Job Openings and Labor Turnover (JOLTS): Mixed Results in March

Summary

- Job openings were little changed...

- ...but hirings and layoffs picked up.

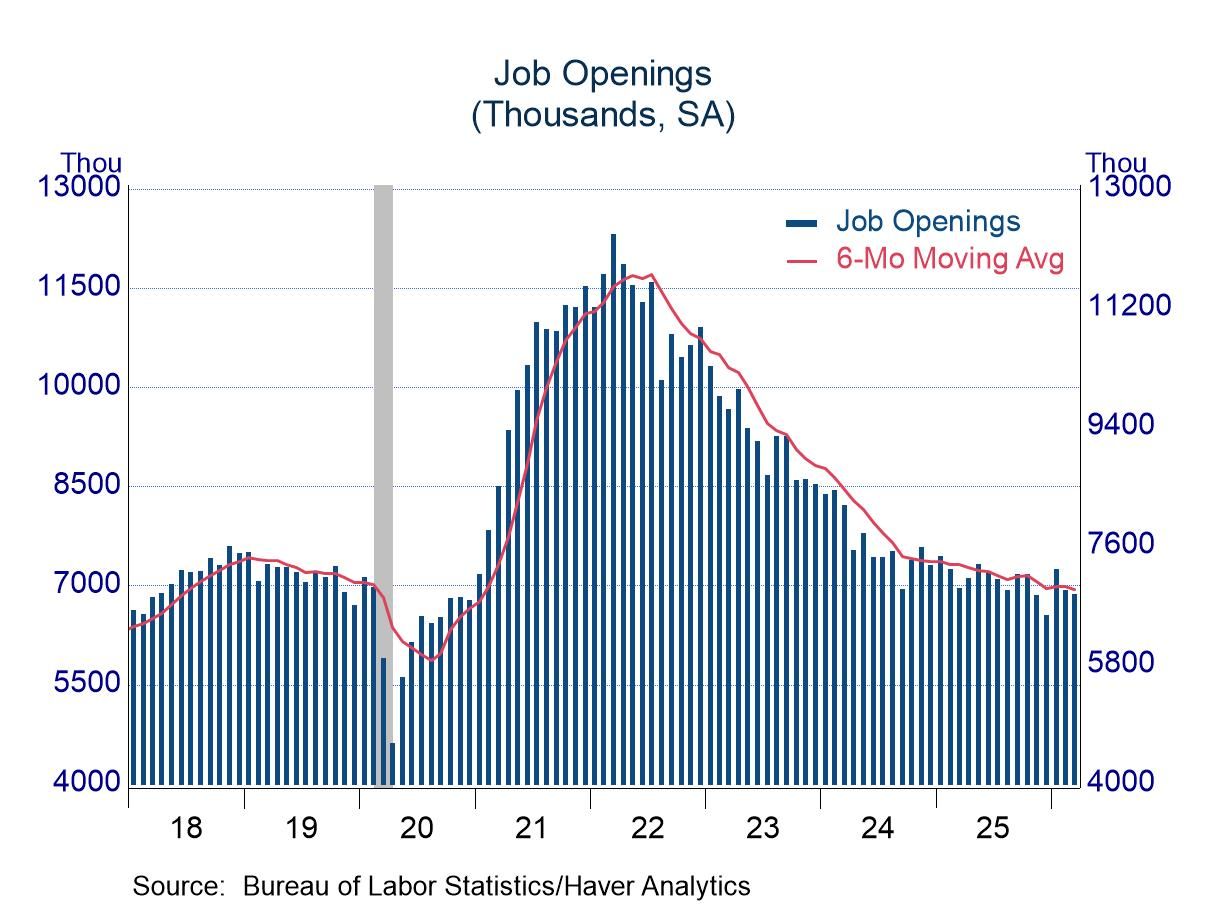

The number of job openings fell slightly in March (off 0.8%), but the new total remained within the range of recent observations, with the monthly ups and downs tracing the slightest of downward drifts. Most industries posted increases in available jobs, but a sharp drop in the business services sector provided an offset. Interestingly, the business services sector also was active in hiring during March, which might explain the drop in openings. Considering the industry detail, the decline in job postings was not especially troubling.

Although the number of job openings fell in March, the number of unemployed individuals fell by a larger amount (off 332,000; published with the monthly employment report), leaving an improvement in the ratio of openings to unemployed. The new reading of 0.95 still indicates that there is less than one job per unemployed individual, but it is an improvement from 0.91 in February. Recent readings in this ratio are still respectable relative to the long-run historical experience, but they are below observations near 1.2 in the years immediately before the pandemic and well below readings close to 2.0 during the post-pandemic surge.

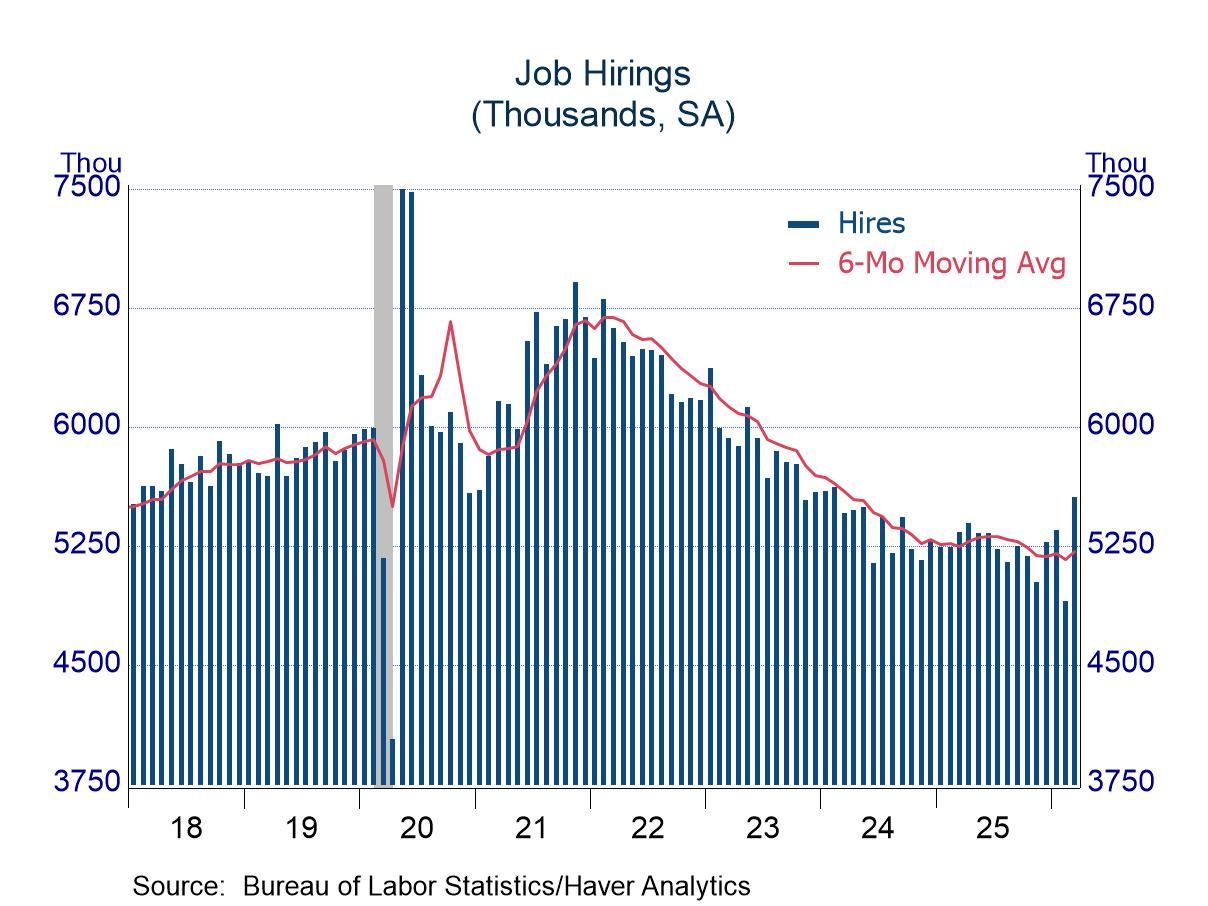

Businesses have been cautious in hiring in the past year or so, but they became more active in March, with hirings increasing 13.4%. The new level of hirings was the best since early 2024. Retail establishments were active in hiring, and as noted, firms in the business services area also brought on more workers.

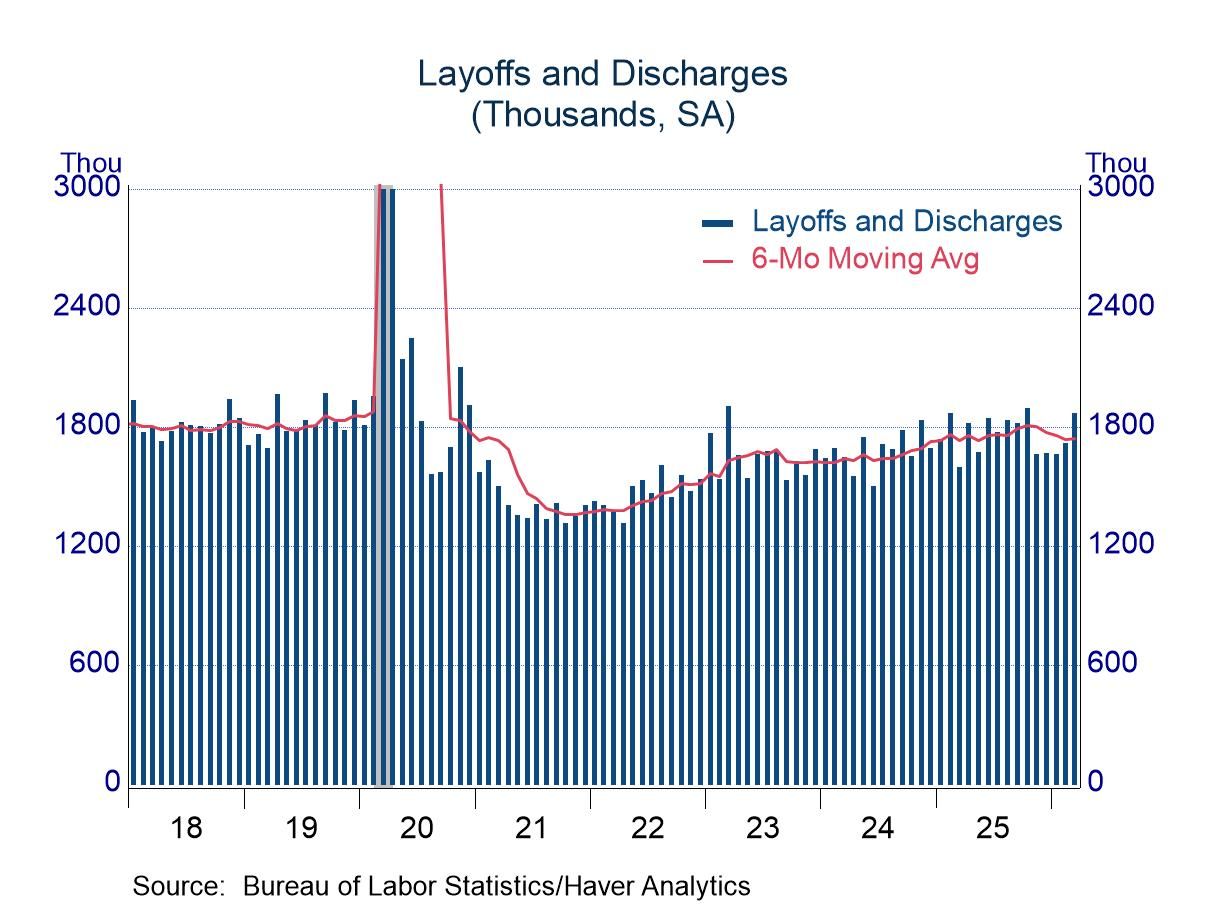

Hiring picked up in March, but layoffs increased as well (up 8.9%). The move was sizeable, but it also might be viewed as random volatility, as this series often shifts widely from month-to-month and it remained within its recent range. The latest reading might be an offset to light observations around the turn of the year. The fact that nonfarm payrolls rose sharply in March (up 178,000) also indicates that layoffs in that month were not troubling.

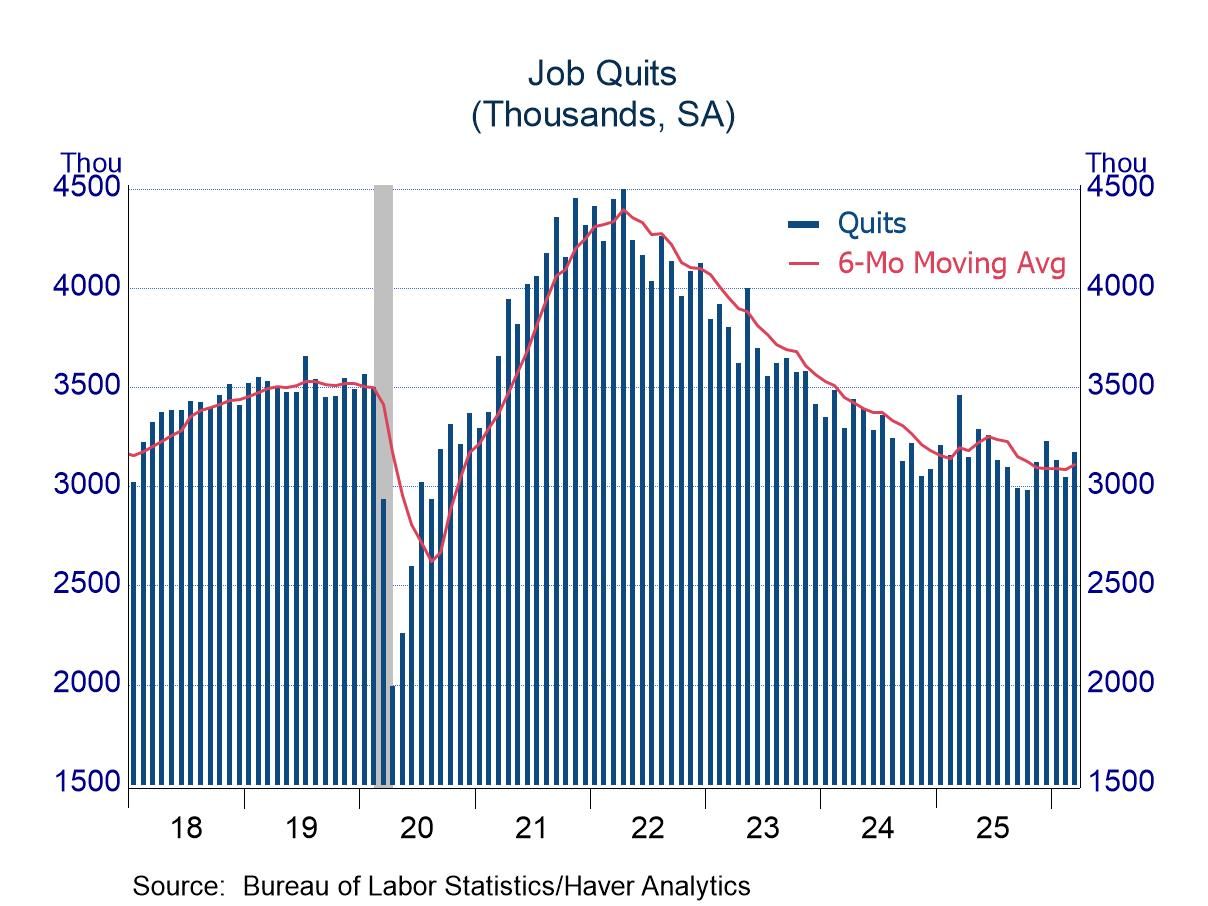

All told, the JOLTs report for March might be viewed as mildly favorable; or at least the decline in openings and the increase in layoffs should not stir concern. A pickup in the number of quits in March (up 4.1%) might suggest that individuals perceive improved prospects in finding a new job. However, the number of quits has waxed and waned in recent months, leaving an ambiguous trend. Certainly, a clear upward trend has not emerged.

The Job Openings and Labor Turnover Survey (JOLTS) data are available in Haver’s USECON database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia