U.S. Consumer Confidence Falls Further in October; Inflation Expectations Edge Higher

by:Tom Moeller

|in:Economy in Brief

Summary

- Confidence level is lowest in six months .

- Present situation index increases but expectations decline.

- Inflation expectations remain contained.

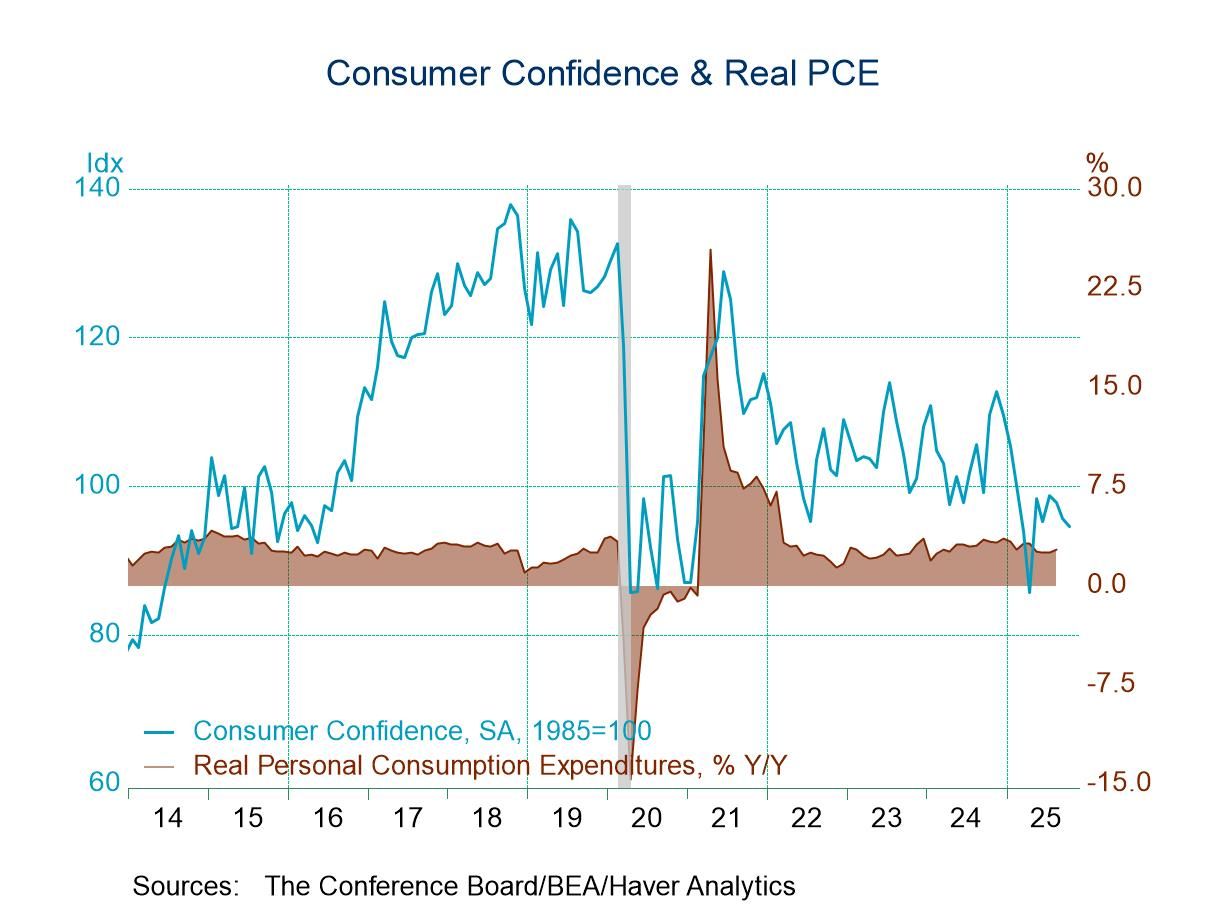

The Conference Board's Index of Consumer Confidence fell 1.0% during October (-13.7% y/y) to 94.6. A level of 93.6 had been expected this month in the Action Economics Forecast Survey. The decline in Consumer Confidence was the third consecutive monthly drop. It followed a 2.2% September shortfall, revised from -3.7%, and an unrevised 0.9% August decline. The index was 16.1% below its peak last November.

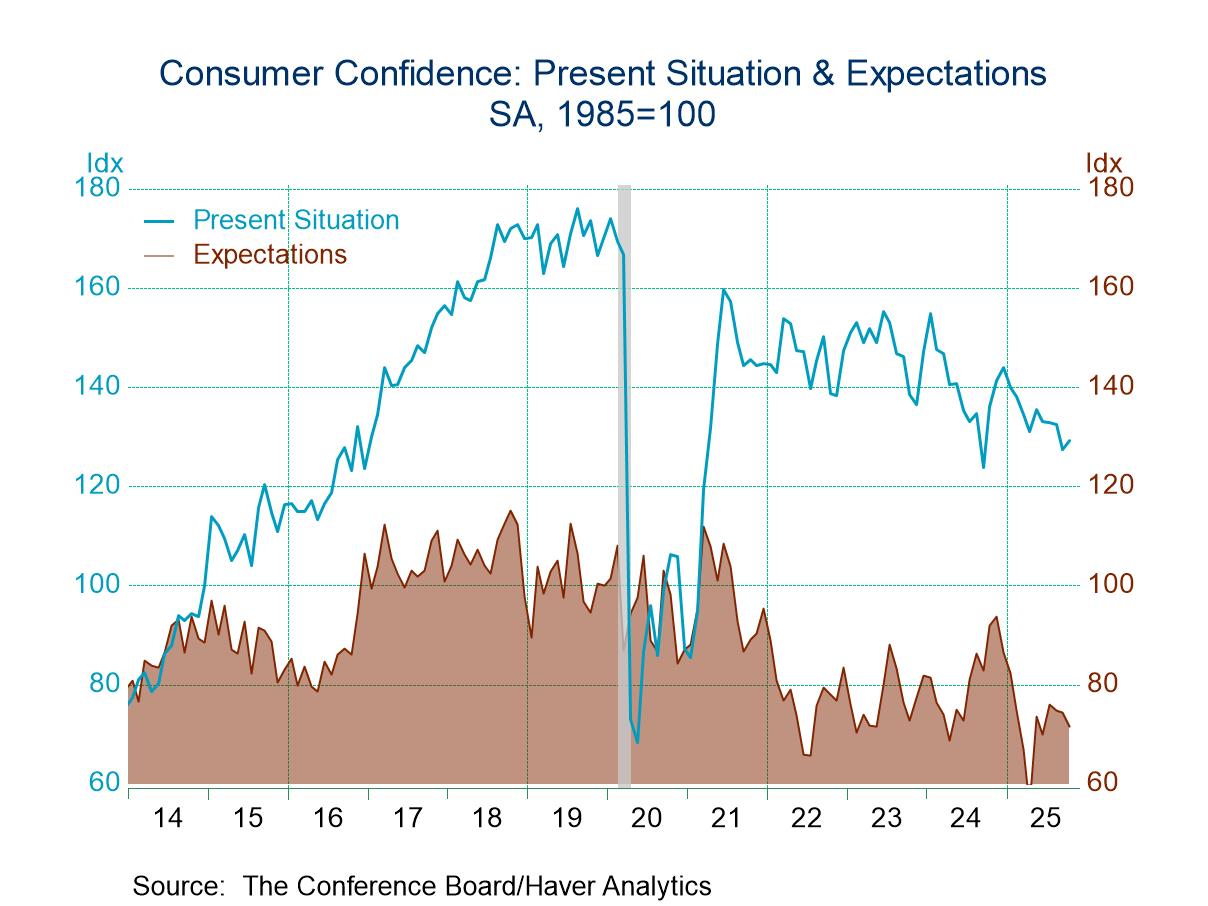

The Present Situation index rose 1.4% in October (-5.0% y/y) after falling 3.7% in September, revised from down 5.3%, after easing an unrevised 0.3% in August. The Expectations Index declined 3.9% this month (-22.2% y/y) after easing 0.4% in September, revised from a 1.7% decline.

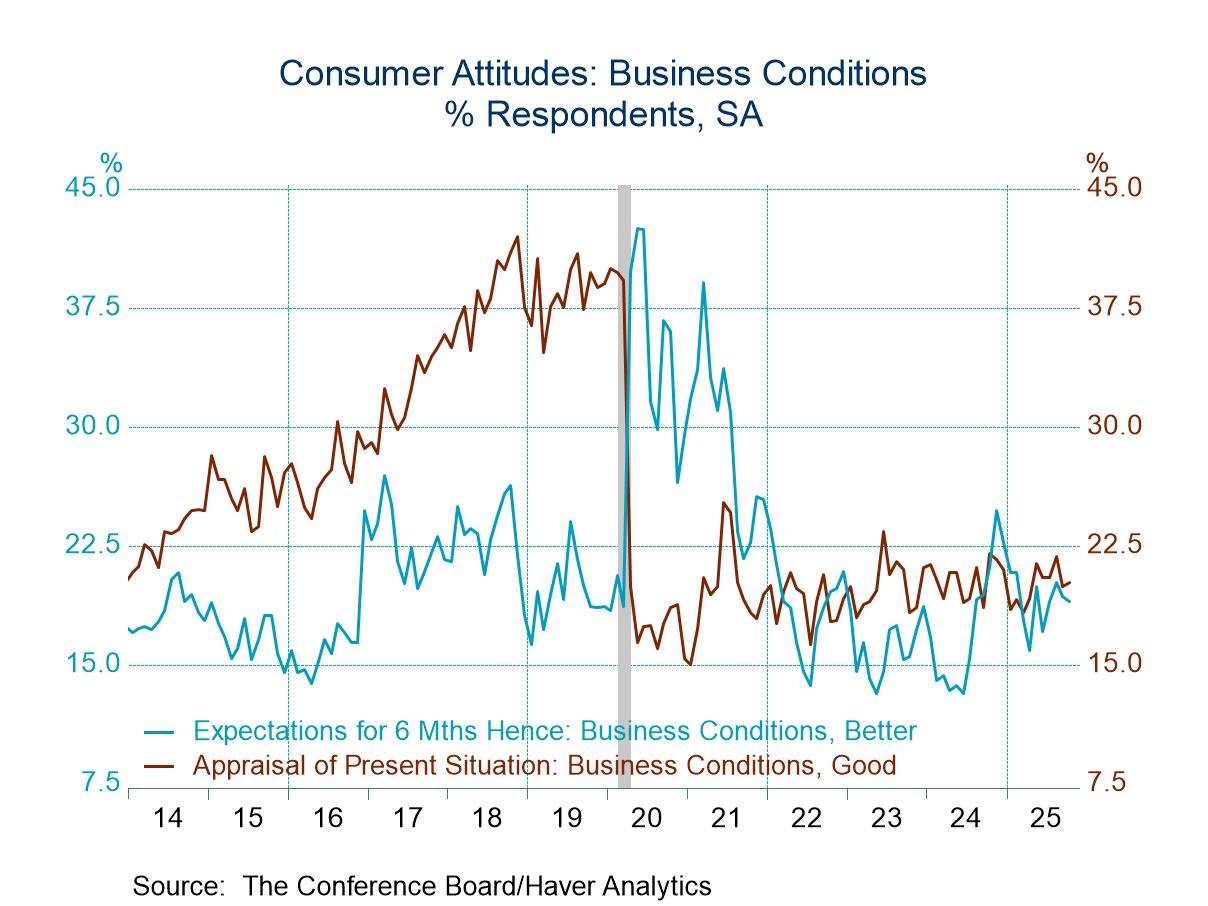

The percentage of respondents assessing business conditions as “good” rose to 20.2% in October after falling to 19.9% in September. It remained close to its weakest reading since April. The percentage assessing conditions as “bad” fell to 14.7% from 15.3% in September. The appraisal of labor market conditions improved as a slightly higher 27.8% described “jobs plentiful” versus 26.9% in September. That remained below a high of 56.7% in March of 2022. Jobs were viewed as “hard to get” by a fairly steady 18.4% of respondents this month, but that was increased from a low of 10.5% in February 2023. The labor market differential calculated by Haver Analytics (the percentage of consumers who think jobs are plentiful minus the percentage who believe that jobs are currently hard to get) rose to 9.4% compared to 8.7% in September and 11.1% in August. This measure remained below a high of 47.1% in March 2022. It has a 60% correlation with the unemployment rate over the last ten years.

Expectations for business conditions continued to deteriorate this month as a lessened 19.0% of respondents expect conditions to improve over the next six months, after 19.3% did so in September, while a steady 22.6% expect them to worsen, after rising from 23.5% in August. On employment, 15.8% expect the number of jobs to increase over the next six months versus 16.6% in September. The percentage expecting the number of jobs to decline in the next six months increased to 27.8% after easing to 25.7% in September. A lessened 17.9% of respondents expect income to increase in six months, down from 18.2% in September. That remained off a high of 20.7% in November of last year and compares to a 12.5% who expect income to decrease, up from 11.7% in September.

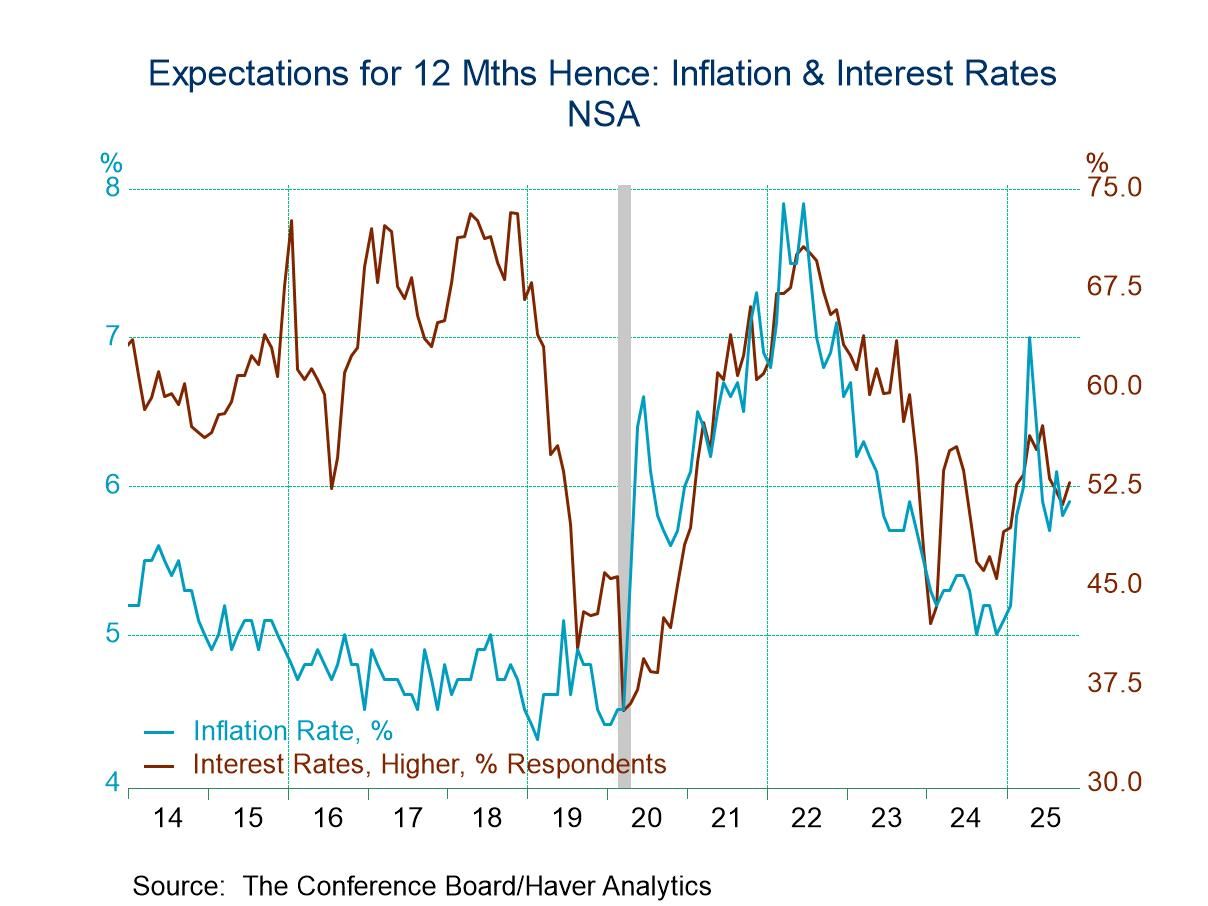

The expected rate of price inflation over the next twelve months edged higher to 5.9% in October from 5.8% in September. These remain up from a low of 5.0% last November. Fifty-three percent of respondents expect interest rates to rise this year, up from a low of 47.2% October of 2024. The percentage of respondents expecting equity prices to increase over the next twelve months held steady at 49.9%, the most since January. The percentage expecting a decline in stock prices increased to 28.5% after falling to 27.4% in September.

The percentage of respondents planning to buy a home fell to 5.7% this month and reversed two straight months of increase. Plans to purchase an automobile improved to 11.6% of respondents this month and mostly reversed the September decline to 11.4%. These readings remain up from a low of 10.6% in April.

The Consumer Confidence data are available in Haver’s CBDB database. The total indexes, which are indexed to 1985=100, appear in USECON, and market expectations are in AS1REPNA.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global

Global