Japan’s PPI Plods Ahead

Japan’s PPI data reveal that not all the inflation measures are flashing danger or warning signals. Japan's preferred CPI gauge that excludes energy & fresh food, for example, is one of the hottest gauges of inflation. It happens to be the gauge that the Bank of Japan emphasizes the most and so it has put policy somewhat on edge worried about inflation.

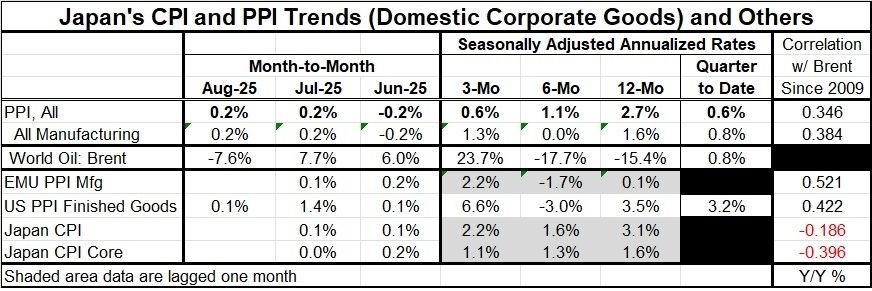

However, the other Japanese metrics are not showing the same degree of inflation that that one is showing. The PPI from Japan was up by 0.2% for the second month in a row in August after falling by 0.2% in June – a very restrained performance. The 12-month inflation rate is 2.7% that falls to 1.1% over six months, then to 0.6% over three months – all at annual rates. For all of manufacturing, the PPI is up by 1.6% over 12 months, flat over six months and then back up to 1.3% over three months; none of these are particularly troubling inflation gauges although I recognize that the PPI is not the CPI and this is not the target of monetary policy.

Still, for Japan, it's reassuring to see that inflation is not simply running wild. In fact, when viewed in several different ways, it's actually rather controlled.

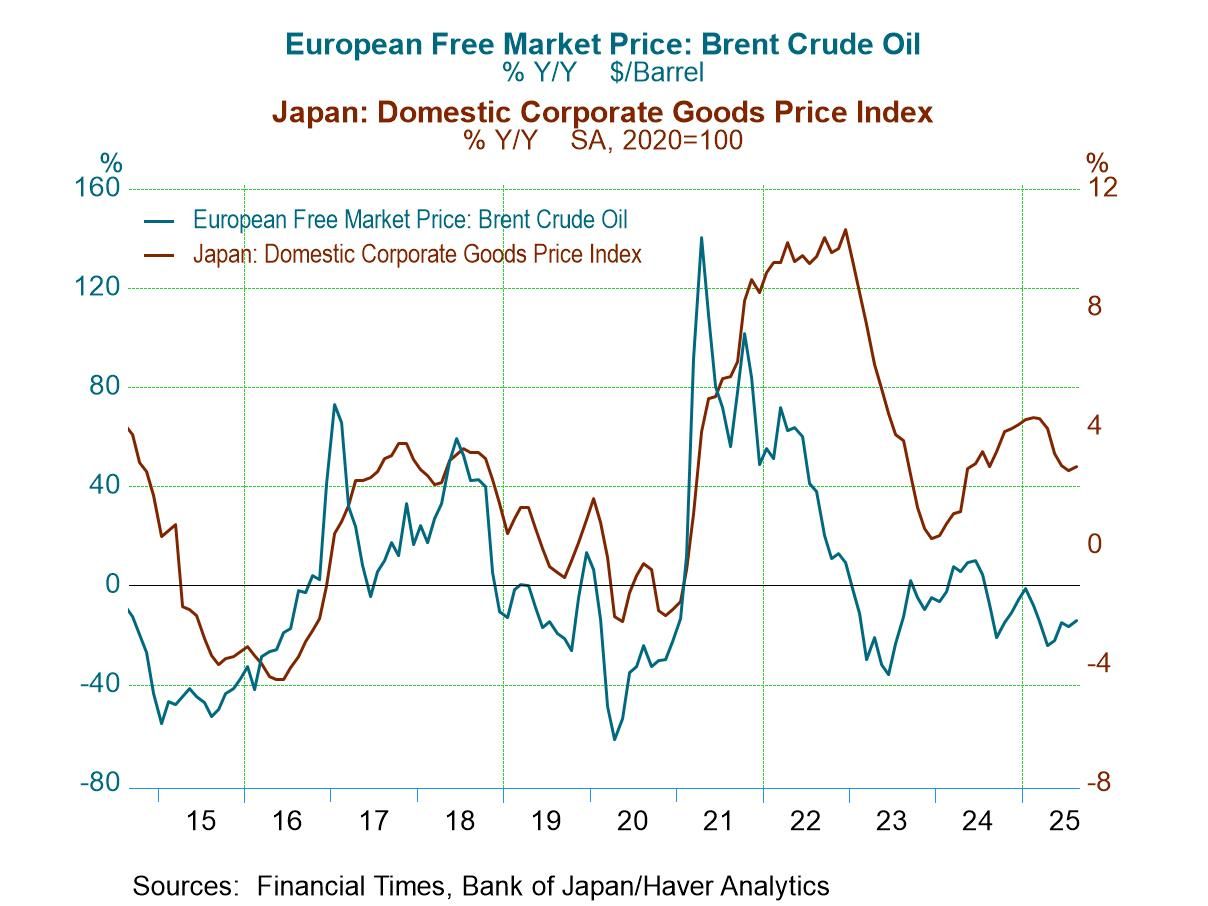

Viewing inflation in Japan and the context of trends in the United States and then the European monetary Union, we find that the broad pressure inflation is concentrated in the U.S. although it may not be tariff-related. In Europe, inflation is broadly controlled. The U.S. is showing the most pressure and of course it has the strongest economy, and it also has an ongoing problem with tariffs that are putting some extra measure of pressure on prices. The U.S. PPI generates a very strong inflation rate over three months - and even an elevated 12-month reading of 3.5%. However, we don't see anything like that coming out of the European Monetary Union where year-over-year inflation is barely positive even though over the most recent three months inflation has accelerated to a 2.2% annualized rate. That's still a relatively subdued rate.

In Japan, the ordinary CPI and the core show relatively subdued inflation over the last year. The headline CPI is 3.1% over 12 months, but it dives under 2% over six months and to a 2.2% pace over three months. Japan's core is only 1.6% over 12 months and its annual rates are under 2% for six months as well as for three months. The inflation situation in Japan, particularly for producer prices, seems to be in pretty good shape with the quarter-to-date inflation rate for the PPI at 0.6% and for all of manufacturing at 0.8%. With oil prices remaining moderate, the outlook for inflation to remain in this more moderate range is still good, and Japan continues to have weak growth; demand should not be putting pressure on inflation. The Bank of Japan should be relatively happy with Japan's producer price number, the domestic corporate goods price index for August.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global