How to Turn a Tariff-Induced One-Time Increase in Inflation into Higher Sustained Inflation

|in:Viewpoints

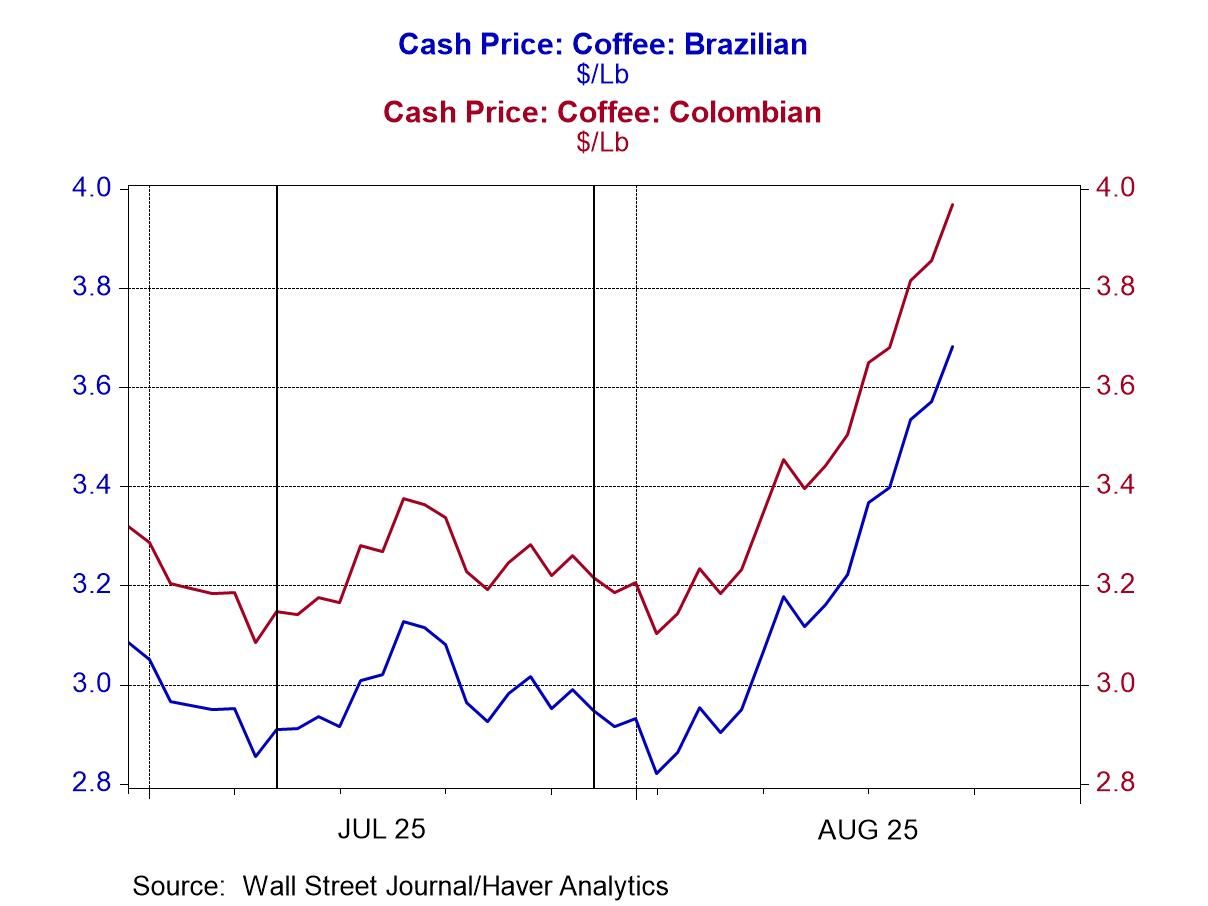

Supreme Court Justice Kavanaugh said during his confirmation hearing that he liked beer. When my confirmation hearing for governor of the Federal Reserve comes up, I am going to tell the Senate Banking Committee that I like coffee. At a minimum, I drink six cups a day. You might say that my demand for coffee is price inelastic, that is, increases or decreases in the price of coffee do not change the quantity of coffee I purchase much. As Chart 1 shows, the wholesale price for coffee has jumped since President Trump announced a 50% tariff on Brazilian coffee. On July 9, 2025, President Trump notified the government of Brazil that he intended to place a 50% tariff on US imports of Brazilian-produced goods. Then on July 30, President Trump imposed the 50% tariff, excluding orange juice and commercial aircraft. (I guess the US airlines and orange juice sellers have strong lobbies). From July 9 through August 22, the wholesale price of Brazilian coffee has increased 77 cents or 26%. The wholesale price of Columbian coffee, a substitute for Brazilian coffee, has also increased 26% in the same time period.

Chart 1

I stated that my demand for coffee was price inelastic. A 26% increase in the price of coffee is unlikely to cause me to cut back much on the quantity of coffee I purchase. But if my nominal income does not increase commensurate to the increase in my nominal expenditures on coffee, I will be forced to cut back on my nominal purchases of other goods and services. Assume that I am not unique with regard the price elasticity of demand for coffee. If so, then, in the aggregate, households will be forced to cut back on their nominal purchases of non-coffee goods and services if their nominal income does not increase. The result of this will be a decline in the prices of non-coffee goods and services. Thus, the price of coffee will increase, but the general (all inclusive) price level need not increase because the prices of non-coffee goods and services will decrease.

The effect of the 26% increase in coffee prices on the general price level changes if nominal incomes increase. In this case, households need not cut back on their purchases on non-coffee goods and services in the face of an increase in the price of coffee because their nominal incomes have increased.

We can generalize about the effects of a tariff-induced price increases on the general price level. The quantity demanded of most goods and services is sensitive, to a larger or smaller degree, to price changes of these goods and services. So, a tariff-induced price increase of a good/service will result in some decline in the quantity demanded of the good/service, but not the total cessation of purchases of the good/service. Thus, if personal income does not increase, the tariff-induced price increase of a good/service will result in some decline in the amount of other goods/services purchased and a decline in the prices of some of these goods/services.

Now, let’s move from levels to rates of change. If a tariff-induced price increase is not accompanied by an increase in the rate of change in personal income, the tariff will result in a one-time increase in the inflation rate. Then inflation will return to its pre-tariff rate. However, if a tariff-induced price increase is accompanied by an increase in the rate of growth of personal income, then the tariff will result in a sustained higher rate of inflation.

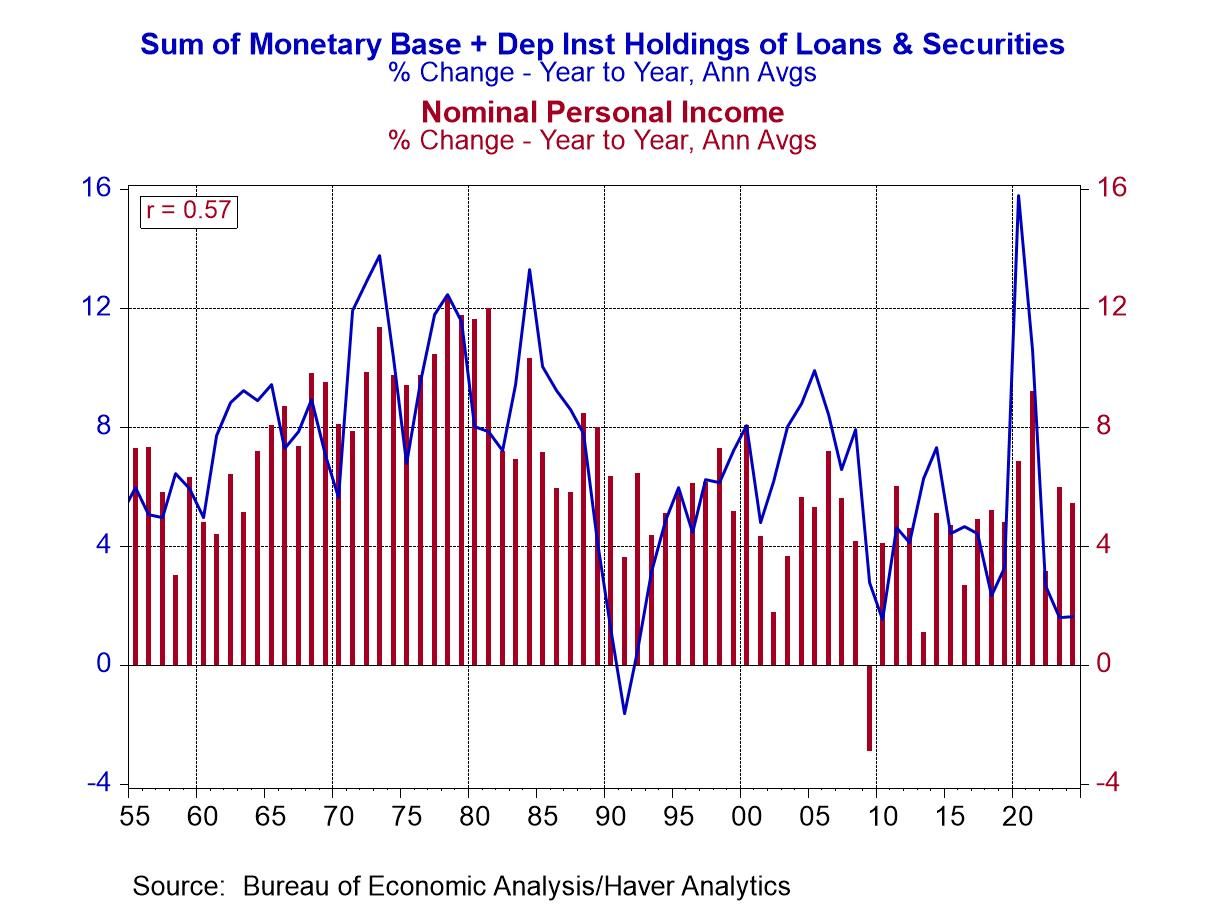

And do you know what can have a positive effect on the rate of growth of aggregate nominal personal income? Yep, an increase in thin-air credit. (Similar to coffee, I am addicted to the concept of thin-air credit.) Plotted in Chart 2 are the year-over-year percent changes in average annual thin-air credit (the sum of the monetary base plus depository institution holdings of securities and loans) and in average annual nominal Personal Income starting in 1955 through 2024. The correlation coefficient between the two series is positive 0.57. If the two series were perfectly correlated, the coefficient would be 1.0. I have tested the lead-lag relationships, and the highest correlation occurs between the two series contemporaneously. Although the correlation coefficient declines to 0.53 when thin-air credit growth is advanced by one year (that is, thin-air credit “causes” Personal Income), it declines to 0.37 when Personal Income growth is advanced by one year. So, it would appear that growth in thin-air credit does cause nominal Personal Income growth.

Chart 2

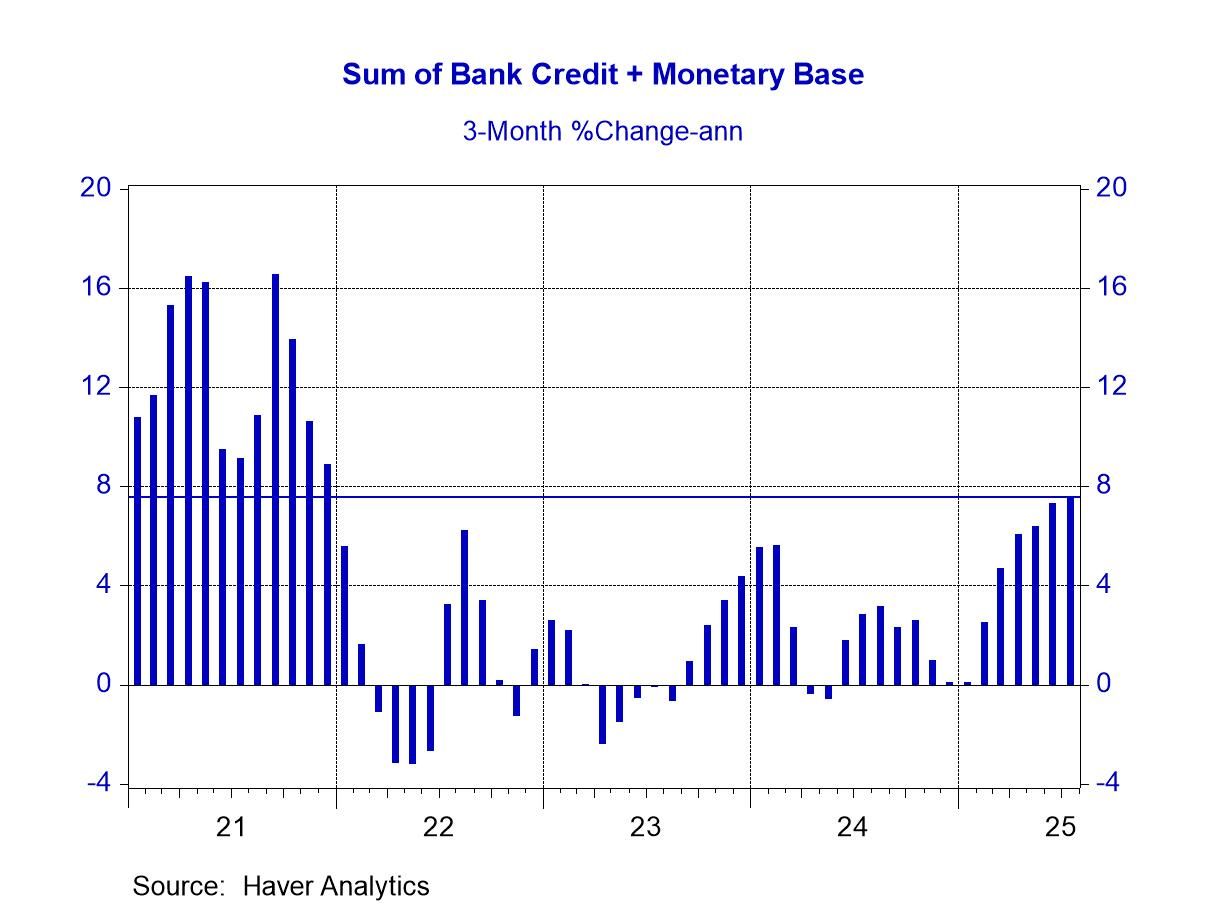

Now, let’s get current. In the three months ended July 2025, the sum of commercial bank credit and the monetary base increased at an annualized rate of 7.6% (see Chart 3). This is the fastest 3-month growth in this narrower version of thin-air credit since December 2021. At this year’s Kansas City Fed sponsored Jackson Hole barbecue (again, my invitation must have been lost in the mail), Fed Chairman Powell’s remarks were interpreted by the financial markets that the Federal Open Market Committee would cut its federal funds target by a quarter of a percent from its current level of 4.33% at its upcoming September 16-17 meeting. All else the same, a cut in the federal funds rate would result in faster growth in thin-air credit. And faster growth in thin-air credit would result in faster growth in nominal personal income.

Chart 3

In conclusion, if the nominal Personal Income growth rate does not increase in the face of a tariff increase, the effect of the tariff increase on the rate of inflation would be, at worst, a one-time increase in the inflation rate, with inflation returning to its pre-tariff rate. However, if the nominal Personal Income growth rate increases in the face of a tariff increase, the effect of the tariff increase on the rate of inflation would be a higher sustained inflation rate. And the empirical evidence suggests that the growth in thin-air credit is an important factor in determining the growth in nominal Personal Income. In the grand scheme of things, a quarter of a percent cut in the federal funds rate on September 17 is not going to radically increase the growth in thin-air credit and nominal Personal Income. But if this is the first in a series of cuts in the level of the federal funds rate, then the Fed is going to ignite another round of higher inflation.

Paul L. Kasriel

AuthorMore in Author Profile »Mr. Kasriel is founder of Econtrarian, LLC, an economic-analysis consulting firm. Paul’s economic commentaries can be read on his blog, The Econtrarian. After 25 years of employment at The Northern Trust Company of Chicago, Paul retired from the chief economist position at the end of April 2012. Prior to joining The Northern Trust Company in August 1986, Paul was on the official staff of the Federal Reserve Bank of Chicago in the economic research department. Paul is a recipient of the annual Lawrence R. Klein award for the most accurate economic forecast over a four-year period among the approximately 50 participants in the Blue Chip Economic Indicators forecast survey. In January 2009, both The Wall Street Journal and Forbes cited Paul as one of the few economists who identified early on the formation of the housing bubble and the economic and financial market havoc that would ensue after the bubble inevitably burst. Under Paul’s leadership, The Northern Trust’s economic website was ranked in the top ten “most interesting” by The Wall Street Journal. Paul is the co-author of a book entitled Seven Indicators That Move Markets (McGraw-Hill, 2002). Paul resides on the beautiful peninsula of Door County, Wisconsin where he sails his salty 1967 Pearson Commander 26, sings in a community choir and struggles to learn how to play the bass guitar (actually the bass ukulele). Paul can be contacted by email at econtrarian@gmail.com or by telephone at 1-920-559-0375.