IP in EMU Remains Weak

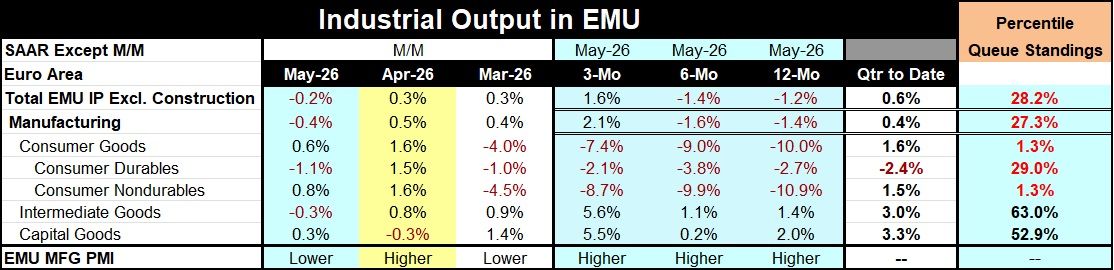

Industrial production in the European Monetary Union (EMU) shows only a very minor and idiosyncratic sector acceleration in the nondurable goods sector. Other sectors show trends that are not focused and drift into random variability. Nondurable goods output shows growth of -10.9% over 12 months, improving to a pace of -9.9% over six months annualized and improving further to -8.7% annualized over three months. The irony is that nondurable output is contracting over all these periods, but the contractions are becoming slightly less virulent. It is nothing to base any optimism on despite the technically ‘improving’ trend.

Total output and manufacturing output in the EMU each show strong gains annualized over three months after declines on balance over six months and 12 months.

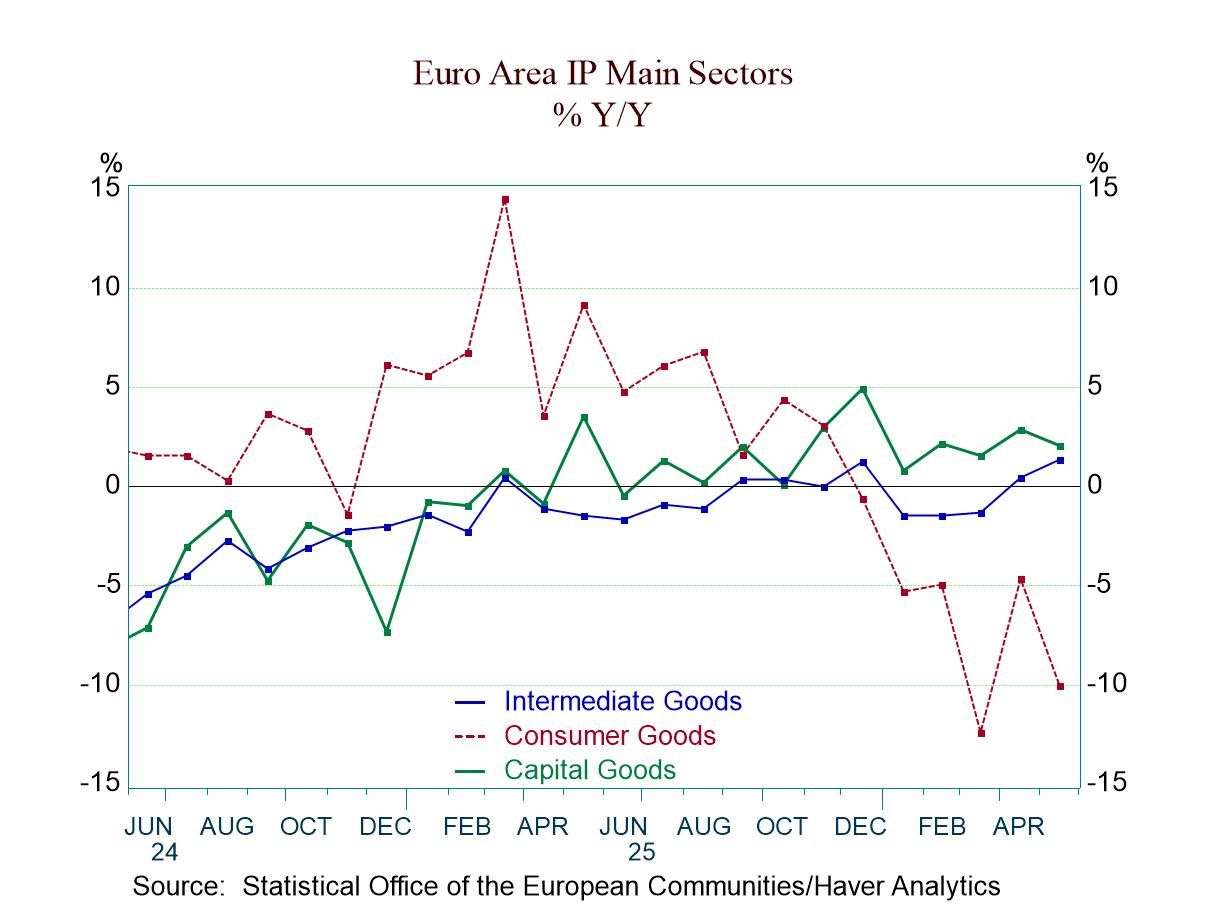

While the secular trends are not clear in showing persistent accelerations or decelerations for the most part, it's true that output across the consumer industries continues to show contraction on all timelines. When we move to intermediate goods and capital goods, we're looking at output showing increases over 12 months, six months, and three months. Even if there are not clear progressions, the persistence of output gains is notable. This again underscores the extent to which expansion is being carried ahead by business and not by the consumer, even in Europe.

On a quarter-to-date (QTD) basis (two months into the second quarter), output is generally showing increases, with the exception of consumer durable goods showing an output decline at a 2.4% annual rate. Top-line growth is still very unimpressive, with total industrial production at a 0.6% annual growth rate and manufacturing alone at a 0.4% annual growth rate; neither of these is strong, solid, or impressive.

Turning to the percentile standing data that evaluate the strength of year-over-year growth on a historic timeline, we see that manufacturing and total output growth log percentile standings just below the 30th percentile. Consumer goods, as an aggregate category, have a 1.3% standing, which is extremely weak. That standing consists of a 29% standing for consumer durables and a 1.3 percentile standing for consumer nondurables output.

Once again, it is intermediate and capital goods that are the backbone of support for output. Intermediate goods’ annual growth rate has a 63-percentile standing, and the year-over-year growth rate for capital goods has a 52.9 percentile standing. Both being above the 50% mark puts them above their median for the period of analysis; that period extends back to August 2006, roughly a 20-year period.

I previously reported on the country detail. The country detail shows accelerating manufacturing output in Ireland, Portugal, and Sweden (Sweden that is not a monetary union member). Austria, a monetary union member, shows persistent deceleration, while the rest of the countries in the group show somewhat chaotic patterns.

While the percentile standing for year-over-year growth in manufacturing is at the 27th percentile mark for the whole of the monetary union, that amalgamation includes size weighting for that evaluation. If we take the unweighted averages for the percentile standings for 11 of the oldest monetary union members, their average individual ranking is much higher at a 48.3 percentile mark. Clearly, there are great differences by country across the monetary union, and this gives the ECB an additional headache in trying to make one monetary policy for such a varied group of economies.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief