Monetary Union Retail Sales Ease as Vehicle Sales Pop

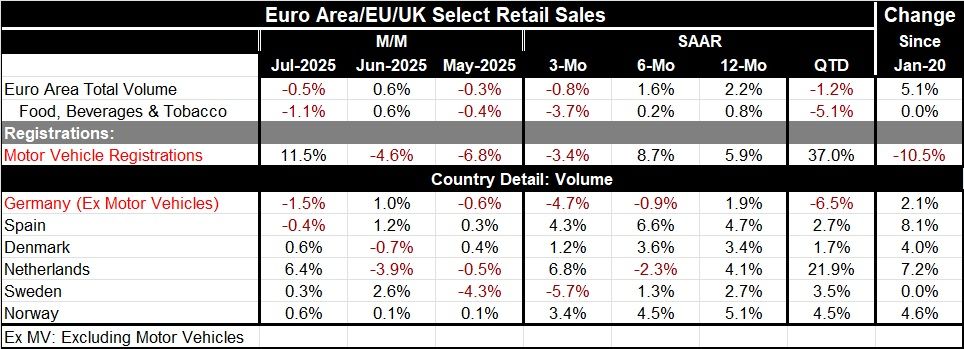

Retail sales volume in the euro area fell by 0.5% in July after rising by 0.6% in June. The three-month percent change is -0.8% at an annual rate; over six months real retail sales volumes are rising at a 1.6% annual rate and over 12 months they're rising at a 2.2% annual rate. The slowdown in retail sales volume growth has been steady from 12-months to 6-months to 3-months.

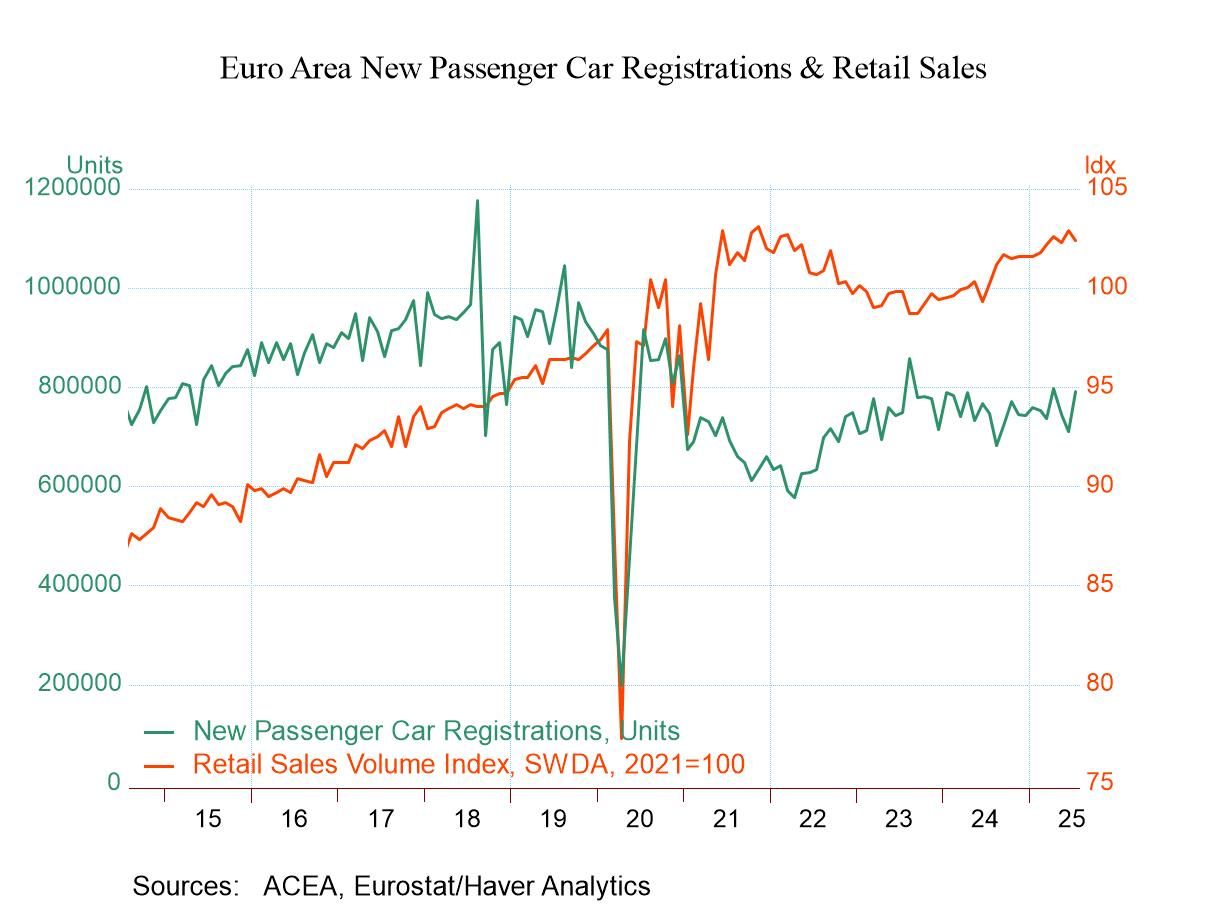

For motor vehicle registrations, the patterns are much choppier with an 11.5% increase in registrations in the EU in July after a drop of 4.6% in June, and a larger drop in May. Over 3 months monetary union motor vehicle registrations are falling at a 3.4% annual rate, after rising at an 8.7% annual rate over 6 months; over 12 months that gain is cut to a 5.9% annual rate. There's no clear trend here for motor vehicle registrations, except to note that over 3 months conditions are much weaker and that is mostly driven by June and May because July was quite strong. In the big picture, vehicle sales have been flat and moving sideways for quite some time in the monetary union- since COVID registrations are lower on balance by 10.5% even with the spike in sales in July.

Individual countries show quite different results. Germany is showing persistent deceleration in retail sales volume growth from 12-months to 6-months to 3-months, culminating in negative numbers for growth over 3 months and 6 months. For Denmark, a country that's not part of the single currency union, there's a hint of a slowdown with growth rates of 3.4% over 12 months and 3.6% over 6 months to give way to a 1.2% rate of increase annualized over 3 months. Both Sweden and Norway show real retail sales volumes in a slippage mode as growth rates ease over 6 months compared to 12 months and then ease again over 3 months compared to 6 months. For Sweden, the 3-month growth rate is a negative result at -5.7% at an annual rate.

In the quarter to date - and this is an early calculation since it's July - the monetary union is starting off with a negative growth rate of -1.2% at an annual rate for total retail sales volumes; this is affected strongly by a -6.5% annual rate reported by Germany, the largest economy and the euro area. There are positive growth rates on a quarter-to-date basis for the rest of the reporters in the table. The Netherlands logs a 21.9% annual rate increase; that strength has at least as much to do with the weak second quarter base as with surging sales in July.

Checking on the performance of sales back to January 2020 when COVID first appeared, total sales volume in the euro area are up 5.1% over that five-year span. Sweden logs no increase, Germany logs an increase of 2.1%, Norway logs an increase of 4.6%, with Denmark up by 4%. The strongest increases on this broad basis come from Spain with an 8.1% increase and the Netherlands with a 7.2% overall increase. Even so, for a five-year period, none of these growth rates are impressive. Clearly the European Monetary Union has been in a dead spot having a difficult time recovering from COVID, dealing with the war, and all of its displacement involving Russia and Ukraine, as well as the aftermath of the inflation from COVID, and what has been an ongoing restrictive monetary policy from the European Central Bank.

Mixed results and trends in retailing

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global