U.K. Inflation Waffles and Percolates

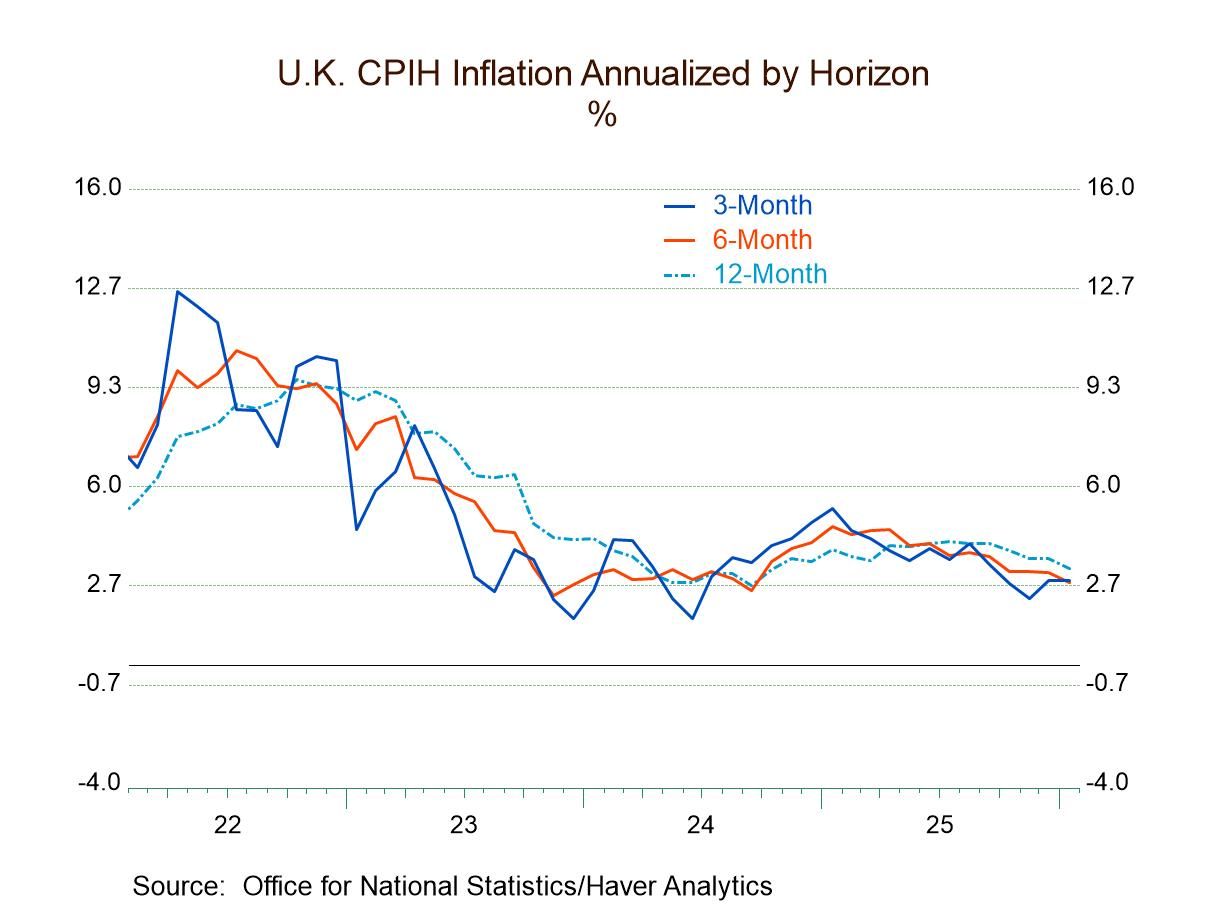

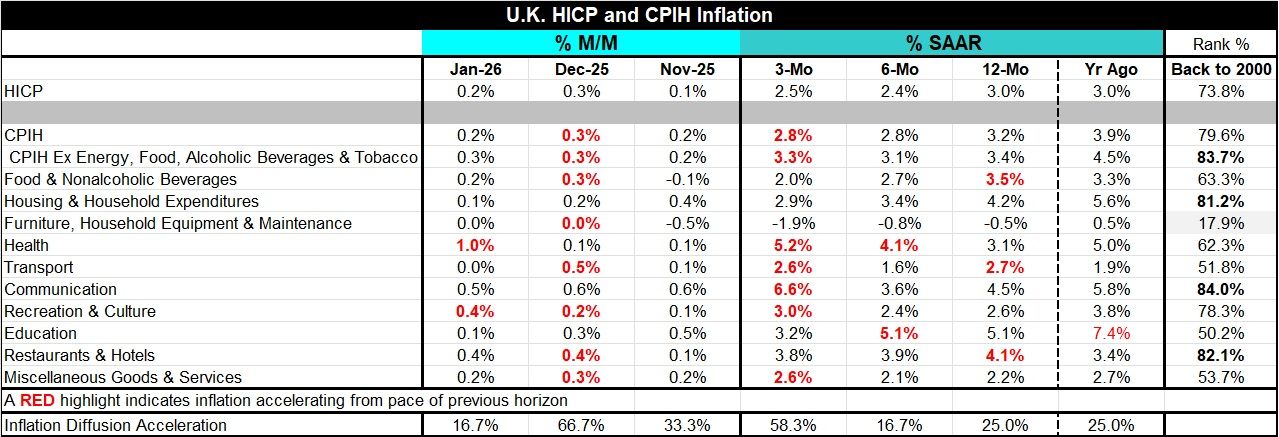

Inflation in the United Kingdom has irregularly downshifted over the past two months. In January, consumer price inflation remained steady at 2.8% over three months, the same pace as over six months. Core inflation ticked up to 3.3% over three months from 3.1% over six months but settled below the 12-month pace of 3.4%. Yet another measure, the HICP, comparable to the inflation rates reported by ECB numbers, logs 2.5% over three months, a slight uptick from six-month pace but less than the 12-month pace of 3%.

Diffusion The diffusion statistics that measure the breadth of acceleration of inflation across categories month-to-month came in at only 16.7% in January, down from 66.7% in December and compared to 33.3% in November. Diffusion readings below 50% indicate more deceleration than acceleration. So, inflation has been under control, with recent results showing more deceleration for inflation monthly than to accelerate. December was an exception. Over the 3 , 6 , and 12 month periods, inflation shows some acceleration tendency over 3 months, with diffusion at 58.3%; but that compares to 6-month diffusion at 16.7% and 12-month diffusion at 25%. Once again, the broad stroke for inflation, trending from 12 months to 6 months to 3 months, is showing more categories decelerating than accelerating.

Inflation rate ranking The final right-hand column ranks inflation rates on data back to 2000 based on their year-over-year performance. The current HICP, at 3%, has a 73.8 percentile standing among inflation rates back to 2000, marking it near the upper 25 percentile of the collection of results. The CPIH has a 79.6 percentile standing, putting it closer to the top 20% of observations over that same span. Core inflation at 3.4% has an 83.7 percentile standing, putting it in nearly the top 15% of results on data back to 2000.

Convergence around 2.8% The chart, supplemented by diffusion data, clearly shows that there is some inflation deceleration in progress; however, the level of year-over-year inflation still shows inflation among the upper ranges of what it's been over the last 25 years.

BOE A lot of attention is focused on the Bank of England and when it will cut rates. While there is some evidence of near term softness in inflation and certainly there is an evenness in economic growth and reason to wonder about the strength of economic growth, inflation results are still probably a little bit too high to allow for rate cuts at this point.

Summing up The Bank of England has a 2% inflation target and current numbers are hovering around or just below 3%. The only reading as low as 2.5% is the 3 month measure. The collection of results simply doesn’t show enough downward movement or stability at lower levels for the BOE to be taken seriously and for the bank to cut rates. Remember, of course, that when the central bank cuts rates, it's taking away some of the braking effects for interest rates on inflation. So, if inflation isn't where you want it and you cut rates, you're taking away a tool that is promoting the reduction of inflation to a lower level closer to your target. When you take that away, you’re acknowledging that you're going to allow inflation to progress more slowly toward the target. I'm not sure that's the signal that the Bank of England would like to make at this time.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global