Global| Sep 16 2025

Global| Sep 16 2025Global Trade and Tariffs: Resilience Amid Uncertainty

|in:Viewpoints

At the start of the year, the consensus view was grim: the US-led world economy was heading into recession, inflation would spiral out of control, and global trade faced collapse. Yet, none of this has come to pass. Business-cycle indicators still show resilience, and neither a global trade downturn nor sustained inflationary pressure has materialised.

Global Exports: Resilient Despite Tariffs

The trade war has been disruptive but not disastrous. In the US, GDP contracted in the first quarter, largely because of a sharp rise in imports as manufacturers front-loaded inventories ahead of tariff deadlines. By the second quarter, domestic demand shrank 0.4% quarter-on-quarter as inventories slumped. Exports and residential investment declined, but consumer spending actually strengthened—hardly evidence of households buckling under tariff pressure.

The labour market has softened but isn’t collapsing. Unemployment at 4.3% is still below the pre-pandemic average of 5.1%, while August retail sales rose a brisk 5% year-on-year.

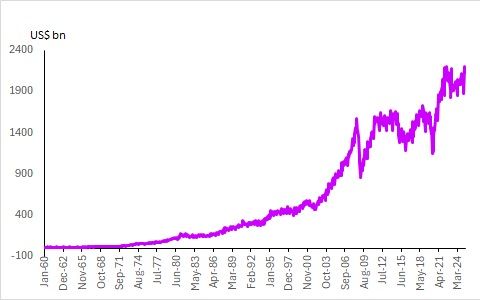

Surprisingly, the trade war’s impact on global trade has been modest. World exports dipped 6.5% from late 2024 to February 2025, only to rebound 13%, leaving shipments up nearly 6% year-to-date through May (Figure 1). The sharpest weakness came in April and May, immediately after tariff hikes, but the recovery was swift.

By comparison, past crises inflicted far greater damage. During the Global Financial Crisis, global exports collapsed by 47% in just eight months. Between 2014 and 2016, shipments fell 28% amid crashing commodity prices, a slowing China, and a strong US dollar. The pandemic caused a 33% peak-to-trough fall when economies shut down worldwide. Against this backdrop, the current downturn appears relatively mild.

Figure 1: World exports

Source: Haver Analytics & Westbourne Research

Regional Shifts

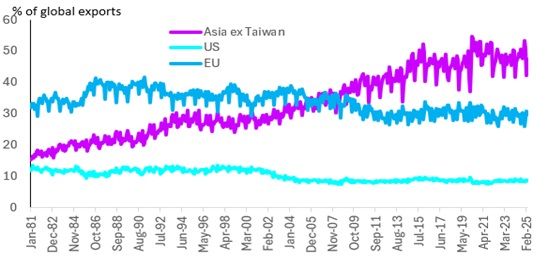

The trade war has altered global trade shares. Asia’s share of exports declined from 53% In January to 49% by May, even as Asian manufacturers continued to dominate (Figure 2). Their performance remains a bellwether for global trade.

Figure 2: Share of global exports

Source: Haver Analytics & Westbourne Research

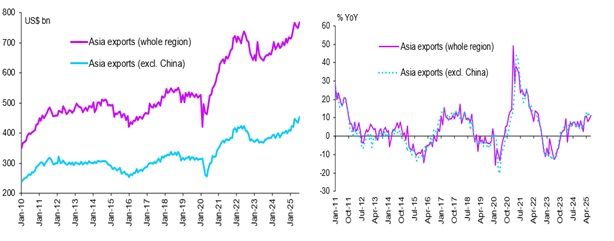

And it is noteworthy that Asian exports, with and without China, have held up through escalating tensions (Figure 3). Chinese exports to the US fell at double-digit rates between April and July, reflecting both weaker demand and shipment front-loading. Yet, overall Asian export growth slowed only to 8% year-on-year in May, stronger than January’s 4.7%. By July, shipments accelerated again, up 11.3% year-on-year.

Figure 3: Asian exports

Source: Haver Analytics & Westbourne Research

US Trade Account

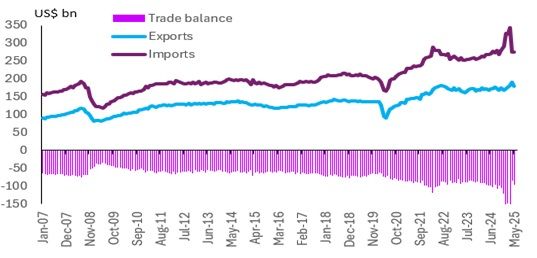

The current account and government coffers have benefited the most from higher import duties. Figure 4 shows the immediate outcome was a strong rise in imports to beat the tariff rise followed by a slump, which leaves the trend mostly unchanged. US exporters are yet to see any positive upside. It is too early. Greater market access from new trade deals will take time to translate into higher US exports. Again, the benefits to American manufacturers are likely to be limited by their relative lack of cost competitiveness compared to emerging market exporters. The biggest beneficiaries will be traditional fossil fuel and defence companies—both sectors on which we have an overweight.

A quick word on dollar weakness and US exports: two points are worth noting. First, currency depreciation typically boosts export competitiveness with a lag of 12 to 18 months. Second, global exporters—particularly those in emerging markets with inherent cost advantages—stand to benefit just as much as, if not more than, their American counterparts, given the US dollar’s central role in international trade settlement.

Figure 4 shows the US the trade balance declining from minus US$155bn in January to minus US$103bn by July. The improvement should be sustained, although a further significant narrowing is unlikely as the economy expands and global exporters adapt to new tariff rates.

Figure 4: US exports, imports and trade balance

Source: Haver Analytics & Westbourne Research

Exporter Pricing Power

The improvement of the trade balance is down to the import bill shrinking. US imports volumes after growing on average by 25% year-on-year in 1Q25, rose on average by 0.6% year-on-year in 2Q25 and by 1.7% year-on-year in July while import prices which were rising by 2.2% year-on-year at the start of the year were flat in August after falling year-on-year in the previous three months.

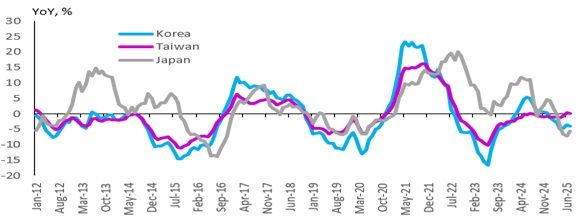

Certainly, Asian exporters have been discounting prices to offset the decline in demand caused by rising tariff rates. This is confirmed by both anecdotal evidence from China and export price data for Japan, Korea and Taiwan (Figure 5). Is this going to last and does it have implications for Asian corporate earnings growth going forward? For China probably yes, because of the weakness of the domestic economy and overcapacity. Elsewhere we expect exporter pricing power to return going into 2026 as global growth and trade pick up and once tariff hikes are digested.

Figure 5: Japan, Korea and Taiwan export prices

Source: Haver Analytics & Westbourne Research

Inflation Impact

Contrary to early fears, tariffs have not unleashed runaway inflation. For tariffs to cause sustained inflation, two conditions must hold: staggered hikes over time, or excessively loose monetary policy. Neither condition applies today. Instead, tariffs deliver a one-off step-up in price levels without igniting an ongoing inflationary spiral.

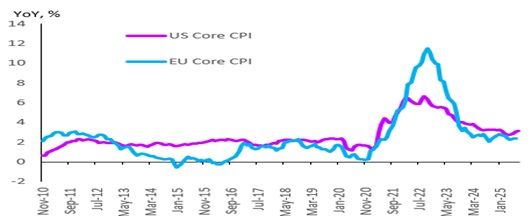

Because Trump’s tariffs target goods rather than services or commodities, their impact is concentrated in core consumer prices (excluding food and energy). These remain contained: in August, US core inflation was 3.1% year-on-year, down from 3.3% at the start of the year. In Europe, the comparable figure was 2.3%, also lower than earlier in the year. Figure 6.

Figure 6: US and EU core consumer price inflation

Source: Haver Analytics & Westbourne Research

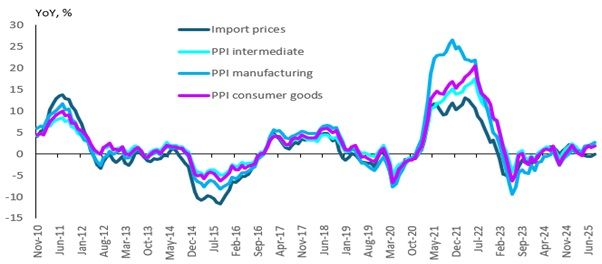

Judging by US import and producer prices - overall and for consumer and intermediate goods - there are signs of pipeline price pressures stemming from higher trade tariffs (Figure 7). This suggest that core consumer prices in the US are likely to rise further.

That said, the transitory impact of high tariff rates on core consumer prices is likely to be more muted than consensus had anticipated. If, as forecast, consumer prices continue to edge up through 2026 it will be cyclically driven, not by tariffs.

Figure 7: US import and producer prices

Source: Haver Analytics & Westbourne Research

Conclusion

Despite sharply higher US import tariffs, the global economy has proven far more resilient than expected. Global exports continue to rise, corporate profitability is holding up even amid price discounting, and inflation remains moderate.

The evidence suggests the impact of tariffs—on trade volumes, corporate earnings, and consumer prices—has been muted and transitory. Trade flows are adjusting, exporters are regaining competitiveness, and households are not retrenching. In short, the tariff war has been more noise than shock: disruptive, yes, but far from the abyss once predicted.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.