Holy Rate Cut Batman...

by:Joel Prakken

|in:Viewpoints

...was the reaction in financial markets after the latest employment report showed that, including revisions, growth of establishment employment slowed to a crawl over the last three months. Investors, who before that report were convinced the Fed will maintain its policy rate in the range of 4¼% - 4½% at the September meeting of the FOMC, are now equally convinced the Committee will cut the rate by ¼ percentage point, a shift in sentiment re-enforced by dovish remarks delivered by Chair Powell at the Fed’s annual shindig in Jackson Hole.

While not religious about it, I do find the Taylor rule a useful framework for contemplating the short-run dilemma facing the Fed as it attempts to satisfy the dual mandate of low inflation and high employment. For a given “neutral” real (i.e., inflation-adjusted) federal funds rate – today we call it real “r-star” – the original rule showed the Fed: (1) raising (lowering) the nominal policy rate by 50 basis points for each percentage point that real GDP exceeds (falls short of) potential GDP; (2) raising (lowering) the policy rate by 150 basis points for each percentage point that inflation exceeds (falls short of) 2%. The value of real r-star itself is not observed directly, only inferred from empirical models. However, the Fed’s Summary of Economic Projections (SEP) reveals policymakers’ views on the matter. For example, the June SEP shows, in the long-run, inflation of 2% and a nominal funds rate of 3%, implying a value of real r-star of 1% - unchanged from December’s SEP.

Another familiar rule in macro is Okun’s law relating changes in the unemployment gap to changes in the output gap. Using a typical textbook version of Okun’s law, the Taylor rule can be restated to show the Fed lowering (raising) the funds rate by 100 basis points for every percentage point that the unemployment rate exceeds (falls short of) the full-employment rate. The current unemployment rate is 4.2%, slightly below CBO’s estimate (= 4.3%) of the “non-cyclical” unemployment rate, while the 12-month change in the core PCE price index is 2.8%. If real r-star is 1%, then current values of the unemployment rate and inflation imply an appropriate policy rate of 4.3%, exactly equal to the funds rate in July.

From this perspective the Fed should be in no hurry to ease policy and, by cutting rates, risks perpetuating inflation above the 2% objective. The argument for a rate cut is that continued slow growth of employment will soon lead to rising unemployment that, through the Phillips Curve, will reduce inflation risks associated with a one-off increase in tariffs, allowing the Fed preemptively to shift its focus to the employment half of the dual mandate.

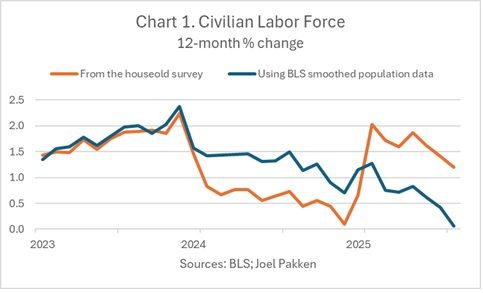

This is a demand-side narrative that may prove out, but there is a supply-side story to tell here as well. With each employment report the BLS publishes monthly data on the labor force that tautologically is the product of population and the labor force participation rate. In Chart 1, the orange line depicts the recent 12-month percent change of this series. Unfortunately, it is contaminated by “population controls” introduced by the BLS each January. Fortunately, the BLS publishes alternative monthly estimates of employment by age and gender that smooth through the population controls. By multiplying the reported participation rate into this alternative series for population, I calculated a smoother version of the labor force (blue line). Over the last year, but especially in 2025, its growth has slowed from 1½% to zero as the participation rate has fallen, especially among foreign-born workers – the consequence of fear engendered by the Trump Administration’s policies on immigration. And this surely understates the actual deceleration in the labor force because estimates of recent population growth do not yet reflect the sharp reduction in immigration – especially border crossings - over the last year.

Why does this matter? Firstly, addressing the current clamor for a rate cut: growth of employment that is lethargic because it is constrained by slow secular growth of the labor force does not necessarily imply a cyclical rise in unemployment requiring rate cuts under the Taylor rule. Indeed, along a steady-state path with no growth in the labor force, I would expect monthly changes of employment to be zero with a constant unemployment rate. Secondly, however, it is standard macro that, all else equal, slower growth of the labor force is associated with a lower equilibrium real interest rate – i.e., a lower real r-star. The logic is that a deceleration in the labor force results in a relative excess of capital the puts downward pressure on the rate of return.

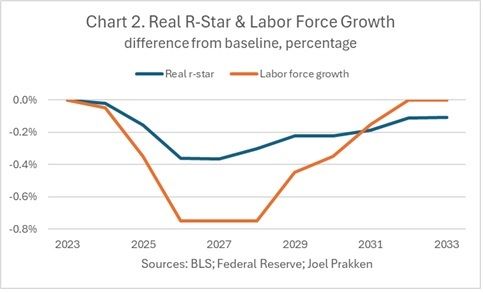

To get an empirical feel for this I fired up my macro system - which, on its supply side, is a Solow growth model – and calibrated it to the current economy assuming the real r-star of 1% shown in the recent SEPs. Then I reduced the annual growth rate of the labor force to zero from a baseline value of 0.7% (the most recent 10-year average) and held it there through 2028 before allowing a gradual recovery. With the Taylor rule maintaining the economy close to full employment, the system kicks out the inferred change in the real r-star. The results of this experiment are shown in Chart 2. They show the deceleration in the labor force is associated with a decline in real r-star that averages about ¼ percentage point through 2028. This could justify the Fed cutting the nominal policy rate even with the economy near full employment and inflation running above target.

None of this is precise. There are unobservable considerations and ceteris that may not be paribus. While in the minority, there are Fed watchers worried that by cutting rates now, the FOMC may validate inflation above 2%. It is a legitimate concern but, thinking about it from a supply-side perspective on the economy, I find that risk a little less concerning.

A PDF version of this commentary is available here.

Joel Prakken

AuthorMore in Author Profile »Joel Prakken is former Chief US Economist of S&P Global and IHS Markit, co-founder of Macroeconomic Advisers, and past president and director of the National Association for Business Economics. He has served as an outside advisor to the Congressional Budget Office, on the Advisory Panel of the Bureau of Economic Analysis, and as a consultant to the Joint Committee on Taxation. He holds a BA in economics from Princeton University and a PhD in economics from Washington University in Saint Louis.