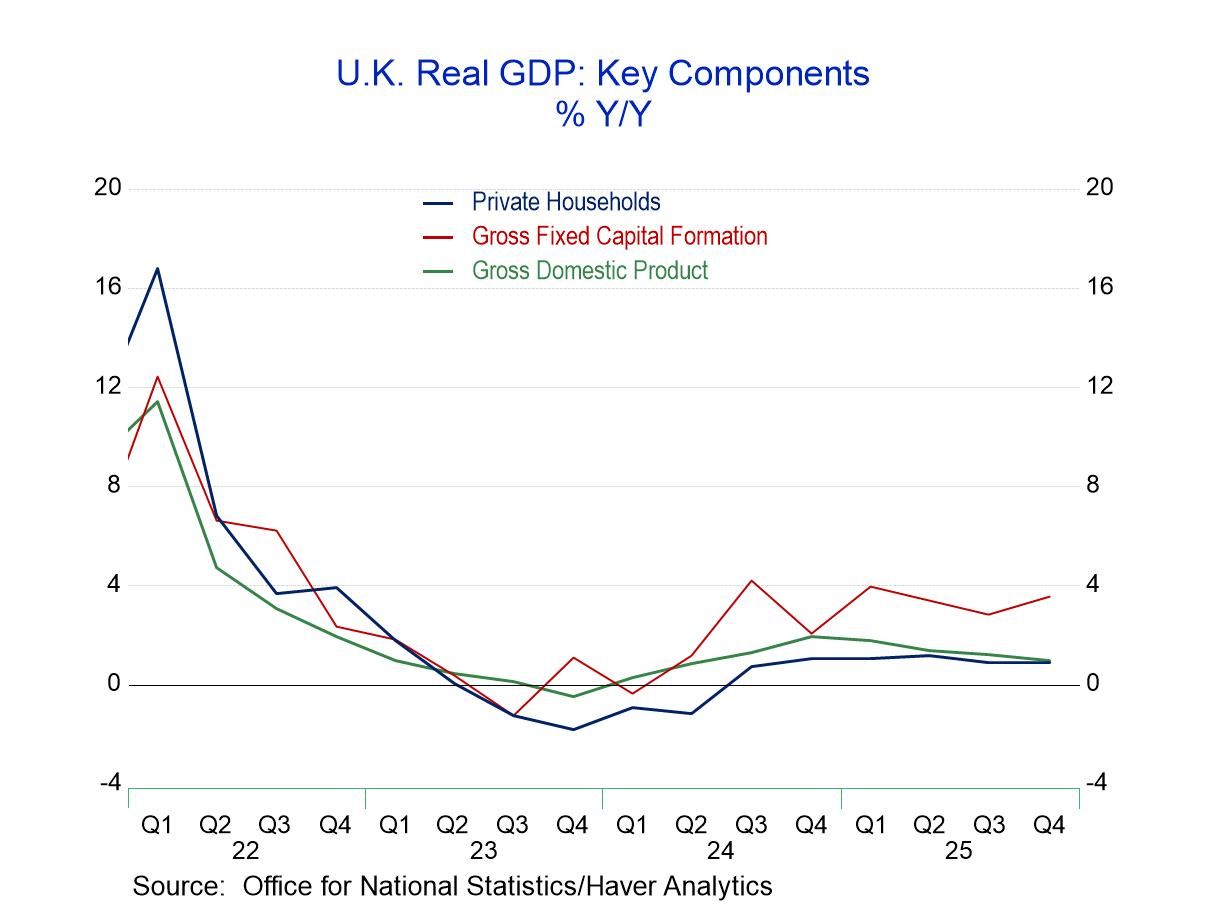

U.K. GDP slowed to a crawl at the end of the year, with growth at a 0.2% (annualized) rate logged in both the third and fourth quarters as 2025 drew to a close. The year had started with a strong 2.7% growth rate in Q1, which slipped to a 0.8% pace in the second quarter and decelerated to negligible growth at the end of the year.

These quarterly growth rates correspond to higher but obviously declining year over year growth rates. Because the quarterly growth rates diminished as the year progressed, year over year growth to start 2025 was at 1.8%; growth slipped to 1.4% in the second quarter and then to 1.2% in the third quarter. By the end of the year, growth had slipped to 1%.

The quarterly growth rates in the fourth quarter show public spending picked up to a 1.7% annual rate following 1% in the third quarter and erratic behavior in the first two quarters. Capital formation has remained relatively strong but has also oscillated, with first quarter growth at a blowout annual rate of 14.3%, falling to a contraction of 3.1% in Q2, rising back to 4.4% in Q3, and then declining at a 0.5% annual rate in Q4. So the year-over-year growth rates for capital formation during the course of the year only slipped from 4% in the first quarter to 3.6% in the fourth quarter, holding up fairly solidly and indicating strong rates of expansion for capital spending.

Housing, which was firm and strong in Q1 and Q2, slipped to a 0.8% annual rate of growth in the third quarter, and then housing investment fell at a 9.1% annualized rate in the fourth quarter. Year over year trends for housing show mostly low to moderate spending growth for residential investment.

U.K. exports have been floundering quarter-to-quarter, alternating between expanding and contracting; this corresponds to year over year growth rates that steadily diminish. In the first quarter of 2025, exports grew 3.5% year-over-year; that slipped to a 2% growth rate in Q2, then to a 1.5% growth rate in the third quarter. In the fourth quarter, U.K. exports are falling at a 0.5% annual rate of growth.

The export pattern contrasts with U.K. imports. They have mostly continued to grow, posting positive growth rates in three of the four quarters, starting the year with 5% quarterly growth and ending the fourth quarter with a 3.3% annual growth rate. Import growth rates have slipped, but not as much as other growth rates in GDP. For example, first quarter import growth was extremely strong at 7.6%; that year over year growth rate slips to 2.1% in Q2, then rises back to 5.3% in Q3, and finishes the year at 2.3%. There is slippage, but still significant growth, and the year began on a really high note.

Domestic demand has been fluctuating. In both quarterly and annual terms, there is unevenness. Quarterly growth rates range from 3.1% at an annual rate in Q1, to a 0.6% and 0.7% annual rate in the middle two quarters of the year; domestic demand ends the fourth quarter with a quarterly growth rate of 2.1% annualized. This causes year-over-year growth to be 2.9% in the first quarter; that falls to 1.2% in the second quarter, rebounds to 2.1% in the third quarter, and ends the year at 1.6% year-over-year.

Domestic demand has consistently been stronger than private consumption and it has been supported by both public consumption and by capital formation. Private consumption in 2025 has been erratic, logging 1.2% quarterly growth, annualized, in the first quarter; growth dropped to 0.2% in Q2, rising back to 1.7% in Q3, and then ending the year at a 0.6% rate of expansion quarter-over-quarter. The year-over-year data showed private consumption slipping but not dramatically, at a pace of 1.1% in the first quarter, up to 1.2% in the second quarter and then logging 0.9% in both the third and fourth quarters of 2025 as domestic demand ended the year stronger.

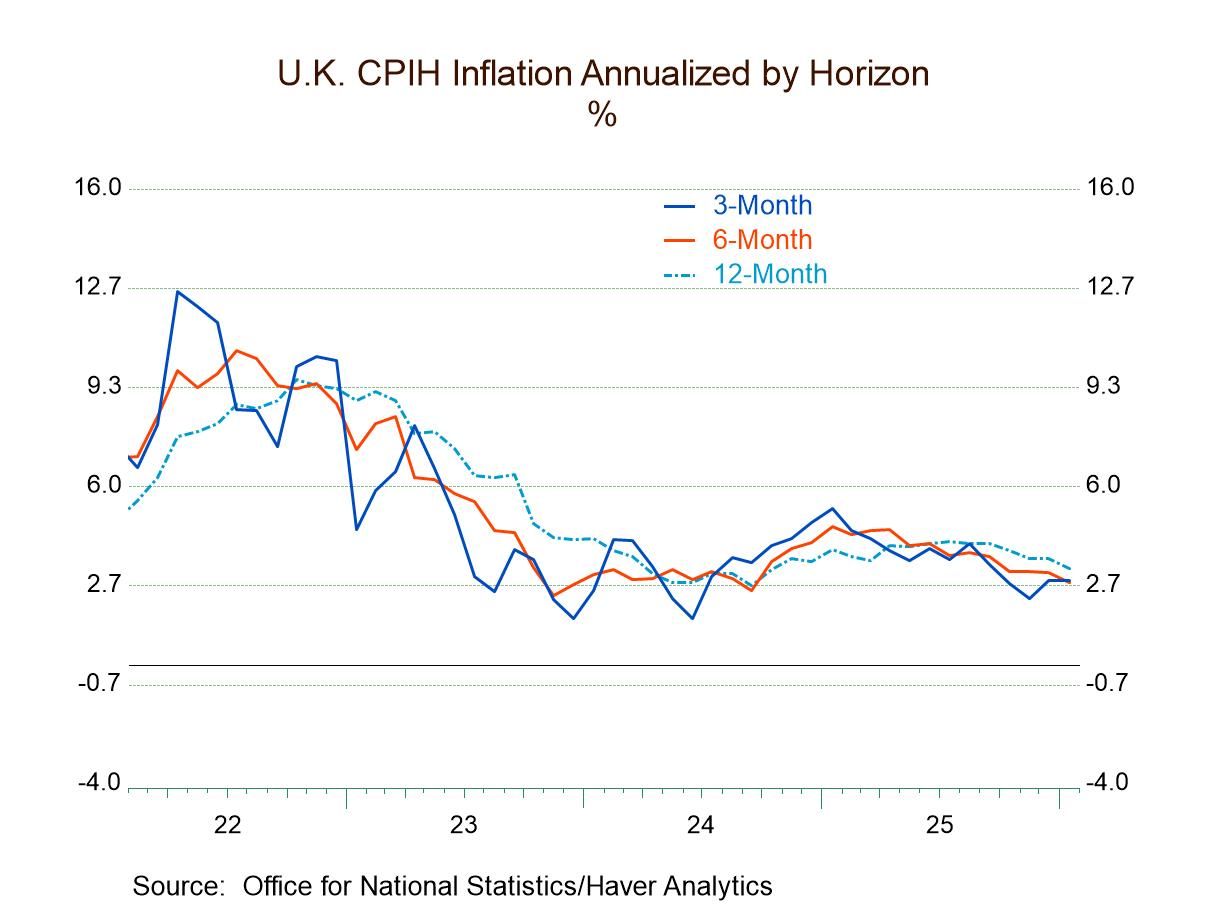

All of the U.K. growth rates are consistently and substantially below their five year growth rates. The economy continues to have a problem with inflation. Some recent inflation signals, however, suggest that there may be deceleration and progress, but the Bank of England hasn’t been convinced yet, even though Monetary Policy Committee members continue to speak favorably about the prospects for rate reductions ahead. The U.K. also has a corseted fiscal situation as there’s not much flexibility to spend more given its relatively bloated budget. The economy is waffling. The current administration has had its share of political issues, having recently had to eject several members from leadership positions in government. The outlook for growth is still touch and go. The outlook for inflation holds slightly more promise for deescalation. But overall, there is a lot of uncertainty over events and the growth path for the U.K. economy.

Global

Global